Refinancing your mortgage can save money in the long run, but it comes with upfront costs, including origination fees. These fees, typically 0.5% to 1.5% of the loan amount, cover lender services like underwriting and document preparation. For example, a 1% fee on a $300,000 loan equals $3,000.

Here’s what you need to know:

- Origination fees are negotiable. Strong credit or shopping around can help lower costs.

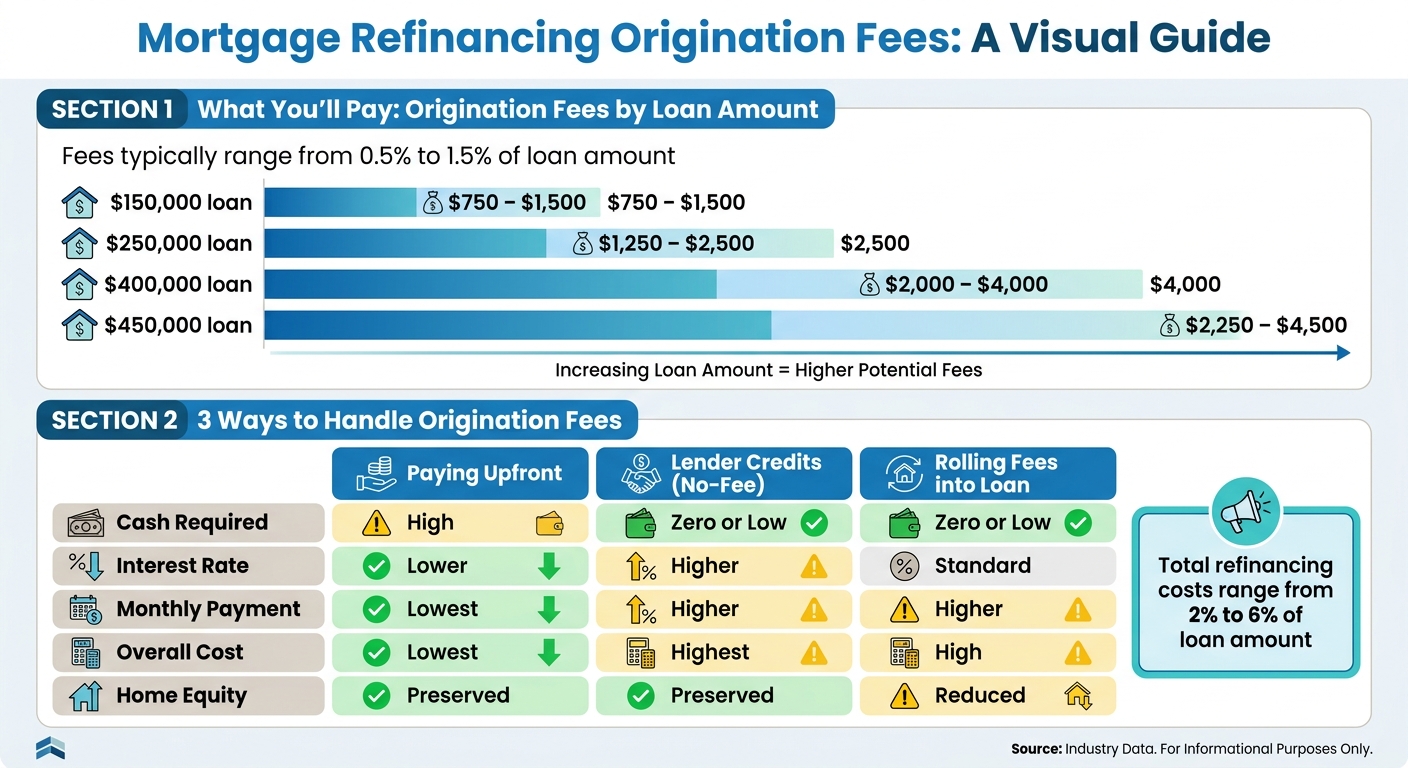

- Total refinancing costs range from 2% to 6% of the loan amount, with origination fees making up a portion.

- Some lenders offer no-origination fee loans, but these often come with higher interest rates.

- Break-even point: Calculate how long it takes for monthly savings to offset upfront fees.

Understanding and negotiating these fees can help you make smarter refinancing decisions.

What Is a Mortgage Origination Fee?

sbb-itb-d613a70

How Origination Fees Work

Mortgage Origination Fees by Loan Amount and Payment Options Comparison

Understanding what you’re paying for when you see "origination fee" on your loan estimate can help you make better refinancing decisions. Knowing these details gives you the chance to negotiate and potentially lower your overall refinancing costs.

What Origination Fees Cover

Origination fees account for the work involved in taking your mortgage from application to closing. This includes underwriting, document preparation, and various administrative tasks. As Alexei Morgado, REALTOR® and CEO of Lexawise, puts it:

"Basically, they cover all the behind-the-scenes effort that goes into getting your mortgage from application to close."

Underwriting is the biggest part of this fee. It involves assessing your risk as a borrower, verifying your employment, and evaluating the property’s value. Document preparation is another key component – it includes creating loan estimates, promissory notes, and closing disclosures. On top of that, administrative work like verifying income documents, conducting title searches, and ensuring compliance with lending regulations is also included.

