Filing for bankruptcy can temporarily or permanently halt foreclosure proceedings in Florida, depending on the type of bankruptcy filed and your financial situation. Here’s what you need to know:

- Chapter 7 Bankruptcy: Offers temporary relief by pausing foreclosure for a few months. However, it doesn’t provide a way to catch up on missed mortgage payments. Once the case ends, foreclosure can resume unless the debt is resolved. It does, however, eliminate personal liability for the mortgage debt.

- Chapter 13 Bankruptcy: Allows homeowners to reorganize overdue payments into a 3-5 year repayment plan, letting them keep their home if payments are maintained. It also provides long-term foreclosure protection during the repayment period.

- Automatic Stay: Filing for bankruptcy triggers an automatic stay, which immediately halts foreclosure actions. However, this protection is time-sensitive and must occur before the foreclosure sale is finalized.

- Florida-Specific Factors: The state’s judicial foreclosure process and strong homestead exemptions can protect equity in your primary residence, but timing and strategy are key.

If foreclosure is imminent, acting quickly by filing bankruptcy before the sale is finalized can provide critical time to explore solutions. Each option has specific benefits and limitations, so consulting with a legal expert is essential to navigate this process effectively.

Florida Foreclosure and Bankruptcy Data

Foreclosure Rates in Florida

Florida currently holds the highest foreclosure rate in the country. As of October 2025, one in every 1,829 housing units in the state faced a foreclosure filing – more than twice the national average of one in 3,871. That month alone, Florida reported 5,512 foreclosure filings, with 4,136 properties entering the foreclosure process.

This isn’t a sudden development. Florida’s foreclosure struggles have been a persistent issue, with major metropolitan areas like Tampa, Jacksonville, and Orlando bearing the brunt. In October 2025, Tampa recorded a foreclosure rate of one in 1,373 units, Jacksonville one in 1,576, and Orlando one in 1,703. Tampa’s surge was partly due to Hillsborough County resuming data collection, which included previously backlogged records.

So, what’s behind these troubling numbers? The main factors include affordability challenges, rising borrowing costs, and financial pressures. Rob Barber, CEO of ATTOM, provides insight into the broader picture:

Foreclosure activity continued its steady upward trend in October, the eighth straight month of year-over-year increases… The current trend appears to reflect a gradual normalization in foreclosure volumes as market conditions adjust and some homeowners continue to navigate higher housing and borrowing costs.

While foreclosure figures are climbing, they’re still far below the peaks seen during past economic downturns. However, this steady increase is fueling a related rise in bankruptcy filings, as homeowners look for ways to manage their financial burdens.

Bankruptcy Filing Trends in Florida

Bankruptcy filings across the U.S. hit their highest levels since 2010 in 2025, driven by corporate challenges and mounting personal financial strain. Individual bankruptcy filings rose 8% year-over-year, reaching a total of 40,973 in November 2025. Among these, Chapter 7 filings – often referred to as a "clean slate" option – increased by 11%, while Chapter 13 filings, which are commonly used by Florida homeowners aiming to save their properties, grew by 5%.

These numbers highlight growing economic stress. Amy Quackenboss of the American Bankruptcy Institute points to rising costs, tighter credit access, and global uncertainties as key contributors to financial hardship.

The link between Florida’s foreclosure rate and bankruptcy trends is evident. When homeowners face foreclosure, many turn to bankruptcy – especially Chapter 13 – as a way to temporarily halt the process and restructure their debts. Florida’s judicial foreclosure process, which typically takes eight months to over a year, makes the automatic stay triggered by a bankruptcy filing an essential lifeline. This pause gives homeowners valuable time to create a plan for financial recovery, underscoring the critical role bankruptcy plays in navigating foreclosure challenges.

The Automatic Stay and Foreclosure Protection

What the Automatic Stay Does

When you file for bankruptcy, an automatic stay kicks in under Section 362 of the Bankruptcy Code. Think of it as a legal "pause button" that stops creditors from taking collection actions against you. Attorney Orfelia Mayor sums it up well:

"The automatic stay is one of the most powerful credit relief actions there is. It serves as a ‘STOP SIGN’ that prevents creditors from proceeding without facing legal repercussions."

