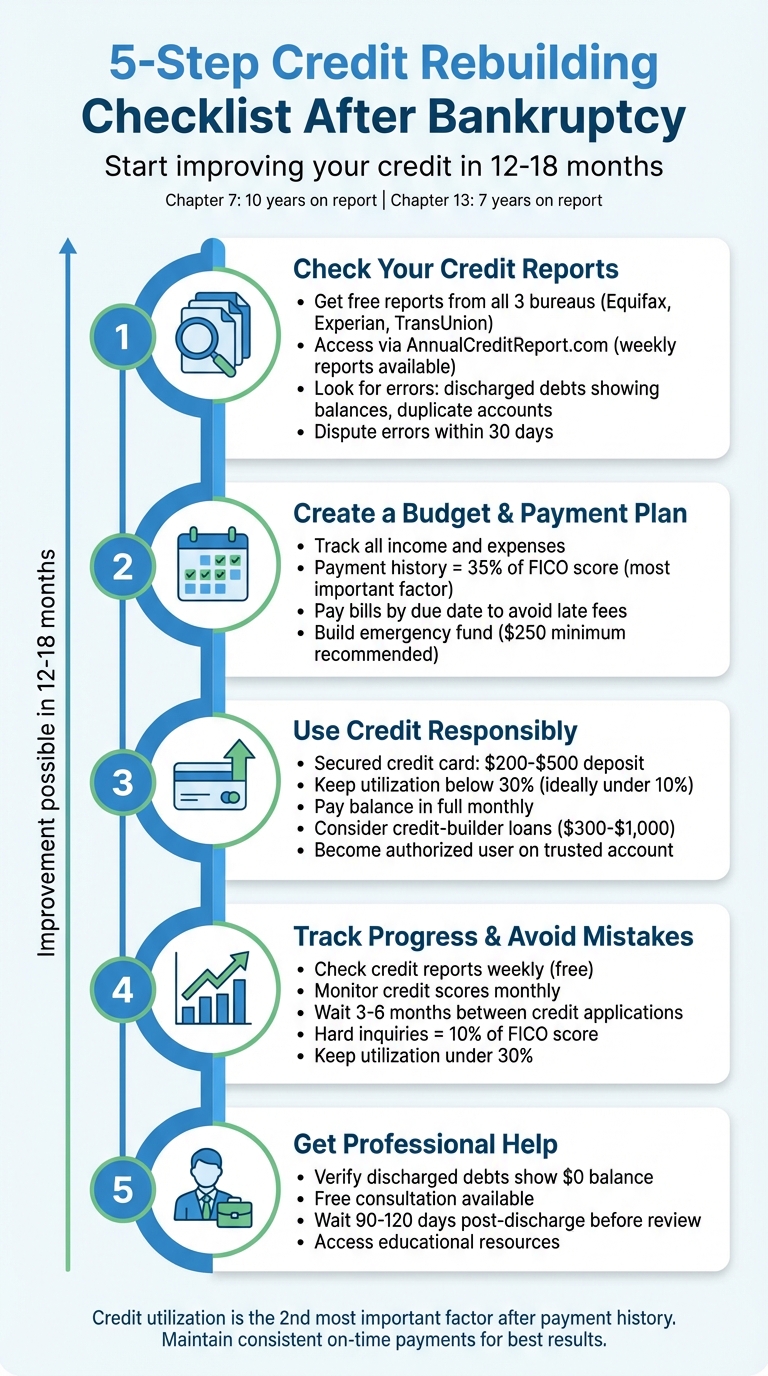

Filing for bankruptcy can significantly lower your credit score, but it doesn’t mean your financial future is ruined. With the right steps, you can start improving your credit within 12–18 months, even though bankruptcy remains on your report for 7–10 years. Here’s how:

- Check Your Credit Reports: Get free reports from Equifax, Experian, and TransUnion via AnnualCreditReport.com. Look for errors like discharged debts showing balances and dispute inaccuracies.

- Build a Budget: Track income and expenses, prioritize on-time payments, and start an emergency fund to avoid relying on credit for unexpected costs.

- Use Credit Wisely: Start with a secured credit card or credit-builder loan. Keep balances below 30% of your limit and pay in full monthly. Consider becoming an authorized user on a trusted account.

- Monitor Progress: Regularly review credit scores and reports, and avoid frequent credit applications to prevent hard inquiries.

