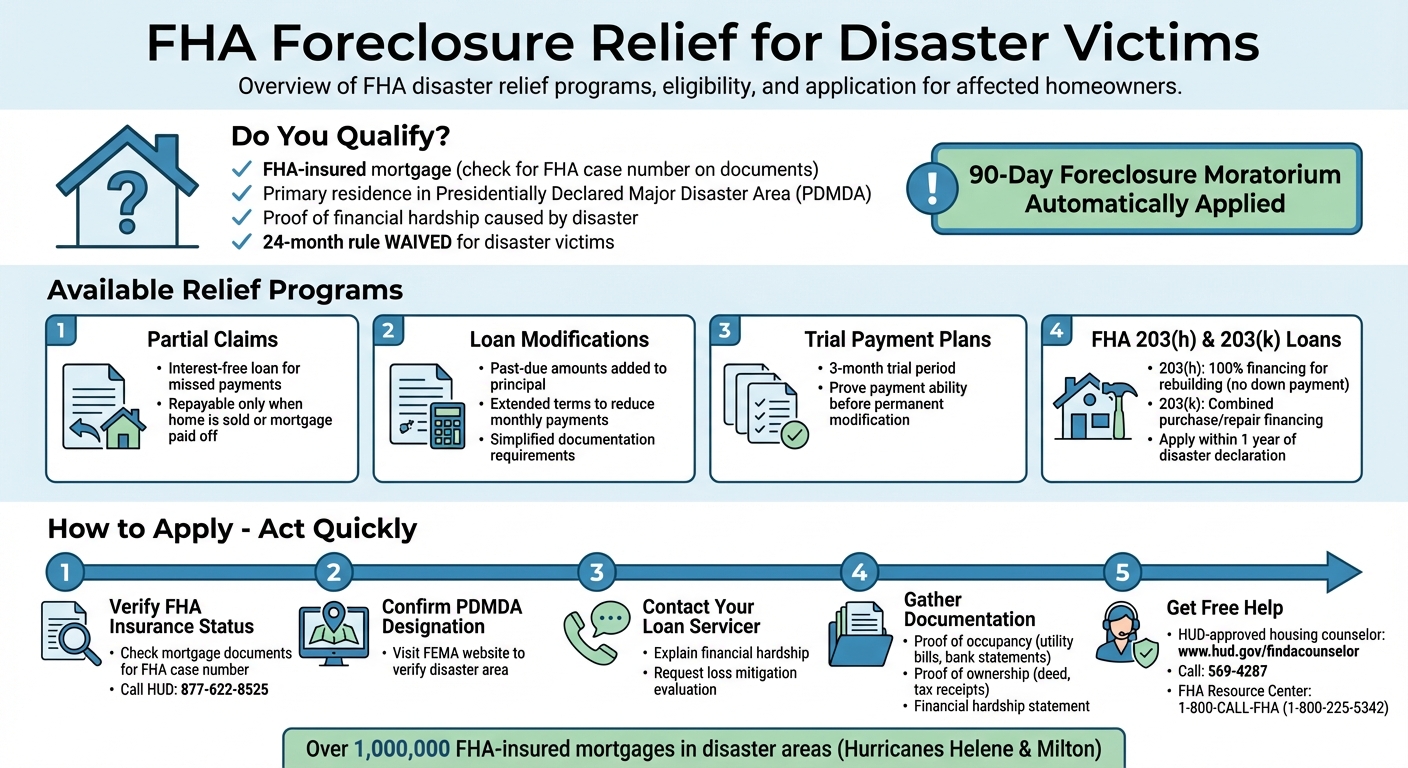

When natural disasters strike, homeowners with FHA-insured mortgages in federally declared disaster areas can access foreclosure relief programs. These programs aim to provide financial breathing room and support recovery efforts. Key measures include:

- 90-day foreclosure moratorium: Stops foreclosure actions for affected properties.

- Partial claims: Interest-free loans to cover missed payments, repayable upon sale or payoff of the mortgage.