This protection is far-reaching. It halts mortgage foreclosures, cancels scheduled foreclosure sales, stops wage garnishments, and blocks car repossessions. In Florida, where foreclosures follow a judicial process, the automatic stay can interrupt the often lengthy proceedings. For homeowners facing an imminent foreclosure sale, filing an emergency bankruptcy petition can immediately activate this safeguard.

The duration of the stay depends on the type of bankruptcy filed. In Chapter 7 cases, it usually lasts four to six months, ending when the case is closed. On the other hand, Chapter 13 provides longer-term protection, potentially lasting three to five years as you work through a repayment plan. However, the stay isn’t all-encompassing – it doesn’t stop criminal cases, child support collections, or IRS audits.

While the automatic stay offers powerful protections, it does have its limits, as outlined below.

When the Automatic Stay Fails

The automatic stay isn’t a guarantee to save your home in every situation. If a foreclosure sale has already been finalized and your property rights have been terminated under Florida law, bankruptcy cannot reverse the outcome. Timing is everything – you must file before the foreclosure sale is completed.

Lenders can also work around the stay by filing a Motion for Relief from the Automatic Stay. In the Southern District of Florida, this process often operates on "negative notice." This means that if you don’t respond within 14 days, the court can grant the lender permission to proceed without holding a hearing. This is particularly common in Chapter 7 cases, where there’s no mechanism to catch up on missed mortgage payments, allowing lenders to move forward with foreclosure.

For those who have filed bankruptcy more than once, the protections of the automatic stay are limited. If a prior case was dismissed within the past 12 months, the stay lasts only 30 days. If two or more cases were dismissed, the stay doesn’t take effect at all. Additionally, if you designate your property as "surrendered" in a Chapter 7 filing, Florida Statute §702.12 creates a rebuttable presumption that you’ve waived any defense to foreclosure in state court.

In Chapter 13 cases, the stay can also be lifted if you fall behind on post-petition mortgage payments or fail to meet procedural requirements, such as attending the creditors’ meeting. In such cases, lenders can petition to resume foreclosure proceedings.

Bankruptcy & Foreclosure: Will Filing Stop It?

