Refinancing your mortgage can save money, but escrow fees often catch homeowners off guard. If not handled carefully, these costs can lead to unexpected expenses or financial strain. Here’s what you need to know:

- Escrow Account Basics: When you refinance, your old escrow account is closed, and a new one is funded at closing. This can leave you temporarily paying for two escrow accounts until the refund from the old account arrives.

- Common Pitfalls:

- Forgetting about leftover balances from your old escrow account.

- Underestimating the upfront cash needed to fund the new escrow account.

- Choosing "no-cost" refinancing without understanding how fees are hidden in higher interest rates.

- Assuming all escrow fees are fixed and not shopping around for better rates.

- Overlooking title and recording updates, which can cause issues later.

- Preventing Mistakes: Carefully review your Loan Estimate and Closing Disclosure, confirm tax and insurance figures, and plan for upfront costs. Compare offers from multiple lenders to find better terms.

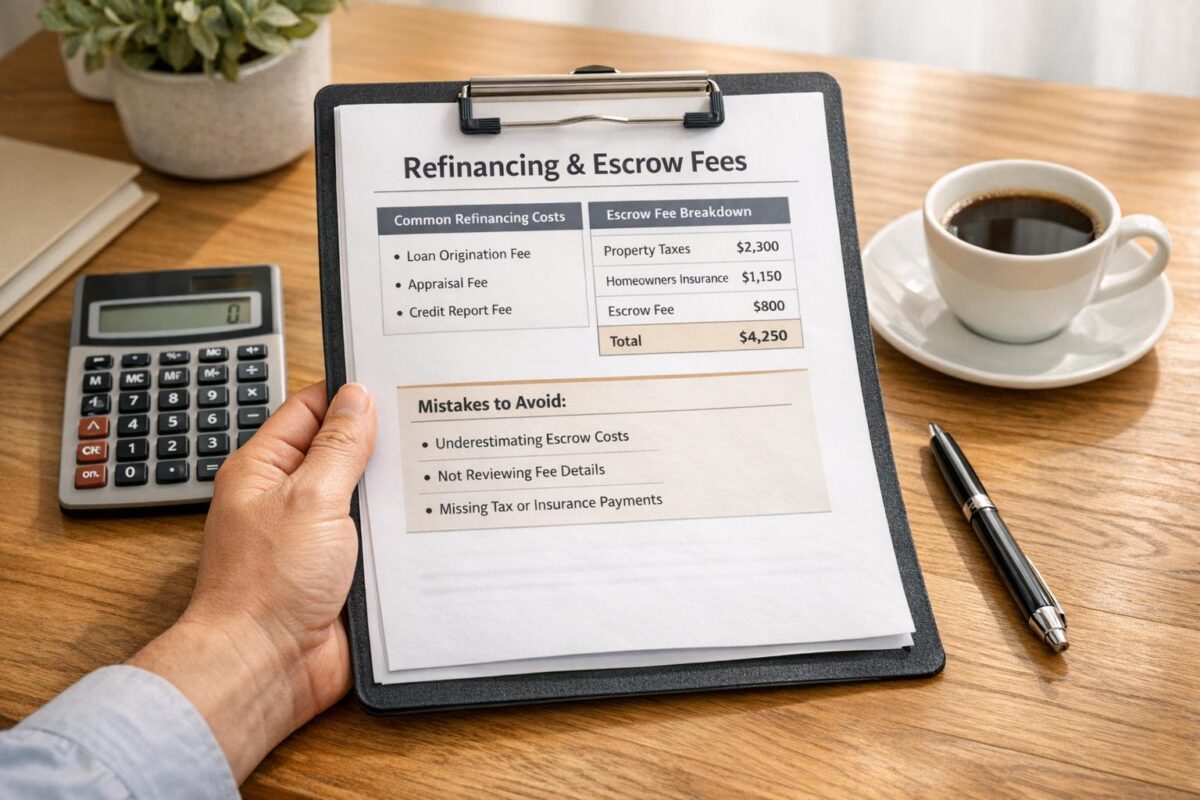

- Cost Breakdown: Refinancing closing costs, including escrow, typically range from 2% to 6% of your loan amount. Escrow fees alone can add 1% to 2% of the home’s purchase price.