- Loan modifications: Adjust loan terms to reduce monthly payments.

- Trial payment plans: A three-month period to prove payment ability before finalizing a loan adjustment.

Eligibility requires an FHA-insured mortgage, primary residence in a disaster zone, and proof of financial hardship. Homeowners can also explore FHA 203(h) loans for rebuilding or FHA 203(k) loans for repairs. Check your FHA status and disaster area designation, then contact your loan servicer or HUD-approved housing counselor for assistance.

Act quickly to secure relief and protect your home.

FHA Disaster Relief Programs: Eligibility Requirements and Application Process

FHA Loss Mitigation Changes

sbb-itb-d613a70

What is FHA Foreclosure Relief for Natural Disaster Victims?

FHA foreclosure relief is designed to help homeowners in areas declared as Presidentially-Declared Major Disaster Areas (PDMDAs) recover after natural disasters. One of the first steps taken is an immediate halt to all foreclosure actions. This pause gives homeowners the breathing room they need to assess property damage and work with their lenders to create a recovery plan.

In addition to the foreclosure moratorium, FHA offers a range of relief options tailored to the needs of disaster victims:

- Partial claims: These allow homeowners to defer the amount needed to bring their mortgage current. The deferred balance is treated as an interest-free loan, repayable only when the property is sold or the mortgage is paid off.

- Loan modifications: Past-due amounts can be added to the loan principal, and terms can be extended to reduce payments. In many cases, standard financial documentation isn’t required.

- Trial payment plans: Homeowners can enter a three-month trial period to demonstrate their ability to make payments before finalizing a permanent loan modification.

"FHA requires an immediate moratorium on foreclosures in PDMDAs, which includes foreclosures that have not started and foreclosures in process." – Steve Sharpe, Senior Attorney, National Consumer Law Center

FHA also lifts the typical 24-month limit on loss mitigation solutions for those affected by disasters. While some relief options, such as modifications and partial claims, may not require extensive financial documentation, a three-month trial payment plan might still be necessary.

To determine if you’re eligible for these protections, confirm that your loan is FHA-insured. You can do this by checking for an FHA case number on your mortgage documents or looking for FHA premium payments on your monthly statements. If you’re unsure, you can call HUD’s National Servicing Center at 877-622-8525 for assistance. Keep in mind, these protections only apply if your property is located within a PDMDA.

Who Qualifies for FHA Disaster Assistance?

To be eligible for FHA disaster assistance, you must have an active FHA-insured mortgage on your primary residence located in a Presidentially Declared Major Disaster Area (PDMDA). Additionally, you need to demonstrate financial hardship caused by the disaster, such as job loss, reduced income, or medical expenses. FHA has also waived its usual 24-month rule, which limits borrowers to one permanent loss mitigation option every two years, allowing access to multiple assistance programs. Below, you’ll find details about foreclosure moratoriums and the necessary documentation to apply for relief.

Requirements for FHA Foreclosure Moratoriums

If you meet the criteria for FHA disaster assistance, specific foreclosure moratorium rules come into play. Following a Presidential disaster declaration, FHA enforces a 90-day moratorium on foreclosure for all FHA-insured mortgages. This includes Single Family Title II forward loans and Home Equity Conversion Mortgages (HECMs). The moratorium halts both the initiation and completion of foreclosure actions, even for mortgages that were already delinquent before the disaster.

"FHA implemented automatic 90-day foreclosure moratoriums that required mortgage servicers to halt the initiation or completion of all foreclosure actions in PDMDAs on the date that each disaster was declared." – HUD News Release

In some cases, HUD may grant an additional 180-day extension to foreclosure deadlines, giving servicers more time to assist borrowers.

Required Documentation for FHA Disaster Relief

FHA keeps the documentation process straightforward to confirm eligibility. FEMA and HUD use automated public records to verify homeownership and occupancy. If this automated process fails, you’ll need to provide digital copies of documents to prove occupancy (like utility bills, bank statements, or a driver’s license dated before the disaster) and ownership (such as a deed, mortgage documents, property tax receipts, or homeowners insurance records). These can be submitted via DisasterAssistance.gov. If original documents were lost, you can request replacements from the appropriate agencies.