sbb-itb-d613a70

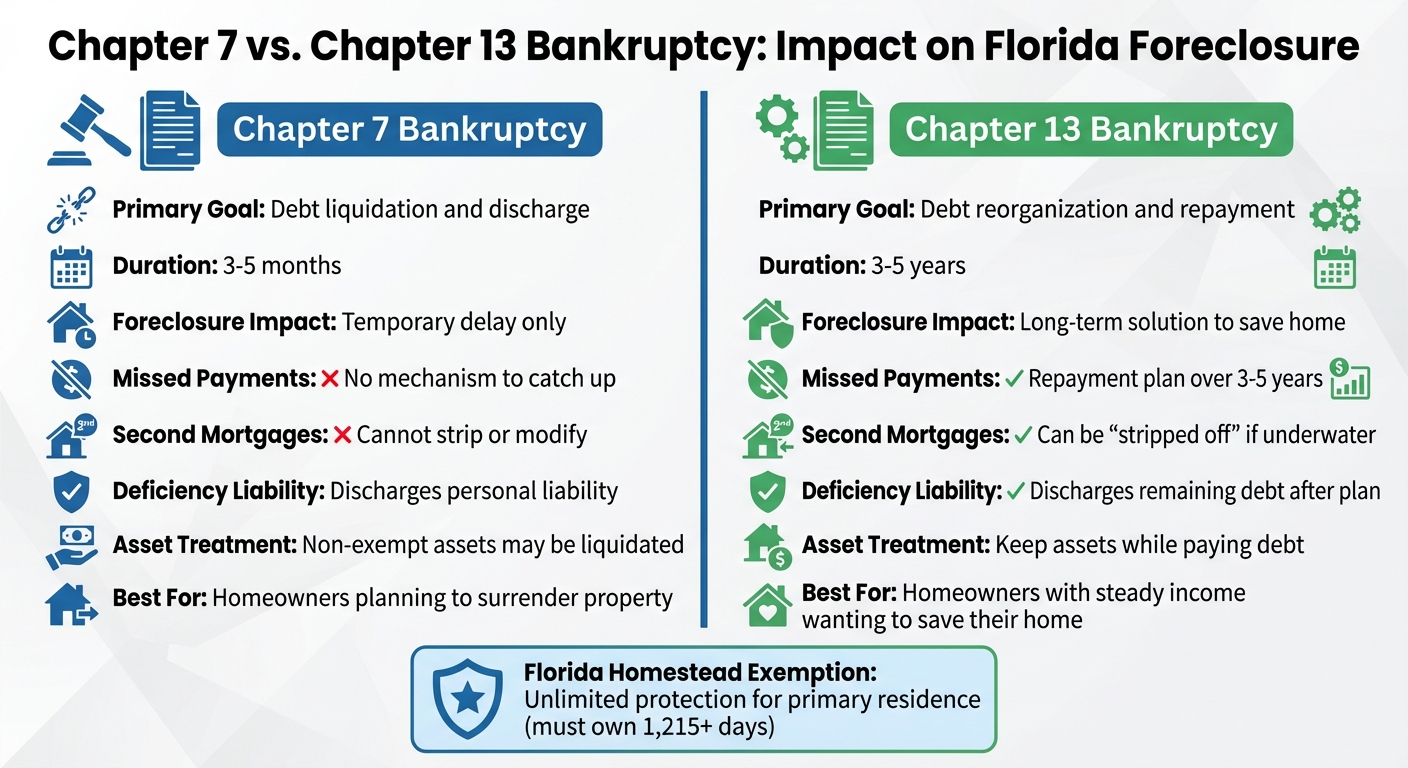

Chapter 7 vs. Chapter 13 Bankruptcy for Foreclosure

Chapter 7 vs Chapter 13 Bankruptcy: Impact on Florida Foreclosure

Chapter 7 Bankruptcy Effects on Foreclosure

When it comes to foreclosure, Chapter 7 and Chapter 13 bankruptcy filings offer very different outcomes. Let’s start with Chapter 7.

Chapter 7 bankruptcy is all about debt liquidation. The process typically lasts about 3 to 5 months, during which the automatic stay temporarily halts foreclosure proceedings. However, as bankruptcy attorney Orfelia Mayor explains:

"A chapter 7 bankruptcy does not do anything to help you keep your home because a Davie chapter 7 bankruptcy is the liquidation chapter in bankruptcy. Filing a chapter 7 bankruptcy will therefore only delay the inevitable foreclosure sale."

In short, Chapter 7 doesn’t provide a way to catch up on missed mortgage payments. Lenders can even request the court to lift the automatic stay, allowing foreclosure to move forward. That said, Chapter 7 does serve a critical purpose: it wipes out your personal liability for the mortgage debt. This means if your home sells for less than what you owe, the lender can’t come after you for the remaining balance.

Florida homeowners benefit from the state’s unlimited homestead exemption, which offers strong protection if you’re current on payments and have significant equity. To qualify, you must have owned your home and lived in Florida for at least 1,215 days (around 40 months). If you don’t meet this requirement, the exemption is capped at about $160,000 per person. This protection applies to up to half an acre in a municipality or 160 acres in rural areas.

Chapter 13 Bankruptcy Effects on Foreclosure

For homeowners looking to save their home, Chapter 13 bankruptcy is often the better choice. Attorney Howard Iken describes it this way:

"Chapter 13 bankruptcy is the most common way for people to improve their financial condition and keep their home especially if the home has substantial equity."

Chapter 13 allows you to catch up on missed payments while continuing to make your regular monthly mortgage payments. Unlike Chapter 7, this is a reorganization plan, not liquidation, meaning you get to keep your assets while working to pay off your debts. The automatic stay remains in effect throughout the repayment plan, which can last up to five years, offering long-term foreclosure protection.