Understanding these details will help you avoid surprises and make refinancing a smoother process.

Refinance Math – Closing Costs and Prepaid escrows

Common Mistakes Homeowners Make with Escrow Fees

Refinancing can bring new challenges with escrow fees that might catch you off guard if you’re not prepared. Here’s a look at common mistakes and ways to sidestep them.

Ignoring Leftover Balances from Your Old Escrow Account

When you refinance, your existing escrow balance is typically refunded after your mortgage is paid off. If you switch to a new lender, this refund usually comes as a check. However, if you refinance with your current lender, the escrow balance might be applied directly to your payoff amount instead.

"Once mortgage payoff funds are posted, money held in escrow with your current lender will be returned to you from that lender. The existing escrow account cannot be transferred unless your current lender is the same as your new lender."

– New York State Department of Financial Services

This process often creates a timing gap: you’ll need to fund a new escrow account at closing while waiting weeks for the refund from your old account. To avoid surprises, request a final escrow statement before closing to confirm the balance. Federal law requires lenders to return any surplus over $50. If your refund is delayed, submit a written inquiry – lenders are required to acknowledge your complaint within 20 business days and resolve it within 60 days. Keep in mind, your current lender might also charge fees, such as up to $60 for a payoff statement and $45 for a lien release.

Not Planning for Upfront Escrow Funding

Homeowners sometimes overlook the upfront cash needed to set up a new escrow account during refinancing. This includes 1–2 months’ worth of property taxes and insurance, plus an additional cushion. As a result, you could find yourself temporarily funding two escrow accounts – one at closing and the other until your refund arrives.

"If you are not refinancing with your current lender, you will have to fund the new escrow account at the time of settlement and then wait to receive a check back from your existing lender."

– New York State Department of Financial Services

For instance, on a $300,000 loan, closing costs – including escrow deposits – can range between $6,000 and $18,000. Lenders generally cap the escrow cushion at no more than two months’ worth of annual taxes and insurance. To manage these costs, carefully review your Loan Estimate to identify which fees are fixed and which can be adjusted. If cash is tight, consider asking your lender about a limited cash-out refinance, which can roll these costs into your new loan balance. Just remember, this may reduce your home equity.

Choosing No-Cost Refinancing Without Reviewing Escrow Terms

No-cost refinancing can sound appealing, but the fees don’t disappear – they’re baked into a higher interest rate, often 0.25 to 0.5 percentage points above the market rate. Over time, even a slight rate increase can significantly raise your total interest costs. Before committing to a no-cost refinance, compare the long-term interest costs against the upfront cash required for a standard refinance.

"When you see a ‘no-closing-cost’ mortgage, remember that the costs aren’t just gone – they’re usually added into the interest rate."

– Dan Green, Publisher, Homebuyer.com

Being aware of how fees are structured can help you negotiate better terms for your refinancing.

Assuming Escrow Fees Are Non-Negotiable

Many homeowners mistakenly believe escrow and closing fees are set in stone. In reality, lender fees like origination, application, and underwriting charges can often be negotiated. However, third-party fees – such as appraisals and recording costs – are typically fixed and harder to adjust.

To maximize savings, request Loan Estimates from at least three lenders to compare origination fees and third-party charges. You can also ask title companies to waive smaller fees, such as courier or copying costs. For a $200,000 mortgage, closing costs can range from $4,000 to $12,000, so even modest fee reductions can add up.

Overlooking Title and Recording Updates

It’s essential to ensure your new lender properly records the deed and lien. Mistakes in title updates can create significant headaches when you sell or refinance in the future. Recording fees typically range from $25 to $250, depending on your location. Addressing these details upfront can help you avoid larger refinancing issues down the road.

How to Prevent Escrow Fee Mistakes When Refinancing

Review Your Escrow Details Before You Close

Before finalizing your refinance, carefully compare your Loan Estimate with your Closing Disclosure. This ensures that your escrow costs and fees are consistent. Federal law mandates that you receive the Closing Disclosure at least three business days before closing. Pay close attention to the "Estimated Taxes, Insurance & Assessments" section. This will clarify which charges are included in your monthly payment and which ones you’ll need to pay separately in lump sums.