Some lenders break these services down on your loan estimate, while others combine them into a single charge. Either way, origination fees compensate the lender for processing and funding your loan.

How Lenders Calculate Origination Fees

Lenders typically calculate origination fees as a percentage of the loan amount. For refinancing, these fees can go as high as 1.5%. For instance, a $250,000 loan with a 1% origination fee would cost $2,500, while a $400,000 loan would result in a $4,000 fee.

Several factors can influence how much you’ll pay. Smaller loan amounts may have higher percentages due to fixed administrative costs. Your credit score and financial profile also matter – borrowers with non-traditional income or self-employment might face higher fees. The type of lender can also make a difference. Online lenders sometimes waive origination fees to stay competitive, whereas traditional banks tend to stick to standard rates.

The type of loan you’re applying for further impacts the fee structure. For example:

- VA loans: Origination fees are legally capped at 1% of the loan amount.

- FHA loans: Fees typically range from 0.5% to 1%, though certain programs like the 203(k) may allow up to 2%.

- USDA loans: Fees usually fall between 0% and 1%, especially for borrowers in rural, low-to-moderate income brackets.

Average Origination Fee Costs

Here’s a breakdown of typical origination fee ranges based on loan amounts:

| Loan Amount | Typical Origination Fee Range |

|---|---|

| $150,000 | $750 – $1,500 |

| $250,000 | $1,250 – $2,500 |

| $400,000 | $2,000 – $4,000 |

| $450,000 | $2,250 – $4,500 |

In Florida, for example, total closing costs – including origination fees – can vary widely. As of January 2026, HomeAmerican Mortgage Corp. had an average closing cost of $1,160, while A&D Mortgage LLC averaged $16,256. This massive variation highlights the importance of comparing lenders, as shopping around could save you thousands.

A 2024 survey found that 66% of homebuyers cited the loan origination fee as the most unexpected cost. Understanding these ranges can help you evaluate whether a lender’s quote is reasonable or overpriced.

How to Reduce Origination Fees

Origination fees are negotiable since lenders control these fees directly. Unlike charges like appraisals or credit reports, which are set by third parties, lenders may agree to lower origination fees – if you know how to approach them.

Negotiate with Your Lender

If you have a strong financial profile, you’re in a good position to negotiate. Borrowers with excellent credit scores, substantial home equity, and low debt-to-income ratios have more leverage to request fee reductions. Lenders may also be more flexible during periods when they need more customers, such as when their production pipeline is slow.

Start by asking for an itemized breakdown of all origination charges. This will help you spot unnecessary or duplicate fees. If you’ve recently refinanced, check with your title company about a "reissue rate" discount on title insurance, which could save you 20% to 40%.

Your current mortgage provider might offer loyalty discounts to retain your business. Don’t hesitate to ask directly, "Can you reduce or waive the origination fee to keep me as a customer?". Keep in mind, however, that government-backed loans like FHA, VA, and USDA loans often have more standardized fees, leaving less room for negotiation compared to conventional loans.

Once you’ve negotiated with your lender, the next step is to shop around for better offers.

Compare Multiple Lenders

Comparing offers from different lenders is one of the most effective ways to save money. Surprisingly, about 47% of borrowers don’t shop around, potentially missing out on significant savings. By getting quotes from multiple lenders, you could improve your refinance rate by as much as 0.5%.

Request Loan Estimates from at least three to five lenders, including your current mortgage provider, online lenders, and local credit unions. Pay close attention to Section A of the Loan Estimate, which outlines origination charges, processing fees, and underwriting costs. On a $300,000 refinance, origination fees can differ by as much as $2,000 between lenders.

Use these competing offers to your advantage. Steven Parangi, a Licensed Mortgage Loan Originator, advises:

"Comparison is key. Get quotes from multiple lenders. When you have competitive offers in hand you can show a lender you are seriously considering other options and ask them to match or beat the terms, including the origination fees."

To protect your credit score, ensure all applications are completed within a 14- to 45-day period so multiple inquiries count as a single hard pull. Keep in mind that fee structures vary among lenders – online lenders often charge less (or even $0), while traditional banks may have higher fees but offer loyalty discounts.

If these strategies don’t yield the lowest fees, you might explore no-origination fee loans as an alternative.

No-Origination Fee Loans: Pros and Cons

If negotiating or comparing lenders doesn’t reduce fees enough, no-origination fee loans could be worth considering. These loans eliminate upfront costs at closing, but they come with trade-offs.

The catch? These loans often come with higher interest rates. Lenders use "lender credits" to cover the fees, which increases the overall cost over the life of the loan. Alternatively, some lenders may roll the fees into your mortgage principal, which reduces your home equity and increases your monthly payments.