- Seek Professional Help: Consult legal or financial experts to ensure discharged debts are accurately reflected and to navigate complex recovery steps.

5-Step Credit Rebuilding Checklist After Bankruptcy

Rebuilding Credit and Finances After Bankruptcy – With Melissa Ingersoll

Step 1: Get and Check Your Credit Reports

To start rebuilding your credit, the first step is to get your credit reports from the three major credit bureaus: Equifax, Experian, and TransUnion. Since lenders may report differently to each bureau, and errors can show up on one report but not the others, reviewing all three is essential. This process lays the groundwork for spotting mistakes, confirming details, and rebuilding your financial standing.

How to Get Free Credit Reports

You can access your credit reports for free through AnnualCreditReport.com, the only website authorized by federal law to provide them. You have three options for requesting your reports:

- Visit AnnualCreditReport.com online.

- Call 1-877-322-8228 (reports will arrive within 15 days).

- Mail a request to P.O. Box 105281, Atlanta, GA 30348-5281.

While federal law guarantees one free report from each bureau every 12 months, all three bureaus currently allow you to check your reports weekly at no cost . Be prepared to verify your identity by providing your Social Security number, date of birth, current address, and answers to security questions about your financial history.

"Only one website – AnnualCreditReport.com – is authorized to fill orders for the free annual credit reports you are entitled to by law." – Federal Trade Commission

Be cautious of websites claiming to offer "free" credit reports but requiring credit card details or subscriptions. AnnualCreditReport.com will never ask for payment information.

Finding Errors and Mistakes

Once you have your reports, carefully review them for errors. Common issues after bankruptcy include:

- Discharged debts showing balances instead of $0.

- Duplicate accounts.

- Incorrect personal information, such as unfamiliar addresses.

- Accounts listed as "active" or "past due" instead of "discharged" or "included in bankruptcy."

- Unfamiliar accounts or credit inquiries, which could point to identity theft.

Your bankruptcy should also be accurately listed: Chapter 7 remains on your report for 10 years, while Chapter 13 stays for 7 years .

"Incorrect information can appear on your report because the credit bureaus processed the information incorrectly or because lenders or debt collectors sent flawed information to the credit bureaus or did not update the information they previously reported." – Consumer Financial Protection Bureau

Disputing Errors with Credit Bureaus

If you find errors, take action by disputing them with each credit bureau. You can file disputes online, by phone, or through the mail. Be sure to include the following:

- Your name and address.

- Relevant account numbers.

- A brief explanation of the error.

- Copies of supporting documents, such as bankruptcy discharge papers .

If filing by mail, use certified mail with a return receipt to confirm delivery . Highlight the specific errors on your report to make your case clear. Credit bureaus are required to investigate disputes within 30 days and will provide the results in writing .

| Credit Bureau | Online Dispute Link | Mailing Address |

|---|---|---|

| Equifax | equifax.com/personal/credit-report-services/credit-dispute/ | P.O. Box 740256, Atlanta, GA 30348 |

| Experian | experian.com/disputes/main.html | P.O. Box 4500, Allen, TX 75013 |

| TransUnion | dispute.transunion.com | P.O. Box 2000, Chester, PA 19016 |

Additionally, reach out to the furnisher of the incorrect information to request updates to their records. If the dispute isn’t resolved to your satisfaction, you can ask the bureau to include a statement of your dispute in your file for future reports. Keep copies of all correspondence and track the dates of your communications. Once your disputes are resolved, you’ll be ready to move forward with rebuilding your credit.

Step 2: Create a Budget and Payment Plan

Building a disciplined budget is a crucial step toward improving your credit. A well-structured budget helps you track income and expenses, ensuring you avoid missed payments. Since payment history is the most important factor in determining credit scores, a solid budget becomes the cornerstone of rebuilding credit after bankruptcy.

Track Your Income and Expenses

Start by listing all sources of income, such as your salary, freelance work, or benefits. Next, detail recurring expenses like rent, utilities, groceries, and any other monthly obligations. This process not only highlights where your money goes but can also uncover areas where you can cut back. Redirecting these savings toward debt repayment or an emergency fund can make a big difference. Reflecting on what caused your bankruptcy – whether it stemmed from medical bills, job loss, or overspending – can help you recognize patterns and avoid similar challenges in the future.

Make Payments on Time

Timely payments are essential for maintaining and improving your credit. For a payment to count as "on time" in credit reporting, it must reach the creditor by its due date. Late payments can damage your credit score and result in extra fees, further straining your budget. To stay on track, consider setting up automatic alerts for bill due dates.