Double-check your property tax and insurance figures by referring to your latest bills. Lenders sometimes rely on outdated numbers, which can disrupt your financial planning. To avoid surprises, contact your local tax authority directly to confirm your upcoming property tax amount. Also, verify that the escrow cushion – essentially a buffer for your account – doesn’t exceed the legal limit, which is typically about two months’ worth of annual payments.

"By law, some fees cannot increase at all unless you have asked your lender for a change in your loan or your financial information has changed. Other fees are limited to a 10 percent increase."

– Consumer Financial Protection Bureau

Be aware of supplemental tax bills from property reassessments. These are usually not included in standard escrow payments and may need to be paid separately. Once everything checks out, adjust your budget to account for any upfront costs.

Plan Your Budget for Escrow Deposits and Initial Costs

Refinancing usually costs between 2% and 6% of your new loan amount. For a $300,000 loan, this means closing costs – including escrow deposits and initial insurance premiums – could range from $6,000 to $18,000. These payments are typically made via wire transfer or cashier’s check.

To save money, request Loan Estimates from at least three lenders and compare their escrow and origination fees. Pay special attention to the "Services You Can Shop For" section, where you might find more affordable providers for services like title searches and appraisals. Make sure the entire "Estimated Cash to Close" amount is ready and accessible in a liquid account.

If budgeting for these costs feels overwhelming or complex, seeking professional guidance can make a big difference.

Get Professional Help for Complicated Situations

Certain refinancing situations call for expert advice. For example, if you’re removing an ex-spouse from the mortgage during a divorce, managing a property held in a trust, or dealing with foreclosure risks, professional assistance is crucial. If escrow disputes remain unresolved, you can reach out to the Consumer Financial Protection Bureau or your state’s financial services department.

Homeowners struggling with foreclosure or payment difficulties can also seek help from HUD-approved housing counselors. These services are free and provide legitimate advice. For more complicated cases, organizations like Foreclosure Defense Group offer legal support. Their attorneys specialize in helping homeowners navigate foreclosure risks, bankruptcy, loan modifications, and other challenges tied to escrow fees and refinancing. They can also explore options like loan forbearance or deed-in-lieu arrangements if traditional refinancing isn’t viable due to legal issues.

