Loan servicing transfers can cause serious problems for homeowners when handled poorly. These issues include lost payments, misapplied funds, and missing documentation, which can lead to credit damage, late fees, and even foreclosure. Federal laws, like RESPA, provide protections, but homeowners must act quickly and document everything to safeguard their rights.

Key Takeaways:

- Common Issues: Payments being lost, applied incorrectly, or placed in suspense accounts; missing or inaccurate loan records.

- Consequences: Damaged credit scores, increased fees, wrongful foreclosure risks.

- Federal Protections: RESPA requires servicers to notify borrowers before and after a transfer, prohibits late fees for 60 days post-transfer, and mandates error resolution within 30 business days.

- Steps to Protect Yourself: Monitor your account, document errors, send formal Notices of Error (NOEs), and seek legal help if needed.

If your loan transfer seems mishandled, take immediate action to protect your home and finances.

Problems Caused by Improper Loan Transfers

When a mortgage servicing transfer goes off track, it can lead to a host of problems for homeowners. These issues don’t just disrupt payment processing – they can also jeopardize your financial stability and credit. Being aware of these potential pitfalls can help you act quickly to address them.

Payment Crediting Errors and Lost Payments

One of the most common issues is the mishandling of payments during the transfer process. Ideally, your old servicer should forward payments to the new one. But this doesn’t always happen. Payments may be returned to you, applied to the wrong account, or even sent to the wrong place entirely.

Sometimes, payments end up in suspense accounts instead of being applied to your loan balance. This can result in your account being marked as delinquent, even though you’ve paid on time. On top of that, new servicers might ignore pre-existing loan modification agreements, making your account even more complicated. If you had a pending loss mitigation application during the transfer, federal law requires the new servicer to review it within 30 days of the transfer date. Unfortunately, this rule is often overlooked.

Besides payment errors, missing or inaccurate data can also create significant challenges.

Missing Documentation and Chain-of-Title Issues

Data errors during loan transfers can lead to serious legal and financial complications. When servicers transfer your loan details from one database to another, critical information – like income records, property taxes, insurance premiums, or HOA dues – can be lost or misrecorded. These inaccuracies can directly affect Net Present Value (NPV) calculations, which are crucial for determining loan modification eligibility. Mistakes in these calculations could result in wrongful denials.

For example, in May 2024, Wells Fargo revealed that a computer glitch had prevented about 870 eligible mortgage borrowers from receiving loan modifications. Tragically, this error led to the wrongful foreclosure of 545 homes.

"These mistakes can cause many problems for a homeowner, like missing out on getting the loan modified or even a wrongful foreclosure".

Such documentation errors often lead to further complications, especially when it comes to communication between servicers.

Communication Breakdowns Between Servicers

A lack of coordination between your old and new servicers can leave you unsure about your loan’s status. In some cases, one department may process your loss mitigation application while another moves forward with foreclosure. This illegal practice, known as "dual tracking," becomes more common during poorly managed transfers.

The situation gets even more tangled when servicers bring in subservicers to handle day-to-day operations. This extra layer increases the chances of information getting lost along the way.

"In some cases, the new servicer fails to review an already submitted loss mitigation application or fails to honor a modification agreement with the previous servicer".

"Data errors often show up in the way the servicer records your income, expenses, property value, or loan terms and then uses that wrong information to run the NPV test".

These communication and data issues can create a cascade of problems, leaving homeowners vulnerable to financial and legal risks.

sbb-itb-d613a70

Legal and Financial Consequences for Homeowners

When loan transfer errors go unresolved, they can lead to serious legal and financial challenges for homeowners. Issues like misapplied payments or poor communication don’t just cause operational headaches – they can also wreak havoc on your credit and even put your home at risk.

Credit Score Damage and Financial Impact

Your payment history accounts for 35% of your FICO Score, making it a critical factor in maintaining good credit. If a servicer mistakenly reports an on-time mortgage payment as late, the consequences can be severe. Even a single payment reported as 30 days late or more can significantly lower your credit score.

"The servicer then improperly reports your payment as missed to the credit reporting bureaus and charges you a late fee." – Amy Loftsgordon, Attorney, Nolo

This kind of error doesn’t just hurt your credit – it can make borrowing more expensive across the board. Higher interest rates on future loans, credit cards, and insurance are just the beginning. On top of that, late fees and other default-related charges can pile up quickly, inflating your loan balance. Even if the error is eventually corrected, catching up can feel like a losing battle.

