If you’re facing foreclosure in Florida and the lender claims the original promissory note is lost, here’s what you need to know:

When a lender can’t produce the original note, they must file a lost note affidavit to proceed. This document proves their right to enforce the debt and complies with Florida’s strict legal requirements. However, errors in these affidavits – like missing documentation or gaps in the note’s ownership history – can give homeowners a chance to challenge the foreclosure.

Key Points:

- What is a Lost Note Affidavit? A sworn statement replacing a missing promissory note, detailing its history and the lender’s right to enforce it.

- Legal Requirements: Florida law mandates clear proof of ownership, a chain of endorsements, and safeguards like bonds to protect homeowners.

- Common Errors: Missing documents, incomplete ownership history, or affidavits signed without proper knowledge can derail foreclosure cases.

- Homeowner Protections: Courts may dismiss cases or impose penalties if lenders fail to meet these standards.

Bottom Line: If you’re dealing with a foreclosure involving a lost note affidavit, review the affidavit closely for errors or seek legal advice. These mistakes can be used to challenge the lender’s claim and potentially stop the foreclosure process.

Florida Statute 702.015 Requirements for Lost Note Affidavits

Florida Lost Note Affidavit Requirements and Common Errors

Florida law imposes strict guidelines for lost note affidavits, ensuring lenders can establish their foreclosure rights even without the original note.

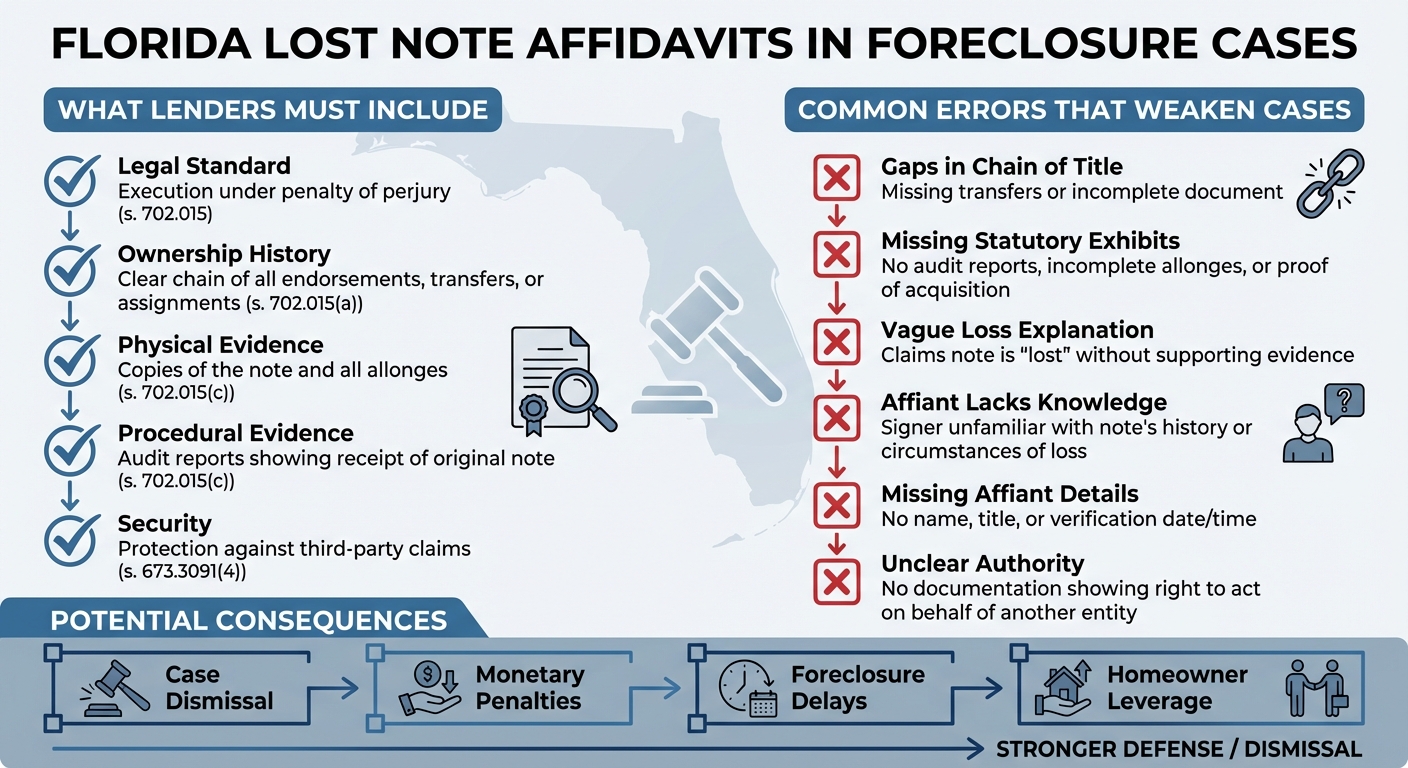

What Must Be Included in the Affidavit

The affidavit must be sworn under penalty of perjury and attached to the foreclosure complaint. This means the person signing the affidavit could face legal consequences if the information provided is false.