sbb-itb-d613a70

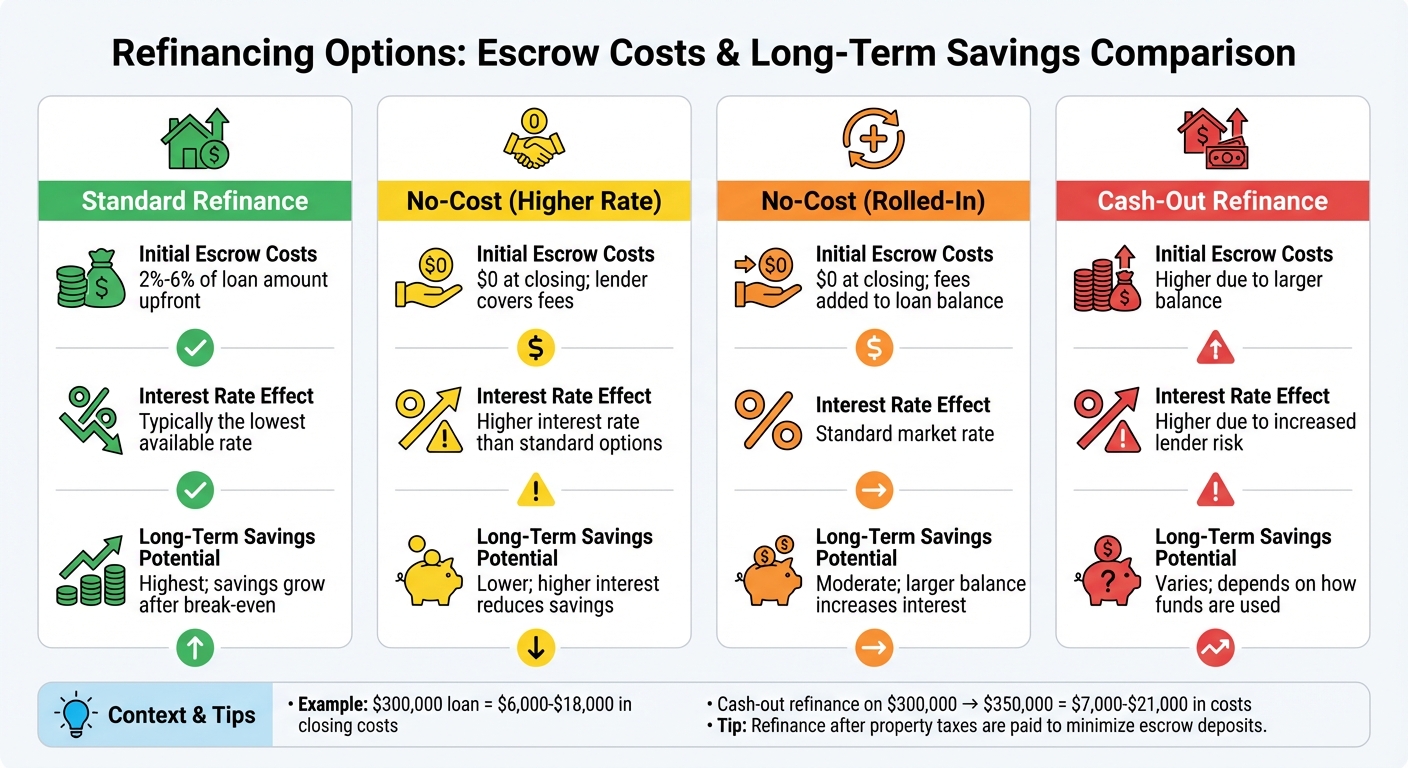

Escrow Costs Across Different Refinancing Options

Refinancing Options: Escrow Costs and Long-Term Savings Comparison

Escrow costs can vary significantly depending on the refinancing option you choose. For a standard refinance, you’ll generally need to pay between 2% and 6% of your loan amount upfront at closing. This includes the initial escrow deposit for property taxes and insurance. While this option requires upfront costs, it often offers the lowest interest rates, which can lead to greater long-term savings after you reach the break-even point.

With no-closing-cost refinancing, you avoid upfront expenses, but there’s a trade-off. Lenders either provide credits that increase your interest rate or roll the fees into your loan balance, which raises the total loan amount. Both approaches eliminate out-of-pocket costs at closing, but they reduce your overall savings over time due to higher monthly payments or increased interest charges.

Cash-out refinancing typically comes with even higher costs. This is because it increases your loan balance, which amplifies percentage-based fees. Additionally, lenders see this option as riskier since you’re borrowing more than you owe, rather than just adjusting your rate or term. For instance, if you refinance a $300,000 loan and opt for a cash-out refinance that raises your balance to $350,000, you could expect total closing costs to fall between $7,000 and $21,000.

Here’s a quick comparison of these refinancing options:

Escrow Cost Comparison Table

| Refinancing Option | Initial Escrow Costs | Interest Rate Effect | Long-Term Savings Potential |

|---|---|---|---|

| Standard Refinance | 2%–6% of loan amount upfront | Typically the lowest available rate | Highest; savings grow after break-even |

| No-Cost (Higher Rate) | $0 at closing; lender covers fees | Higher interest rate than standard options | Lower; higher interest reduces savings |

| No-Cost (Rolled-In) | $0 at closing; fees added to loan balance | Standard market rate | Moderate; larger balance increases interest |

| Cash-Out Refinance | Higher due to larger balance | Higher due to increased lender risk | Varies; depends on how funds are used |

Timing also plays a role in escrow costs. Refinancing later in the year can require a larger escrow deposit, as lenders may need to collect more funds upfront for property taxes. To minimize these costs, consider refinancing shortly after your property taxes have been paid.