But the financial toll doesn’t stop there. If these errors remain unresolved, they can lead to even more serious consequences, like foreclosure.

Increased Foreclosure Risk

Loan transfer errors can create a domino effect, sometimes leading to a technical default that puts homeowners at risk of foreclosure. Misapplied payments or lost records can falsely signal delinquency to the servicer. Worse yet, practices like dual tracking – where foreclosure proceedings continue while loss mitigation efforts are under review – can amplify the risk.

Federal law prohibits this dual tracking if a complete loss mitigation application is submitted at least 37 days before a scheduled foreclosure sale. However, poorly managed transfers can still result in these violations.

"Calling the servicer, sending a notice of error, or filing a complaint with the Consumer Financial Protection Bureau is highly unlikely to stop foreclosure proceedings. You’ll most likely need an attorney’s assistance to halt a foreclosure." – Amy Loftsgordon, Attorney

If foreclosure looms due to a transfer error, time becomes your most valuable resource. Administrative steps like filing notices of error may not be enough to stop a scheduled sale. In such cases, swift legal action is often the only way to protect your home.

Legal Protections and Recognizing Servicer Violations

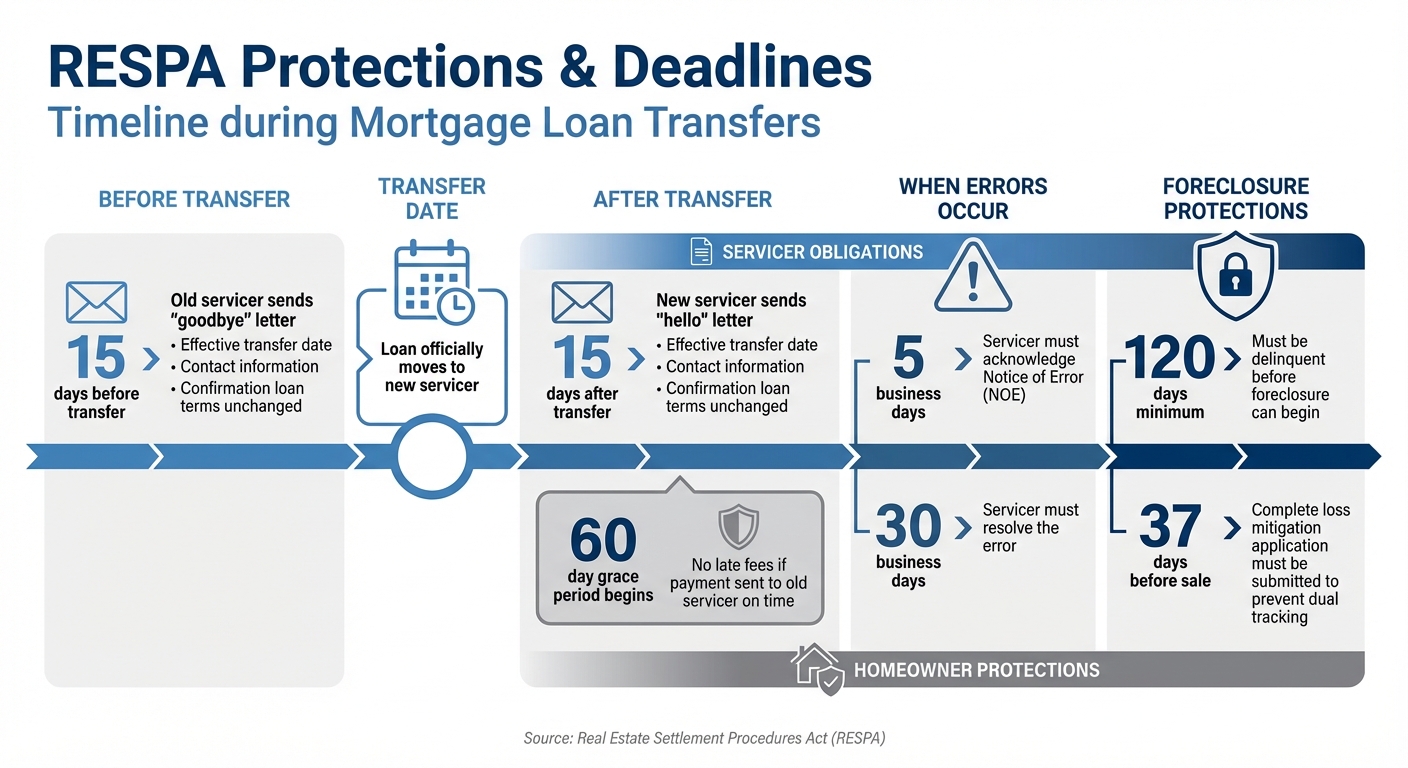

RESPA Timeline and Protections During Mortgage Loan Transfers

Federal Protections Under RESPA

The Real Estate Settlement Procedures Act (RESPA) offers specific protections when your loan servicer changes. Under RESPA, the old servicer must send you a "goodbye" letter at least 15 days before the transfer, and the new servicer must follow up with a "hello" letter within 15 days after the transfer. These letters must include the effective transfer date, contact information, and a confirmation that your loan terms remain unchanged.

Additionally, RESPA provides a 60-day grace period after the transfer. During this time, if you accidentally send your payment to the old servicer but pay on time, the new servicer cannot charge late fees or report the payment as late.

"Under the federal Real Estate Settlement Procedures Act (RESPA), if you send a written ‘notice of error’ or ‘request for information,’ the servicer has to respond to your letter within specific time limits."

- Amy Loftsgordon, Attorney, Nolo

If you believe an error has occurred, you can file a formal Notice of Error (NOE). The servicer must acknowledge your letter within 5 business days and resolve the issue within 30 business days. If the transfer was recent (less than a year ago), both the old and new servicers are required to investigate and respond. RESPA also prohibits "dual tracking", meaning servicers cannot proceed with foreclosure while reviewing a complete loss mitigation application. Furthermore, foreclosure cannot begin unless you are more than 120 days behind on payments.

These protections are designed to help you identify and address any violations by your loan servicer.