It should include a clear chain of endorsements, transfers, or assignments that tracks the note’s history. Any gaps in this chain can weaken the lender’s claim. Additionally, the affidavit must outline specific facts that show the plaintiff is entitled to enforce the note, as required by Florida Statute 673.3091.

| Requirement Type | What the Lender Must Include | Legal Reference |

|---|---|---|

| Legal Standard | Execution under penalty of perjury | s. 702.015 |

| Ownership History | Clear chain of all endorsements, transfers, or assignments | s. 702.015(a) |

| Physical Evidence | Copies of the note and all allonges | s. 702.015(c) |

| Procedural Evidence | Audit reports showing receipt of the original note | s. 702.015(c) |

| Security | Protection against third-party claims | s. 673.3091(4) |

These elements are essential to meet both evidentiary and statutory requirements.

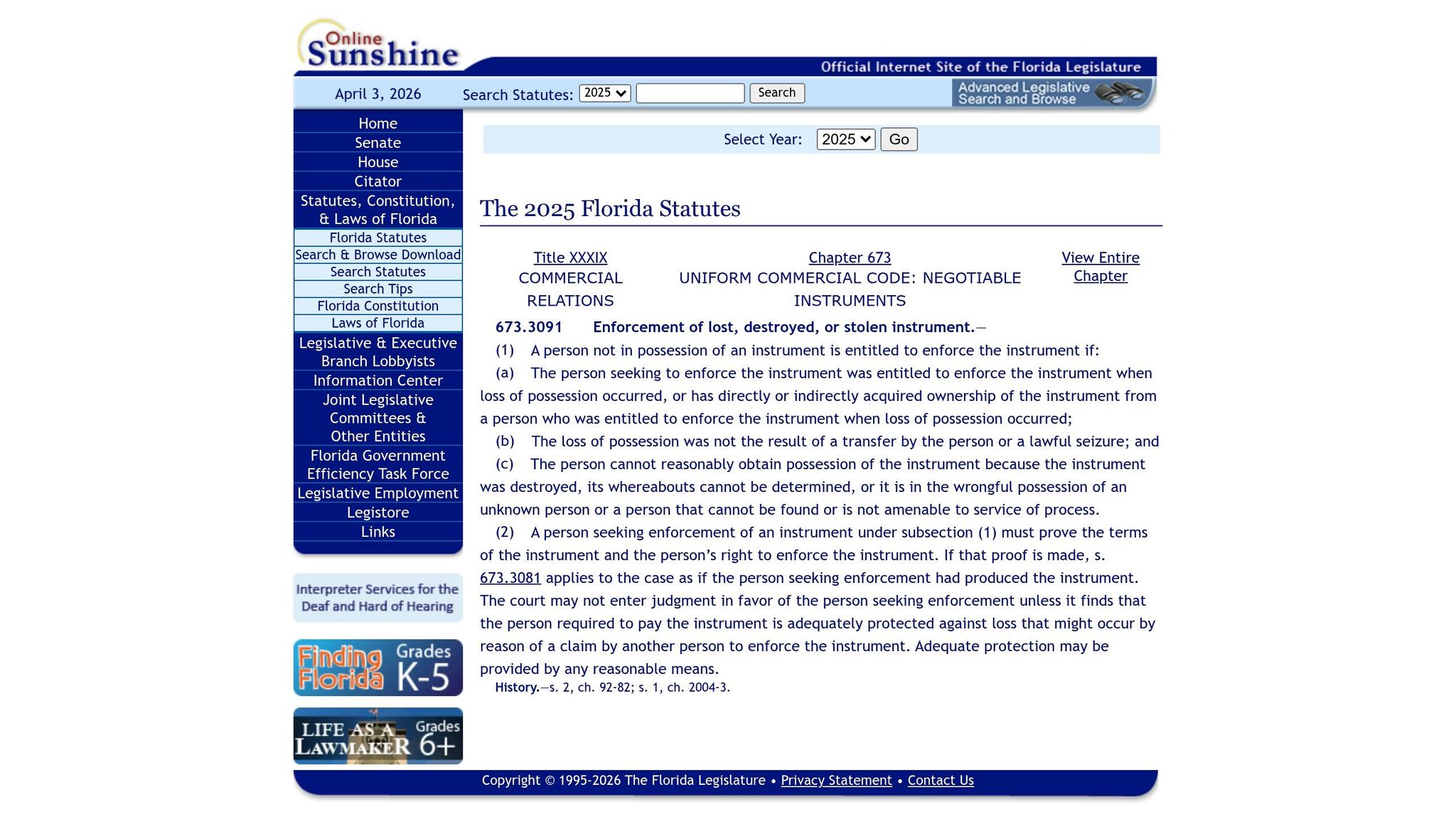

How Florida Statute 673.3091 Applies

Florida Statute 673.3091 builds on the affidavit’s requirements by detailing the criteria for enforcing a lost note. Lenders must prove they were entitled to enforce the note either at the time of its loss or through subsequent acquisition.

They must also establish that the loss of the note wasn’t due to a transfer or lawful seizure. Furthermore, they need to show the note cannot reasonably be recovered – whether it was destroyed, its location is unknown, or it’s in the wrongful possession of someone who cannot be reached. Before granting a final judgment, the court must ensure the homeowner is protected against the possibility of another party presenting the original note to claim the same debt. This protection might take the form of a surety bond, letter of credit, or cash deposit.

Supporting Documents and Evidence

To comply with Florida Statute 702.015(c), lenders must provide additional supporting documents alongside the affidavit. These include copies of the promissory note, all allonges, and audit reports confirming receipt of the original note.

Lenders are also required to submit any other available evidence related to the acquisition, ownership, and possession of the note. Courts can impose sanctions on plaintiffs who fail to meet these documentation standards, making it crucial for lenders to provide complete and accurate evidence from the outset.

sbb-itb-d613a70

Problems with Lost Note Affidavits in Foreclosure Cases

Lenders often make serious mistakes in lost note affidavits, which can weaken their foreclosure cases and give homeowners an opportunity to push back. Understanding these mistakes is crucial for homeowners looking to challenge improper foreclosure actions.

Incomplete or Incorrect Affidavits