Use reminders a few days before your bills are due, and if mailing payments, send them early to ensure they’re processed on time. For debts that remain after bankruptcy, like recent tax bills or reaffirmed car loans, prioritize these payments to avoid further collection actions. Whenever possible, pay more than the minimum amount due – this helps reduce interest costs and clears debt faster. Staying consistent with payments is key to building a stronger financial future.

Start an Emergency Fund

An emergency fund can keep you from turning to credit cards when unexpected expenses pop up. Studies show that even $250 in savings can help families avoid high-interest loans or new credit card debt during emergencies. Without this safety net, an unexpected car repair or medical expense could undo months of progress in rebuilding your credit.

"Having a percentage of your paycheck automatically deposited into a high-yield savings account is a great place to start. This way, consumers will have a safety net if financial hardship strikes again."

- Leslie H. Tayne, Founder of Tayne Law Group

Treat your savings like any other fixed expense in your budget – just like rent or utilities. Deposit these funds into a high-yield savings account to let your money grow while remaining accessible for emergencies. This approach ensures you’re prepared for the unexpected without derailing your financial recovery.

Step 3: Use Credit Responsibly to Rebuild Your Score

Rebuilding your credit after bankruptcy requires demonstrating to lenders that you can manage credit responsibly. This involves using credit products wisely to establish a positive payment history, which is the most influential factor in your FICO score – accounting for about 35% of the total score. Below are some practical ways to rebuild your credit step by step.

Get a Secured Credit Card

A secured credit card can be a great starting point after bankruptcy. These cards require a refundable deposit, usually between $200 and $500, which sets your credit limit. Since the deposit reduces the lender’s risk, secured cards are easier to get compared to traditional unsecured cards.

Before applying, make sure the card issuer reports your activity to all three major credit bureaus – Equifax, Experian, and TransUnion. Without this reporting, your efforts won’t contribute to rebuilding your credit. Look for a card with low fees and consistent reporting.

Use your secured card for small, manageable purchases that you can pay off in full each month. Pay your balance in full by the due date to avoid high interest charges, which are often over 20%, and to show lenders you’re reliable. Keep your balance below 30% of your credit limit – for example, under $150 if your limit is $500. Setting up autopay can help ensure you never miss a payment.

After 6 to 12 months of responsible use, many issuers may review your account and "graduate" you to an unsecured card, refunding your deposit. This progression makes secured cards an excellent way to establish good credit habits and work toward qualifying for other credit products.

Consider Credit-Builder Loans

Once you’ve established a foundation with a secured card, adding a credit-builder loan can diversify your credit profile. These loans are unique because instead of receiving the loan amount upfront, the lender holds the funds – usually $300 to $1,000 – in a locked savings account or certificate of deposit. You make fixed monthly payments, and once the loan is fully paid, you gain access to the funds.

Credit-builder loans are low-risk for lenders since they can reclaim the funds if you default. More importantly, lenders report your payments to all three major credit bureaus, helping you build a history of on-time payments. These loans usually have repayment terms of 6 to 24 months and lower interest rates compared to unsecured personal loans.

Before applying, confirm that the lender reports to all three credit bureaus and check for any fees associated with the loan. Setting up automatic payments can help ensure you never miss an installment. Additionally, having an installment loan like this complements revolving credit (such as credit cards), which makes up 10% of your FICO score. Together, these steps strengthen your overall credit profile.

Become an Authorized User

If you have a trusted family member or friend with good credit, consider becoming an authorized user on their credit card. This allows you to benefit from their positive credit history, including on-time payments and low credit utilization, which will appear on your credit report.

As an authorized user, you’re not legally responsible for paying the bills – the primary account holder takes on that responsibility. It’s essential to ensure the account holder has a solid credit history, as their responsible behavior will reflect positively on your credit report.

"Piggybacking off someone else’s credit this way is a great idea for people who have just declared bankruptcy. If the card owner pays on time and keeps the debt low, your credit scores will rise."

