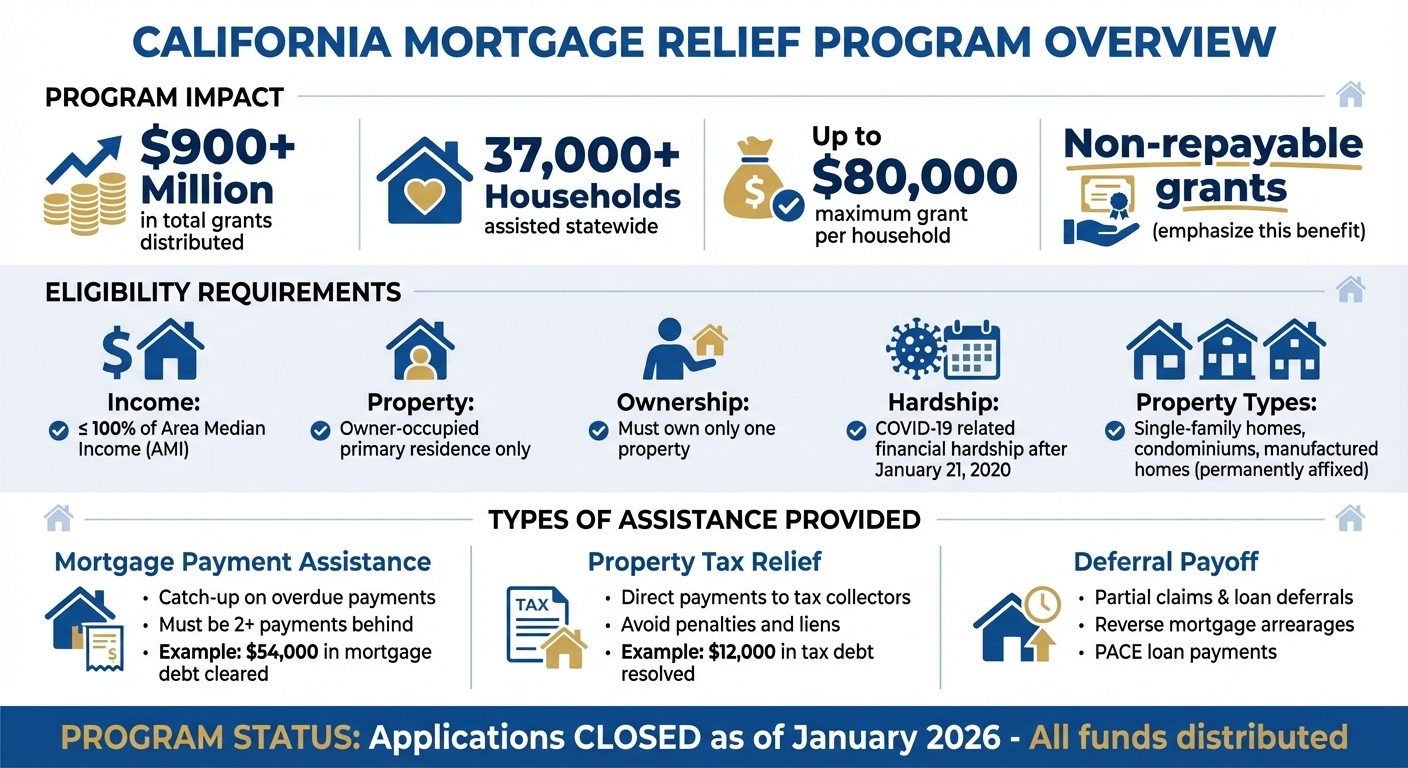

The California Mortgage Relief Program provided up to $80,000 in non-repayable grants per household to help Californians manage overdue mortgage payments, property taxes, and other housing-related debts. Funded by ARPA‘s Homeowner Assistance Fund, it supported over 37,000 households by early 2026, preventing foreclosures and stabilizing families during financial hardships.

Key details:

- Eligibility: Income ≤ 100% of Area Median Income, owner-occupied primary residence, pandemic-related financial hardship after January 21, 2020.

- Types of Assistance: Mortgage payment catch-up, property tax relief, and payoff of deferred payments or reverse mortgage arrears.

- Status: Applications closed as of January 2026; all funds distributed.

For ongoing support, homeowners should contact a HUD-certified housing counselor at 1-800-569-4287 or explore legal aid options like foreclosure defense and loan modifications.

California Mortgage Relief Program Key Statistics and Eligibility Requirements

Eligibility Requirements

Income and Property Ownership Criteria

The California Mortgage Relief Program outlined specific qualifications for those seeking assistance. To qualify, a household’s total income – including all members aged 18 and older – could not exceed 100% of the county’s Area Median Income (AMI).