One of the most common issues involves gaps in the chain of title. According to Florida Statute 702.015(a), affidavits must clearly outline "a clear chain of all endorsements, transfers, or assignments" of the promissory note. Missing transfers or incomplete documentation violates this requirement and leaves the affidavit open to scrutiny.

Another frequent problem is missing statutory exhibits. Lenders are required to include audit reports, complete allonges, and proof of acquisition. The affidavit must also explain why the note is lost in a way that meets legal standards. Vague claims that the note is "lost" without supporting evidence fail to satisfy these requirements.

Questions About Affiant Knowledge and Authority

The individual signing the affidavit must have personal knowledge of the facts they are attesting to under penalty of perjury. Issues arise when the affiant is unfamiliar with the note’s history, the circumstances of its loss, or the lender’s right to enforce it. By law, the affidavit must include the affiant’s name, title, and the exact date and time of verification. Omitting these details creates procedural flaws.

If the plaintiff is acting on behalf of another entity, they must clearly identify the document granting them the authority to act. A lack of detail about this authority can undermine the entire foreclosure case.

How Affidavit Errors Affect Foreclosure Proceedings

Homeowners can use these affidavit errors to fight foreclosures, especially with the help of legal counsel. Spotting deficiencies in affidavits can help homeowners protect their rights during foreclosure proceedings. These errors not only raise doubts about the lender’s authority but also lead to immediate procedural setbacks.

Flawed affidavits can bring foreclosure cases to a standstill. Florida Statute 702.015(d) gives courts the power to impose sanctions on plaintiffs who fail to meet disclosure and affidavit requirements. Sanctions may include case dismissal or monetary penalties.

These mistakes also cause delays and create procedural hurdles. Courts cannot issue a final judgment unless the lender provides adequate protection – such as a surety bond, letter of credit, or cash deposit – to safeguard the homeowner against potential claims from others who might later produce the original note. If the affidavit doesn’t address this requirement or the lender fails to offer protection, the case stalls. For homeowners, identifying these flaws can provide critical leverage to contest the foreclosure and potentially negotiate better terms.

How Homeowners Can Challenge Lost Note Affidavits

Homeowners facing foreclosure due to lost note affidavits have options to push back by focusing on gaps or errors in the lender’s documentation.