You must also submit a statement explaining your financial hardship and how the disaster impacted your ability to make payments. For those unable to provide standard documentation – such as individuals living on tribal lands or in mobile homes – a written self-declarative statement may be accepted to verify occupancy or ownership as a last resort.

Main FHA Programs for Disaster Victims

Now that eligibility and documentation requirements are clear, let’s look at two key loan programs offered by the FHA to aid disaster recovery. These programs are designed to help homeowners rebuild or repair their homes after a natural disaster. The FHA 203(h) program focuses on financing for those needing to replace or rebuild their homes entirely, while the FHA 203(k) program supports homeowners in repairing or renovating damaged properties. Both are exclusively available to those living in Presidentially Declared Major Disaster Areas (PDMDAs) and can be used together to provide more comprehensive recovery options.

FHA 203(h) Loan Program

The FHA 203(h) program is tailored for homeowners whose primary residences were destroyed or severely damaged in a declared disaster. What makes this program stand out is its 100% financing – no down payment is required. This allows you to purchase a new home or rebuild your existing one without upfront costs. It’s available to both first-time and repeat buyers, as long as the property will serve as your primary residence.

Applications must be submitted within one year of the disaster declaration, though extensions may be granted in some cases. Lenders offering this program often provide flexible credit requirements, taking into account the financial challenges caused by the disaster. While FHA loans generally require a minimum credit score of 500, most lenders set higher thresholds for the 203(h) program, typically 580 or 620.

You can also purchase a home outside the original disaster area, provided it falls within FHA loan limits. However, this program cannot be used for multi-unit properties, manufactured homes, co-ops, or investment properties. Borrowers are responsible for paying both an upfront and annual Mortgage Insurance Premium (MIP), just like with standard FHA loans. For example, FHA insured over one million single-family mortgages in disaster areas impacted by Hurricanes Helene and Milton.

If your property needs repairs rather than a full rebuild, the FHA has another option for you.

FHA 203(k) Loan Program for Home Repairs

The FHA 203(k) program is designed to help homeowners in PDMDAs finance both the purchase (or refinancing) of a home and the costs of its repair or renovation – all through a single mortgage. This program is ideal if your property has sustained damage or if you’re looking to buy a home that requires significant work. It covers a range of upgrades, including structural repairs, system modernizations, and essential health and safety improvements.

To use this program, you’ll need to work with an FHA-approved lender. For additional guidance, you can consult a HUD-approved housing counseling agency. HUD provides an online search tool at www.hud.gov/findacounselor or you can call 569-4287 for assistance.

"Today’s action will allow more flexibility as our fellow Americans continue working to stabilize their families, properties and communities".

This program complements other recovery efforts by addressing immediate repair needs, helping homeowners restore their properties after a disaster.

How to Apply for FHA Foreclosure Relief Programs

Taking quick action is essential when recovering from a disaster. Start by confirming that your mortgage is FHA-insured. Look for an FHA case number or insurance premiums on your mortgage statements. Then, verify that your property is in a Presidentially-Declared Major Disaster Area by checking the FEMA website. FHA relief programs are only available for properties in these designated zones. Once you’ve confirmed eligibility, your next step is to contact your mortgage servicer.

Reach out to your servicer without delay. They’ll evaluate your situation using their loss mitigation process. Thanks to recent FHA updates, the documentation requirements have been simplified. You’ll need to provide proof of financial hardship and confirm that the property is your primary residence.

For additional help, consider speaking with a HUD-approved housing counselor. These counselors offer unbiased, free assistance and can guide you through the application process while working with your servicer. Foreclosure prevention counseling is always free. You can find a counselor by visiting www.hud.gov/findacounselor or calling 569-4287.