Identifying Violations and Building a Case

Understanding RESPA protections makes it easier to spot when a servicer fails to meet its legal duties. For instance, if you don’t receive both the goodbye and hello letters within the required timeframes or if the letters are missing key details like the transfer date or contact information, this could signal a violation.

Payment issues are another common problem. If the new servicer charges a late fee or reports a late payment during the 60-day grace period – even though you paid on time to the old servicer – that’s a clear breach of RESPA rules. Similarly, if the new servicer refuses to honor a loan modification previously agreed upon by the old servicer, that’s another red flag. It’s a good idea to monitor your account closely for at least two payment cycles after a transfer to ensure payments are being applied correctly to the principal, interest, and escrow.

Non-responsiveness from the servicer is another warning sign. If you submit a written Notice of Error and the servicer doesn’t acknowledge it within 5 business days or resolve the issue within 30 business days, they may be violating federal law. To protect yourself, keep copies of all transfer letters, payment receipts, and correspondence with servicers. These records are invaluable if you need to build a case for noncompliance. If you encounter these types of issues, Foreclosure Defense Group can help you enforce your rights and navigate the legal process.

| Protection | Timeline |

|---|---|

| "Goodbye" Notice (Old Servicer) | At least 15 days before transfer |

| "Hello" Notice (New Servicer) | No more than 15 days after transfer |

| Payment Grace Period | 60 days (no late fees for payments sent to old servicer) |

| NOE/RFI Acknowledgment | 5 business days |

| Error Resolution | 30 business days |

| Foreclosure Delinquency Buffer | 120 days minimum before first filing |

Steps to Address and Resolve Loan Transfer Errors

Documenting and Reporting Errors

If you notice payment or documentation errors with your loan, it’s important to act quickly. Start by documenting and reporting any discrepancies to your loan servicer. Reach out via phone, their secure portal, or email, and make sure to log the date, time, and the name of the representative you spoke with. If this initial contact doesn’t resolve the issue, escalate the matter by sending a formal Notice of Error (NOE) under the Real Estate Settlement Procedures Act (RESPA). Be sure to send the NOE to the servicer’s designated dispute address – not the payment address.

If your loan was transferred within the past year, send the NOE to both your old and new servicers. Use certified mail with a return receipt to confirm delivery.

"If your initial contact with the servicer doesn’t resolve the problem, you can send your servicer a ‘notice of error.’ Under the federal Real Estate Settlement Procedures Act (RESPA), you can send your servicer a letter informing them that it made an error on your account."