Conclusion

Refinancing can help lower your monthly payments and potentially save you money, but mistakes with escrow fees might eat into those savings. The key to avoiding surprises is to understand exactly what you’re paying for upfront and how different refinancing options impact your long-term costs. For example, closing costs typically fall between 2% and 5% of your loan’s value, while escrow fees often add another 1% to 2% of the home’s price. Knowing these details can help you make better decisions when it’s time to close.

To figure out if refinancing makes sense for you, calculate your break-even point by dividing the total loan costs by your monthly savings. If you plan to move before hitting that break-even point, refinancing might not be worth it. Also, don’t assume your current lender has the best offer – shop around and get quotes from at least three lenders on the same day to compare rates and fees.

As SmartAsset puts it:

"Refinancing isn’t something you want to jump into without running all the numbers first and making sure that you will come out ahead financially." – SmartAsset

Be sure to understand the difference between "no-cost" and "no-cash" refinancing. No-cost refinancing may sound appealing, but the fees are often hidden in higher interest rates or rolled into the loan, which can reduce your long-term savings.

If escrow fee issues become complicated – such as with trust-held properties or unclear terms – seeking professional advice can help you avoid costly mistakes. A financial advisor can confirm whether refinancing aligns with your long-term goals rather than just addressing short-term cash flow. For homeowners dealing with foreclosure risks or payment struggles, organizations like Foreclosure Defense Group provide legal assistance, including help with foreclosure defense, bankruptcy, loan modifications, and other challenges tied to escrow fees and refinancing.

FAQs

What are the downsides of no-cost refinancing with hidden escrow fees?

Choosing a "no-cost" refinance might sound appealing at first, but it often comes with hidden drawbacks – especially when escrow fees are involved. Instead of paying these fees upfront, lenders typically roll them into the loan by increasing your interest rate. This means you could end up with higher monthly payments and pay significantly more in interest over the life of the loan.

To steer clear of this pitfall, take the time to thoroughly review your loan terms. Ask your lender for a detailed breakdown of all costs, including how escrow fees are being handled. Clear insight into these details can help you make smarter financial decisions and avoid added stress down the line.

How can I make sure I get my escrow refund quickly after refinancing?

To get your old escrow account balance refunded quickly after refinancing, start by requesting a written escrow analysis before the closing process. Check if your account has a surplus of $50 or more, as federal law mandates refunds for amounts at or above this threshold. Next, submit a written refund request to your previous loan servicer, making sure to include your forwarding address. Be sure to follow up within the 30-day window outlined by the Real Estate Settlement Procedures Act (RESPA) and any relevant state laws to keep things on track. If this feels overwhelming or you encounter issues, consider reaching out to a professional, such as Foreclosure Defense Group, for guidance and to avoid unnecessary delays.

How can I reduce escrow costs when refinancing my mortgage?

Reducing escrow costs during refinancing starts with one key step: comparing lender estimates. Some lenders might lower or even waive fees like origination or processing costs, particularly if you have strong credit or substantial home equity. It pays to shop around and negotiate – you might be surprised by how much you can save.

Another strategy is to request an escrow analysis before finalizing your refinance. For instance, if your homeowner’s insurance premium has gone down or you find a more affordable policy, your lender can recalculate the escrow reserves. This adjustment can lower both your monthly escrow payments and upfront costs. If upfront savings are your main concern, you might also consider a no-closing-cost refinance. With this option, fees are either rolled into your loan or offset by a slightly higher interest rate. While it helps preserve cash initially, it may increase the overall cost of the loan in the long run.

Foreclosure Defense Group advises reviewing your Good Faith Estimate (GFE) as early as possible. Double-check all line-item fees and keep records like insurance bills and escrow statements handy. These documents can support any requests for adjustments. By staying informed and proactive, you can cut down on escrow costs and secure refinancing terms that work best for you.

Related Blog Posts

- How to Refinance from ARM to Fixed-Rate Mortgage

- Escrow Errors vs. Lender Mismanagement

- How Appraisals Affect Refinancing Costs

- How Private Lender Refinancing Stops Foreclosure