One unique feature of Chapter 13 is lien stripping. If your home’s value is less than the amount owed on your first mortgage, you can strip off a second mortgage and treat it as unsecured debt. This option isn’t available in Chapter 7, thanks to the Supreme Court’s Caulkett decision. Miami bankruptcy lawyer Julia Kefalinos highlights this key difference:

"Unlike Chapter 7, in a Chapter 13 case the debtor has the right to make up past-due mortgage payments during the term of the court-approved repayment plan, which can last up to five years."

These features make Chapter 13 a powerful tool for homeowners aiming to avoid foreclosure.

Chapter 7 vs. Chapter 13 Comparison

Choosing between Chapter 7 and Chapter 13 depends on your financial situation and whether you’re trying to keep your home.

| Feature | Chapter 7 Bankruptcy | Chapter 13 Bankruptcy |

|---|---|---|

| Primary Goal | Debt liquidation and discharge | Debt reorganization and repayment |

| Foreclosure Impact | Temporary delay (3–5 months) | Long-term solution to save home |

| Missed Payments | No mechanism to catch up | Repayment plan over 3–5 years |

| Second Mortgages | Cannot strip or modify second mortgages | Can be "stripped off" if underwater |

| Deficiency Liability | Discharges personal liability | Discharges remaining debt after plan |

| Asset Treatment | Non-exempt assets may be liquidated | Debtor keeps assets while paying debt |

If you’re behind on payments but have a steady income, Chapter 13 is your best bet for saving your home. On the other hand, if you’re planning to give up the property, Chapter 7 can help you eliminate deficiency liability and protect you from future collection efforts.

For tailored legal advice on navigating bankruptcy and foreclosure, Florida homeowners can turn to the experienced team at Foreclosure Defense Group (https://foreclosuredefensegroup.com).

Long-Term Effects of Bankruptcy on Foreclosure

Housing Outcomes After Bankruptcy

If you’re looking for a way to prevent foreclosure in the long run, Chapter 13 bankruptcy can be a powerful tool. It allows you to address defaults through a structured repayment plan lasting three to five years, helping you retain control of your home during that time.

On the other hand, Chapter 7 bankruptcy provides only temporary relief. Once the automatic stay expires, lenders can resume foreclosure proceedings. Under Florida Statute 702.12, declaring your intent to surrender the property in a Chapter 7 filing could mean permanently giving up any foreclosure defenses. Miami bankruptcy attorney Julia Kefalinos underscores the gravity of this decision:

By filing for bankruptcy, they surrendered any right to keep the house. So even if the bankruptcy trustee abandoned his claim, the creditor’s secured claim remains intact.

These immediate outcomes regarding your home lay the foundation for the broader financial challenges you’ll face after bankruptcy.

Financial Recovery After Bankruptcy

While bankruptcy can alter the timeline for foreclosure, its effects on your overall financial health are equally important to consider.

Bankruptcy leaves a lasting mark on your credit report: Chapter 7 filings remain for 10 years, while Chapter 13 filings stay for seven. Similarly, a foreclosure will appear on your credit report for seven years, potentially affecting your ability to qualify for a mortgage for five to seven years.

Rebuilding your financial standing after bankruptcy requires a focused approach. Staying current on mortgage payments is crucial, especially if you’re using Chapter 7 to eliminate unsecured debts like medical bills or credit card balances. Keeping up with your mortgage can safeguard your home under Florida’s homestead exemption. For those in a Chapter 13 plan, it’s essential to stick to a strict budget and consult with your bankruptcy trustee before taking on any new financial obligations.

Florida law also offers some protection: employers cannot penalize you solely for filing bankruptcy. This safeguard can help you maintain steady income as you work toward financial recovery. If you’re feeling overwhelmed by the complexities of these decisions, reaching out to experienced attorneys, such as those at Foreclosure Defense Group (https://foreclosuredefensegroup.com), can provide valuable guidance. They can help you build a strategy that addresses both immediate foreclosure concerns and long-term financial stability.