- Adam Selita, CEO, The Debt Relief Company

Before being added, confirm that the credit card issuer reports authorized user activity to all three major credit bureaus, as not all issuers do. If the account holder’s financial habits change or become risky, you can usually request to be removed from the account, which will stop future activity from affecting your credit. While this is a helpful short-term strategy, use it alongside tools like secured cards and credit-builder loans to establish your own independent credit history. Together, these steps create a well-rounded approach to rebuilding your credit.

sbb-itb-d613a70

Step 4: Track Your Progress and Avoid Common Mistakes

Once you’ve started correcting errors and managing payments, the next step is to keep an eye on your progress and steer clear of common missteps. Rebuilding credit takes time and effort, but tracking your improvements and avoiding pitfalls can make the process smoother. Regular monitoring and responsible habits are your best tools for staying on track.

Check Your Credit Scores and Reports Regularly

Keeping tabs on your credit is crucial to ensure your bankruptcy discharge is accurately reflected and that your efforts to rebuild are effective. As mentioned in Step 1, you can access free weekly credit reports through AnnualCreditReport.com. Make it a habit to review your reports often. Look for accounts included in your bankruptcy and confirm they’re marked as "closed" with a $0 balance. If you spot any errors, dispute them right away.

"Debts should be marked as included in bankruptcy with zero balances."

- Ashley F. Morgan, Debt and Bankruptcy Lawyer

When it comes to credit scores, track them monthly using free tools provided by your bank or credit card issuer. Many banks offer access to FICO or VantageScore for free. Just make sure you stick to the same scoring model each time – comparing a FICO score one month to a VantageScore the next can give you a misleading picture of your progress.

"It’s smart to track your credit score month to month, and it’s crucial to look at the same score each time – otherwise, you’ll get a not-useful apples-to-oranges comparison."

If you manage your new accounts responsibly and pay all bills on time, you could see your credit scores start to improve within one to two years. Regular reviews not only help you measure your progress but also guide you in deciding when to apply for new credit.

Limit New Credit Applications

Once you have a clear understanding of your credit, be cautious about applying for new accounts. Submitting too many credit applications in a short time can harm your score. Each application results in a hard inquiry, which can temporarily lower your score and may signal to lenders that you’re facing financial trouble. Hard inquiries account for about 10% of your FICO score, so spacing out applications is important.

A good rule of thumb is to wait at least 3 to 6 months between credit applications. This allows each new account to establish a positive payment history before you add another. Focus on managing one or two accounts well rather than juggling multiple accounts. Setting up automatic payments can help ensure you never miss a due date, which is critical since payment history is the most important factor in your credit score. Even one late payment can set you back significantly, especially after bankruptcy.

Keep Credit Utilization Low

Credit utilization – the percentage of your available credit that you’re using – is the second most important factor in your FICO score after payment history. A high utilization rate can indicate to lenders that you’re overextended, which can hurt your score. After bankruptcy, proving that you can manage credit responsibly is essential.

Experts recommend keeping your utilization below 30%, though those with excellent credit often stay at 10% or less. For example, if you have a secured card with a $500 limit, aim to keep your balance under $150 – or better yet, under $50.

"Maintaining utilization rates under about 30% can prevent harm to your credit scores. People with excellent credit scores typically keep their utilization rates at or below 10%."

- Jim Akin, Freelance Writer, Experian

The best approach is to pay your balance in full every month. This not only keeps your utilization low but also helps you avoid interest charges. If you use your card frequently, consider making multiple small payments throughout the month instead of a single large payment at the end. This way, the balance reported to credit bureaus remains low. Also, avoid closing old credit card accounts, even if you rarely use them. Closing accounts reduces your total available credit, which can increase your utilization rate and hurt your score. Keeping your utilization low consistently demonstrates financial responsibility and strengthens your credit recovery journey.

Step 5: Get Professional Help for Post-Bankruptcy Recovery

Once you’ve laid the groundwork for rebuilding your credit, seeking professional help can make the process smoother and more effective. Recovering from bankruptcy can feel daunting, especially when juggling multiple accounts and correcting errors on your credit report. While you can handle many tasks independently, working with professionals can help you avoid mistakes and speed up your recovery. Their expertise in bankruptcy discharge and credit reporting ensures no critical details are missed.

Why Professional Legal Help Matters

Legal professionals play a key role in ensuring your debts are properly handled post-bankruptcy. They make sure discharged debts are accurately recorded, confirm creditors update your accounts correctly, and protect your credit score from unnecessary harm. As bankruptcy lawyer Ashley F. Morgan explains, “Debts should be marked as included in bankruptcy with zero balances”.