"Only people who own and occupy one property and make at or below 100% of their area median income will be eligible." – Gov. Gavin Newsom

Applicants were required to own and live in a single primary residence. Properties like vacation homes or investment properties did not qualify. Eligible residences included single-family homes, condominiums, and manufactured homes that were permanently attached to land and taxed as real estate.

| Criteria | Requirement Details |

|---|---|

| Income Limit | ≤ 100% of Area Median Income (AMI) |

| Occupancy | Must be owner-occupied primary residence |

| Property Ownership | Must own only one property |

| Eligible Structures | Single-family, condominium, or manufactured (affixed) |

Qualified Financial Hardships

Beyond income and property guidelines, applicants had to show financial hardship directly tied to the COVID-19 pandemic. These hardships needed to have occurred after January 21, 2020, and could include job loss, reduced work hours, or increased healthcare expenses caused by the pandemic. Demonstrating that the pandemic was the direct cause of the hardship was essential.

For mortgage payment assistance, homeowners typically needed to be at least two payments behind when they applied. Later, the program expanded to include those facing disaster-related hardships. This included homeowners whose properties were destroyed or severely damaged by qualified disasters such as the Eaton Fire, Palisades Fire, Park Fire, or San Diego floods, which occurred between January 1, 2023, and January 8, 2025.

Types of Assistance Provided

Mortgage Payment Assistance

This program offered grants to help homeowners catch up on overdue mortgage payments. To qualify, homeowners needed to be at least two payments behind as of December 27, 2021. The funds were sent directly to the mortgage servicer, bringing the mortgage account up to date.

Angela Morrow, a flight attendant from San Bernardino County, benefited from this program by clearing over $54,000 in mortgage debt. This not only reduced her monthly payments but also helped her avoid foreclosure in Bloomington. Similarly, Maurice, a homeowner from Los Angeles County, was "days away from the foreclosure sale" when a grant enabled him to get current on his mortgage and keep the home he had lived in for 23 years.

"Over 20,000 homeowners have already gotten help with late mortgage payments, missed property taxes and partial claims loan deferrals taken during the pandemic." – Rebecca Franklin, President, CalHFA Homeowner Relief Corp.

Along with mortgage payment assistance, the program extended support for other pressing financial needs.

Property Tax Relief

The program also addressed overdue property taxes by providing direct payments to tax collectors. This assistance helped homeowners avoid penalties, interest charges, and potential tax liens that could lead to property loss.

For example, Eloy Anthony Garcia, a Los Angeles resident with a home in Palm Springs, received $12,000 in assistance to resolve his property tax debt. After checking the City of Palm Springs website, he confirmed the debt was cleared, saving his property from potential loss.

Partial Claim or Deferral Payoff Options

The program tackled "partial claims" and "loan deferrals" (commonly known as "silent seconds") that many homeowners had taken during or after January 2020 to cope with pandemic-related financial challenges. Grants were provided to settle these deferred payments – amounts moved to the end of a loan term during forbearance – helping to restore equity and eliminate future financial burdens.

Additionally, the program covered reverse mortgage arrearages, enabling seniors to keep their homes, and cleared overdue PACE (Property Assessed Clean Energy) loan payments. All assistance was provided as non-repayable grants, with a maximum limit of $80,000 per household. Homeowners could use various forms of assistance, provided the combined total remained within this cap.

How to Apply

Step-by-Step Application Process

As of early 2026, the California Mortgage Relief Program stopped accepting applications after distributing all available federal funding.

Before the program closed, homeowners could apply through the official website at camortgagerelief.org. The process began with a brief questionnaire to determine eligibility, which required applicants to have an income at or below 100% of their county’s Area Median Income (AMI) and to demonstrate a pandemic-related financial hardship that started after January 21, 2020. Once eligibility was confirmed, applicants had 30 days to submit a complete application. This included documents like mortgage statements, bank and utility bills, and proof of income. Decisions were usually made within 30 days, and approved funds were sent directly to mortgage servicers or tax collectors to ensure timely payments.

"I appreciated the efficient process and prompt responses. The funds were paid directly to the mortgage company in a timely manner." – Ana, Homeowner

Although this program is no longer available, there are still resources for homeowners who need assistance.

Where to Get Help with Applications

With the program now closed, homeowners dealing with mortgage issues can reach out to a HUD-certified housing counselor by calling 1-800-569-4287. These counselors provide free assistance with foreclosure prevention, debt management, and other housing-related concerns. For those affected by specific events, such as the 2025 Los Angeles fires, alternatives like the CalAssist Mortgage Fund or extended forbearance under AB 238 may be available.

For legal help, organizations like Foreclosure Defense Group (https://foreclosuredefensegroup.com) offer support with foreclosure defense, loan modifications, and bankruptcy proceedings. Homeowners are also encouraged to contact their mortgage servicer directly to explore relief or forbearance options. Additionally, online tools can help borrowers check if their loan is backed by Fannie Mae or Freddie Mac, which may unlock further assistance opportunities.

sbb-itb-d613a70

California Mortgage Relief Program Offers $80,000 Grants to Help People Meet Mortgage Payments

Other Legal and Financial Support Options

When government programs run their course, there are still other ways to protect your home through legal and financial assistance.

Foreclosure Defense Services

Having legal representation can make a big difference when facing foreclosure. Foreclosure defense attorneys can review your mortgage documents for mistakes, spot violations of state or federal laws, and even negotiate with lenders to delay or stop foreclosure proceedings. This extra time can be crucial for finding alternative solutions.