Review the Affidavit for Errors

Start by carefully examining the affidavit. Check whether it was executed under penalty of perjury and ensure every transfer in the chain of title is accounted for. If there are missing endorsements between the original lender and the current plaintiff, that could be a critical issue for your defense.

The affidavit should also include all required exhibits, such as audit reports and proof of receipt. If the lender relies solely on a copy of the note and skips these supporting documents, they might not meet the legal requirements. Any discrepancies you uncover here could weaken the lender’s case.

Question the Lender’s Right to Foreclose

After reviewing the affidavit, you can question the lender’s authority to foreclose if the documentation is incomplete. Even when the affidavit appears complete, you can still challenge the lender’s standing by demanding clear proof of a proper chain of title and safeguards against future claims.

For example, in September 2011, the Florida District Court of Appeal reversed a summary judgment in Gee v. U.S. Bank Nat’l Ass’n. The court found that the lender failed to show how American Home Mortgage Servicing became the successor to Option One Mortgage Corporation. If the lender tries to secure a summary judgment without fully reestablishing the chain of title for the lost note, object immediately. Additionally, insist that the lender provide adequate protection, such as a surety bond or indemnification, to ensure you won’t face future claims over the same note.

Get Legal Help

Given the strict statutory requirements and the potential complexity of lost note affidavits, it’s wise to seek professional legal advice. A qualified attorney can identify missing links in the chain of title and ensure the lender complies with state laws. For instance, Foreclosure Defense Group offers free consultations to help homeowners craft a strong defense strategy and safeguard their homes. Legal expertise can make all the difference in navigating these challenges effectively.

Conclusion

Know Your Rights as a Homeowner

Understanding the role of lost note affidavits can have a major impact on the outcome of your foreclosure case. Florida law imposes strict guidelines on lenders who claim to have lost the original promissory note. These affidavits must be signed under penalty of perjury and clearly outline the chain of endorsements involved. If a lender fails to meet these legal requirements, you may be able to challenge their right to foreclose.

"A party seeking foreclosure must prove by competent, substantial evidence that it has standing to foreclose at the time of filing the lawsuit." – ORFINGER, J., Florida District Court of Appeals

The October 2017 case of Wisman v. Nationstar Mortg., LLC highlights the importance of these defenses. Mary T. Wisman successfully fought foreclosure after the court found that Nationstar’s lost note affidavit relied on inter-office emails rather than firsthand knowledge. The Florida District Court of Appeals overturned the foreclosure judgment because Nationstar failed to prove it had standing when the case was filed.

Knowing your rights is just the first step – acting promptly is equally important.

Act Quickly and Get Professional Advice

Time is of the essence. Start by reviewing the affidavit for critical exhibits, such as audit reports or proof of ownership, and verify that the affiant has personal knowledge of the note’s history. Any gaps in the chain of title or missing documentation can significantly weaken the lender’s case and bolster your defense.

An experienced attorney can spot technical errors that might otherwise go unnoticed and ensure the lender provides proper safeguards against future claims on the same debt. For example, Foreclosure Defense Group offers free consultations to help you explore your options and develop a robust defense strategy. Don’t delay – securing legal representation early can make all the difference in protecting your home and your rights.

FAQs

Can a lender foreclose in Florida without the original promissory note?

In Florida, lenders are required to have the original promissory note to proceed with a foreclosure. However, if the original note is unavailable, they can still move forward – but only by providing a sworn affidavit or other legal documentation, like a lost note affidavit. This document must confirm that the note has been lost or destroyed and also prove the lender’s legal authority to enforce the debt, as mandated by Florida law.

What should I look for to spot defects in a lost note affidavit?

To spot issues in a lost note affidavit, look for a certification that confirms whether the claimant had possession of the original promissory note. This should include details about its location and who certified it. Additionally, the affidavit must clearly state that the claimant either holds the original note or provides a factual basis to justify enforcement, as outlined under Florida law.

How can I force the lender to prove standing and the chain of ownership?

To challenge a lender’s standing and chain of ownership in a Florida foreclosure, you can request documentation and affidavits that demonstrate their legal authority to enforce the note. Under Florida law, lenders are required to submit an affidavit – signed under penalty of perjury – outlining all endorsements, transfers, or assignments of the promissory note. Additionally, the foreclosure complaint must include specific allegations proving the lender’s right to enforce the note or showing that they have delegated authority to do so.

Related Blog Posts

- 3 Ways to Stop Foreclosure in Florida

- How Attorneys Help Resolve Mortgage Disputes

- Common Lender Errors in Foreclosure Cases

- Private Mortgage Foreclosure Process in Florida