Professionals also guide you through complex recovery timelines. For instance, FHA guidelines may allow you to qualify for a mortgage just one year after bankruptcy or foreclosure, provided you meet specific conditions. Organizations like Foreclosure Defense Group specialize in helping individuals navigate these situations. Their services extend beyond ensuring accurate bankruptcy discharge; they also assist with foreclosure alternatives, such as loan modifications, Chapter 13 repayment plans, and deed-in-lieu agreements.

Schedule a Free Consultation

Foreclosure Defense Group offers a free consultation to help you create a personalized recovery plan. During this session, you can review your credit reports, confirm that discharged accounts are correctly updated, and receive tailored advice on managing debts not covered by your bankruptcy, such as student loans or mortgages.

To make the most of your consultation, come prepared with recent credit reports, your discharge papers, and a list of relevant accounts. It’s best to wait 90 to 120 days after your discharge to give creditors enough time to update their records. A professional can then help you identify lingering errors and outline a clear strategy for rebuilding your credit. This consultation not only addresses immediate concerns but also sets the stage for informed, long-term financial recovery.

Use Educational Resources

Professional guidance is invaluable, but staying informed is just as important. Foreclosure Defense Group provides a wealth of educational resources through its blog, offering practical advice on life after bankruptcy, foreclosure defense, and financial planning. These materials help you make informed decisions, understand your rights, and stay updated on lending rules. By combining expert advice with self-education, you’ll be better equipped to rebuild your financial future and achieve lasting stability.

Conclusion

Rebuilding credit after bankruptcy takes time, discipline, and consistent effort. While a Chapter 7 bankruptcy stays on your credit report for 10 years and Chapter 13 for 7 years, the negative impact lessens as you establish a positive payment history. Many people notice improvements in their credit within 12 to 18 months of filing. This timeline serves as a foundation for the steps discussed earlier.

Key actions include ensuring discharged debts are correctly marked as $0 on your credit reports, paying bills on time, keeping credit utilization low, and building an emergency fund. As Mae Koppes, Content Director at Upsolve, explains:

"While rebuilding credit after bankruptcy is a short- or medium-term project, maintaining good credit is a long-term commitment".

The financial decisions you make in the next two years will have the greatest impact on your credit score.

For those looking to speed up their recovery, seeking professional guidance can be a game-changer. Whether it’s confirming your discharge status, accessing legal help, or learning more about your rights, expert support can help you avoid costly mistakes and potential scams. For homeowners, Foreclosure Defense Group provides experienced legal representation and free consultations to help verify discharge statuses and safeguard your financial future.

FAQs

How long does it take to rebuild your credit after bankruptcy?

Rebuilding your credit after bankruptcy isn’t an overnight process – it requires patience and consistent effort. While you might see small positive changes within a few months, more noticeable progress often takes 6 to 12 months or longer. How quickly your credit improves largely depends on steps like addressing inaccuracies on your credit report and adopting responsible financial behaviors.

Key actions to focus on include disputing any errors on your credit report, ensuring bills are paid on time, and responsibly using tools like a secured credit card or a small loan to establish a positive credit history. With dedication and persistence, you can steadily improve your credit score and work toward financial stability.

How can I keep my credit utilization rate low to rebuild my credit after bankruptcy?

To keep your credit utilization rate in check, try to use less than 30% of your credit limit on each card – though aiming for 10% or less is even better. Paying off balances before your statement closing date can help lower the usage that gets reported. Another option? Request a higher credit limit or divide your spending across multiple cards to keep balances on each card manageable. Regularly reviewing your credit reports is also a smart move to stay aware of your utilization and catch any mistakes that might affect your credit score.

Why should I check and dispute errors on my credit report after bankruptcy?

Disputing errors on your credit report is an important step in protecting your financial health. Mistakes on your report can hurt your chances of rebuilding credit and may affect decisions made by lenders, employers, landlords, or insurers. These parties often rely on your credit report when determining loan approvals, job offers, rental agreements, or insurance rates. By ensuring your credit report is accurate, you can avoid unnecessary obstacles and set yourself up for a smoother financial recovery after bankruptcy.

Correcting errors also shows that you’re taking responsibility for your financial situation. This proactive approach can leave a positive impression on potential creditors, helping you regain financial stability faster.

Related Blog Posts

- Bankruptcy vs. Loan Modification: Which Option Is Right for You?

- How Chapter 13 Stops Foreclosure

- How Long Foreclosure Stays on Credit Reports

- Ultimate Guide to Post-Forbearance Repayment Options