To decide if this option is right for you, focus on the Annual Percentage Rate (APR) listed on page 3 of the Loan Estimate. Unlike the interest rate, the APR reflects the total cost, including upfront fees. You can also calculate your break-even point by multiplying the monthly payment difference by the length of time you plan to stay in the home. If you’ll stay for five years or longer, paying the origination fee upfront usually saves money. But if you plan to sell or refinance within three to five years, a no-fee loan might be the smarter choice.

| Feature | Paying Upfront | Lender Credits (No-Fee) | Rolling Fees into Loan |

|---|---|---|---|

| Cash Required | High | Zero or Low | Zero or Low |

| Interest Rate | Lower | Higher | Standard |

| Monthly Payment | Lowest | Higher | Higher |

| Overall Cost | Lowest | Highest | High |

| Home Equity | Preserved | Preserved | Reduced |

Common Myths About Origination Fees

Misunderstanding origination fees can lead to costly mistakes. Knowing the facts equips you to better assess lender fees as you navigate refinancing.

Myth: Origination Fees Are Fixed

Contrary to popular belief, origination fees aren’t set in stone. They vary depending on the lender and your financial profile. Borrowers with strong credit, high income, or large loan amounts often have more room to negotiate fees – or even have them waived. On the other hand, smaller loans may come with higher percentage fees due to fixed administrative costs. Some lenders also offer flat fees or loans with no origination fees, though these typically come with higher interest rates.

Myth: Higher Fees Mean Better Service

Paying more doesn’t necessarily mean you’re getting better service. Many online lenders and credit unions provide competitive service while charging lower – or even zero – origination fees. High fees can often be avoided by shopping around or simply negotiating.

However, there are cases where higher fees might reflect added value. As Steven Parangi, a Real Estate Attorney and Mortgage Loan Originator, points out:

"Sometimes a more experienced lender may charge a slightly higher origination fee but have the expertise to find better loan programs or handle complex situations that will save you money over the life of the loan."

To get a full picture of loan costs, comparing APRs is essential. Unlike interest rates alone, APRs include origination fees and other closing costs, giving you a clearer sense of the total expense.

Myth: Origination Fees Are the Only Cost

Origination fees are just one part of the closing cost puzzle. Total closing costs usually range from 2% to 6% of the loan amount. These costs include lender fees (often negotiable), third-party fees (usually fixed), government recording fees, and prepaid items. For example, on a $300,000 refinance, total closing costs typically fall between $6,000 and $18,000, with origination fees making up about $1,500 to $3,000 of that total.

Understanding the full scope of closing costs can help you weigh whether a no-origination-fee loan is truly a better deal – or if it simply shifts the expense into a higher interest rate.

Key Points to Remember

Understanding how to manage origination fees can make a big difference in keeping refinancing costs under control.

Managing Your Origination Fees

Origination fees, which typically range from 0.5% to 1.5% of your loan amount, are negotiable. For instance, on a $400,000 refinance, these fees could amount to $2,000 to $4,000. By gathering multiple Loan Estimates, you can use competing offers to push for lower fees – potentially saving up to $2,000.

Focus on Section A of your Loan Estimate, which outlines origination, processing, and application fees. Additionally, ask your current lender about loyalty discounts; they may lower fees to keep your business. Borrowers with strong financial profiles, such as those with a credit score of 780+ and significant home equity, often receive better terms.

Understanding your break-even point is also critical. If you plan to move or refinance again in a few years, a no-origination-fee loan could save you money, even with a slightly higher interest rate (usually about 0.25% more).

By combining these strategies, you can take charge of your refinancing costs and make more informed decisions.

Get Professional Help

Once you’ve negotiated fees, consulting a professional can provide added clarity and security. Refinancing involves long-term financial decisions, and expert advice can help you weigh options like paying fees upfront versus accepting a higher interest rate. Professionals can also identify which lender fees are negotiable, calculate cost–benefit scenarios, and tailor strategies to your specific needs.

For homeowners facing financial challenges or potential foreclosure while exploring refinancing, organizations like Foreclosure Defense Group (https://foreclosuredefensegroup.com) offer specialized legal assistance. Their experienced attorneys can help protect your home, navigate loan modifications, and manage refinancing costs effectively.

FAQs

Where do I find origination fees on my Loan Estimate?

Origination fees appear under the closing costs section of your Loan Estimate. These fees represent what your lender charges for processing and underwriting your loan. Take a close look at this section to see the cost breakdown and confirm everything is accurate.

Are discount points the same as origination fees?

No, discount points and origination fees are not the same.

- Origination fees cover the costs of processing and underwriting your loan. These are usually between 0.5% and 1% of the loan amount.

- Discount points, on the other hand, are optional. They’re paid upfront to reduce your loan’s interest rate. Typically, one discount point equals 1% of the loan amount and can lower the interest rate by about 0.25%.

While both are upfront expenses, they serve very different purposes.

Can I roll origination fees into my refinance loan?

Yes, many lenders let you include origination fees in your refinance loan, but this depends on the lender’s policies and the specific loan program. Some lenders allow these fees to be added to the loan balance, helping you avoid upfront costs. Others might require you to pay them at closing. It’s important to check with your lender to understand their terms before moving forward.

Related Blog Posts

- How to Refinance from ARM to Fixed-Rate Mortgage

- Top Refinancing Mistakes with Escrow Fees

- Top Legal Protections Against Predatory Lending

- Top Refinancing Options for Poor Credit