Before drafting the NOE, gather supporting evidence like canceled checks, bank statements, and transfer letters. If you need additional details, consider sending a Request for Information (RFI) to access your complete payment history or confirm the current loan owner. While the dispute is being reviewed, continue making your regular mortgage payments to the new servicer to avoid default or foreclosure. Also, keep a close eye on your account for at least two months to ensure no payments are misapplied.

If the servicer doesn’t resolve the issue within the legally required timeframe, consider filing a complaint with the Consumer Financial Protection Bureau (CFPB).

Once you’ve taken these steps, the next move is to consult a legal professional for further assistance.

Getting Professional Legal Help

If your efforts to resolve the issue don’t yield results, it’s time to seek legal guidance. Navigating RESPA rights can be complex, and an experienced attorney can help identify errors you might overlook. They’ll also ensure servicers comply with strict response deadlines under RESPA and the Truth in Lending Act (TILA).

"Expert foreclosure defense attorneys ensure you understand and enforce your rights."

If foreclosure is imminent, don’t delay in seeking legal help. A Notice of Error alone may not stop a scheduled sale, but an attorney can step in to halt wrongful foreclosure proceedings. This is especially critical if the servicer violated the 60-day grace period or moved forward with a sale while a complete application was still pending.

Foreclosure Defense Group offers free consultations and experienced legal representation for homeowners in such situations. Their attorneys can help you address servicer violations, enforce federal protections, and explore potential solutions like loan modifications, forbearance agreements, or even bankruptcy assistance.

Acting early is key. The sooner you involve legal professionals, the more options you’ll have to protect your home and your rights.

Conclusion

When loans are transferred improperly, it can lead to serious issues like misapplied payments, credit score damage, and even the risk of wrongful foreclosure. To safeguard yourself, it’s crucial to stay alert during the transition and keep thorough records of all interactions. Remember, new servicers cannot charge late fees for timely payments sent to the previous servicer during a 60-day grace period. You also have the right to send formal Notices of Error to demand corrections when mistakes occur.

"The most important thing you can do as a homeowner is stay informed and read all notices you receive." – Upsolve Team

For the first two months after a loan transfer, closely monitor your account and maintain detailed records. If you notice any discrepancies, act quickly by sending a written Notice of Error via certified mail to both the old and new servicers. This creates a paper trail that strengthens your position under RESPA and ensures you can take legal action if necessary.

If errors persist or foreclosure becomes a concern, don’t hesitate to seek legal help. Foreclosure Defense Group offers free consultations and skilled representation to address servicer violations, enforce federal protections, and explore options like loan modifications or forbearance agreements. An experienced attorney can help you stop wrongful foreclosure proceedings, ensure servicers comply with federal deadlines, and protect your property rights.

Time is critical – take action at the first sign of trouble to protect your home and financial well-being. Don’t wait until a foreclosure sale is imminent; reach out for legal assistance as soon as possible.

FAQs

How can I prove my mortgage payment wasn’t late after a servicer transfer?

To show that your mortgage payment wasn’t late after a servicer transfer, hold onto key documentation like bank statements, canceled checks, or payment confirmation emails that confirm you paid on time. If you sent a payment to the previous servicer during the transition, they are required to either forward it to the new servicer or return it to you. If your payment hasn’t been properly credited, you can dispute the error by submitting this evidence and following the new servicer’s error resolution process.

What should I include in a RESPA Notice of Error for a transfer mistake?

When drafting a RESPA Notice of Error related to a transfer mistake, it’s crucial to clearly outline the specific issue. For example, this might include a foreclosure being initiated before the 120th day of delinquency or a property sale conducted in violation of Regulation X (§ 1024.41). Make sure to send the notice at least 7 days before the scheduled foreclosure sale. Additionally, you should request the loan servicer to either cancel or postpone the sale if the identified error directly contributed to the problem.

Can a loan transfer error stop or delay a foreclosure sale?

Mistakes during a loan transfer can stall or even stop a foreclosure sale. Errors in loan servicing or mishandling of paperwork might give homeowners a legal argument to contest the foreclosure. These challenges can serve as a defense, helping to safeguard homeowners’ rights and possibly prevent the foreclosure process from moving forward.

Related Blog Posts

- Top Legal Cases on Loan Modification Breaches

- Common Lender Errors in Foreclosure Cases

- Loan Modification Compliance: Legal Rights Explained

- Loan Servicer Errors in Escrow Explained