If you’re applying for an FHA 203(h) loan, make sure to do so within one year of the disaster declaration. For many permanent relief options, you’ll need to complete a three-month trial payment plan to show you can resume regular payments. Keep in mind that forbearance extensions are not automatic – you’ll need to request them directly from your loan servicer.

If you need more guidance or have questions, contact the FHA Resource Center at 1-800-CALL-FHA (1-800-225-5342) or email them at answers@hud.gov. Taking these steps promptly can make a significant difference in securing the relief you need.

How Foreclosure Defense Group Can Help

When navigating FHA relief processes feels overwhelming, having legal support can make all the difference. FHA disaster relief procedures can be tricky to understand, especially in the aftermath of a disaster. That’s where Foreclosure Defense Group steps in, offering expert legal guidance to help you understand FHA loss mitigation options and protect your rights. Plus, they provide free consultations, giving you a chance to discuss your case and explore your options without any pressure.

If your loan servicer fails to honor HUD-mandated foreclosure protections, you may have the right to challenge their actions. Attorney Amy Loftsgordon from the University of Denver Sturm College of Law highlights this point:

"Many courts have said that a servicer’s failure to comply with HUD guidelines provides a defense to a foreclosure".

Foreclosure Defense Group works to ensure these protections are upheld, holding servicers accountable when they fall short of federal requirements.

The firm also helps with the tricky details that can complicate relief applications. For instance, if you’re dealing with an absent co-borrower due to a death or divorce, their legal expertise can help you qualify for loan modifications under HUD’s updated guidelines. They also assist disaster victims in accessing specific waivers, like exceptions allowing more than one permanent loss mitigation option within a 24-month period. This kind of support ensures you have access to fair solutions during tough recovery periods.

If keeping your home isn’t possible, Foreclosure Defense Group can guide you through alternatives like short sales or deeds in lieu of foreclosure, helping you avoid deficiency judgments. Beyond foreclosure defense, they also offer assistance with bankruptcy, loan modifications, and forbearance. Their approach is tailored to your unique situation, ensuring you understand every available option and receive the representation you need during this challenging time.

To take the next step, visit foreclosuredefensegroup.com and schedule your free consultation. Their team is ready to help you secure the FHA disaster relief you’re entitled to.

Protecting Your Home After a Disaster

When disaster strikes, every minute counts. Start by filing an insurance claim as soon as possible, and notify your mortgage servicer about the disaster and any financial difficulties you’re facing. Make sure to get written confirmation of any relief plan they offer. Even if your home is uninhabitable, keep making required mortgage payments until you have a written agreement for relief.

After addressing immediate recovery needs, check if you qualify for FHA disaster protections. First, confirm that your loan is FHA-insured and that your property is in a federally designated disaster area. For example, HUD has previously provided foreclosure moratoriums in major disaster zones, giving homeowners extra time to recover financially. These protections are part of FHA’s broader disaster relief efforts.

To stabilize your financial footing further, consider federal programs and other assistance. Register with FEMA for housing aid, which may help with temporary rent or repair costs that your insurance doesn’t cover. Always maintain your mortgage payments unless you have a documented agreement, as missed payments can damage your credit. Keep a detailed record of all communications, including the names of representatives and dates of discussions.

FHA disaster relief includes simplified processes, such as waiving the usual 24-month limit on permanent loss mitigation options. Additionally, HUD-approved housing counseling services are available at no cost to guide you through these programs. With over 1,000,000 FHA-insured single-family mortgages in disaster areas, these protections are designed to help homeowners stay in their homes.

If the process feels overwhelming or your mortgage servicer isn’t cooperating, professional legal assistance can help protect your rights. You can visit foreclosuredefensegroup.com to schedule a free consultation and get the support you need to secure the FHA disaster relief you’re entitled to.

Related Blog Posts

- Checklist: FHA Foreclosure Relief Eligibility

- California Mortgage Relief Program Overview

- 5 Government Programs to Avoid Foreclosure

- FHA Loan Modification: Application Process Simplified