For example, Foreclosure Defense Group (https://foreclosuredefensegroup.com) provides legal help to homeowners in California. Their services include free consultations to review your case, court representation, and guidance on your legal rights throughout the process. With a foreclosure defense attorney on your side, you can ensure lenders follow proper procedures and avoid being taken advantage of during a stressful time.

In addition to foreclosure defense, exploring options like loan modification can help make payments more manageable.

Loan Modification and Forbearance

Loan modification is a permanent change to your mortgage terms, designed to make payments more affordable. This could involve lowering your interest rate, switching from a variable to a fixed rate, extending the loan term up to 40 years, or deferring part of the principal. If your loan is eligible under the Fannie Mae or Freddie Mac Flex Modification program, you could see a 20% reduction in your monthly payment. To check if your loan qualifies, use the Fannie Mae or Freddie Mac "Loan Lookup" tools.

For a temporary solution, a forbearance agreement can reduce or pause your mortgage payments. Homeowners with federally backed loans can request a 180-day extension if they’re facing financial hardship. Once the forbearance period ends, you’ll need to repay the deferred amount. Repayment options include a lump sum, a short-term repayment plan (usually 3, 6, or 9 months), or adding the amount to the end of your loan.

If these options fall short, bankruptcy might provide a structured way to manage overwhelming debt.

Bankruptcy Assistance

Bankruptcy is often considered a last resort for homeowners in severe financial trouble. Filing for Chapter 13 bankruptcy allows you to reorganize your debts and establish a repayment plan over three to five years. This can halt foreclosure proceedings and give you time to catch up on missed payments. On the other hand, Chapter 7 bankruptcy doesn’t save your home long-term, but it can eliminate other debts, freeing up income to address your mortgage.

"Free legal services are available to homeowners who aren’t able to afford them. These services are intended to help homeowners seeking legal advice on matters relating to preserving sustainable homeownership." – CalHFA

Low-income homeowners in California can access free legal help through Qualified Legal Services Projects (QLSPs) and Qualified Support Centers (QSCs). These organizations provide advice on foreclosure prevention, mortgage servicing, and bankruptcy. For additional guidance, you can also contact a HUD-approved mortgage counselor at 800-569-4287 for free assistance with foreclosure alternatives.

Conclusion

The California Mortgage Relief Program provided over $900 million in grants, offering up to $80,000 per household to assist 37,000 households statewide. While the program has stopped accepting new applications, its impact highlights the power of direct financial aid in helping homeowners regain stability. As Tony, a recipient of the program, expressed: "I am so relieved, pleased and grateful for your assistance. This has taken a huge weight off my shoulders and is the reset that I needed". Though this program has ended, other resources are still available to those in need.

If you’re dealing with foreclosure or mortgage difficulties, a HUD-certified housing counselor can provide free assistance. Call 800-569-4287 for advice on loan modifications, forbearance agreements, or other debt-relief options. For legal support, the Foreclosure Defense Group (https://foreclosuredefensegroup.com) offers free consultations and experienced help with court defense, loan modifications, and bankruptcy solutions.

Don’t wait – taking action early can open more doors and help secure your home’s future.

FAQs

Who qualifies for the California Mortgage Relief Program?

To be eligible for the California Mortgage Relief Program, you must meet these key criteria:

- Residency and Property Use: You must own a home in California and use it as your primary residence.

- Financial Hardship: You need to have faced financial difficulties due to the pandemic or a qualifying disaster.

- Missed Payments: You must be behind on mortgage, property tax, or reverse mortgage payments.

- Income Limits: Your household income must be at or below 100% of your county’s Area Median Income (AMI). For instance, in Los Angeles County, the income limit is up to $211,050.

The program is designed to help homeowners stay in their homes by addressing missed payments and providing financial relief tailored to individual circumstances.

How does the California Mortgage Relief Program assist with overdue mortgage payments?

The California Mortgage Relief Program provides free, non-repayable grants of up to $80,000 for qualifying homeowners. These grants are intended to help cover overdue mortgage payments, giving homeowners a chance to catch up financially without adding the stress of repayment.

This initiative focuses on helping those experiencing financial difficulties, offering support to ensure they can remain in their homes without the added burden of repayment.

What can homeowners do now that the California Mortgage Relief Program has ended?

If the California Mortgage Relief Program is no longer an option, there are still ways for homeowners to navigate financial hurdles. One effective step is connecting with a HUD-certified housing counselor. They can offer tailored advice and help you explore various options like payment plans, special forbearance agreements, temporary interest rate reductions, or loan modifications through programs such as CalHFA.

For those at risk of foreclosure, reaching out to a legal professional can be a game-changer. Experts, like the team at Foreclosure Defense Group, specialize in safeguarding your rights and identifying solutions that fit your needs, whether that’s foreclosure defense or restructuring your loan. Acting promptly can be crucial in overcoming financial challenges and securing your home.

Related Blog Posts

- Top 4 Mortgage Relief Programs in Florida for 2025

- Short Sale Document Requirements Explained

- Government Loan Modifications: Solving Foreclosure Risks

- Checklist: FHA Foreclosure Relief Eligibility