Conclusion

Dealing with foreclosure while considering bankruptcy in Florida requires a clear understanding of how these legal processes interact. The automatic stay – triggered as soon as you file a bankruptcy petition – offers immediate relief by stopping all collection efforts, including foreclosure auctions. However, the type of bankruptcy you choose plays a critical role in determining your next steps. Chapter 13 provides a structured three- to five-year repayment plan to help you catch up on missed payments and retain your home. On the other hand, Chapter 7 only offers a temporary pause, after which lenders can proceed with foreclosure. Acting quickly and choosing the right bankruptcy option is essential to effectively defend against foreclosure.

Timing is everything. To protect your home, you must file for bankruptcy before the foreclosure sale is finalized and the certificate of sale is filed. Missing this window could mean permanently losing your property rights.

Navigating the complexities of bankruptcy and foreclosure laws can be overwhelming without professional guidance. Attorney Lewis Roberts emphasizes:

Bankruptcy is a maze of procedures and regulations that must be followed to the letter.

Even a single error could result in case dismissal, wasted resources, and long-term financial harm. Without legal representation, you may also unknowingly forfeit important foreclosure defenses.

This is why working with an experienced attorney is so important. If you’re facing foreclosure and considering bankruptcy, seeking legal advice early can make all the difference. The attorneys at Foreclosure Defense Group are equipped to guide you through these challenging processes. They offer free consultations to assess your situation and create a strategy that aligns with your financial needs, whether that means keeping your home through Chapter 13, exploring loan modifications, or pursuing other alternatives like short sales.

Take action now. The earlier you seek help, the more options you’ll have to protect your home and secure your future.

FAQs

What happens to foreclosure proceedings in Florida when you file for bankruptcy?

Filing for bankruptcy in Florida activates an automatic stay, which temporarily halts foreclosure actions. During this period, lenders are prohibited from filing a notice of sale, scheduling a foreclosure auction, or pursuing other collection efforts. This pause offers homeowners a critical window to consider solutions such as loan modifications, Chapter 13 repayment plans, or other alternatives to foreclosure.

If a lender wishes to move forward with foreclosure despite the automatic stay, they must request approval from the bankruptcy court by filing a motion to lift the stay. Typically, the stay remains in effect until the bankruptcy case concludes or the court decides otherwise. This legal safeguard provides homeowners with much-needed time to protect their property and explore viable options.

For Florida homeowners facing foreclosure, working with experienced legal professionals, like the Foreclosure Defense Group, can be instrumental in leveraging the protection of the automatic stay and crafting a plan tailored to their financial needs.

What’s the difference between Chapter 7 and Chapter 13 bankruptcy when it comes to stopping foreclosure in Florida?

Both Chapter 7 and Chapter 13 bankruptcy offer an automatic stay that temporarily pauses foreclosure proceedings in Florida. However, they serve different purposes and have distinct long-term outcomes.

Chapter 7 bankruptcy provides temporary relief by halting foreclosure while your assets are assessed and unsecured debts are discharged. That said, it doesn’t erase mortgage debt. If you’re behind on payments, the lender can resume foreclosure once the stay is lifted. Florida’s homestead exemption may protect the equity in your primary home, but it won’t prevent foreclosure if mortgage payments remain unpaid.

Chapter 13 bankruptcy takes a different approach, giving you the chance to develop a court-approved repayment plan that spans three to five years. This plan allows you to catch up on missed mortgage payments, potentially saving your home from foreclosure. It’s often a more practical choice for homeowners who are committed to keeping their property and can handle structured repayments.

If foreclosure is a concern in Florida, the Foreclosure Defense Group can help you evaluate your options and guide you through the bankruptcy process to safeguard your home.

Can filing for bankruptcy help me avoid foreclosure on my home in Florida?

Filing for bankruptcy in Florida can offer temporary relief and might help you hold onto your home. When you file, an automatic stay is triggered, which temporarily halts foreclosure proceedings.

If you opt for Chapter 13 bankruptcy, it allows you to reorganize your debts and set up a repayment plan. This plan could help you catch up on overdue mortgage payments while keeping your home. Alternatively, Chapter 7 bankruptcy may protect the equity in your home through Florida’s homestead exemption, as long as you continue making your mortgage payments on time.

While bankruptcy can be a useful tool, its effectiveness in addressing foreclosure depends on your unique financial circumstances. Speaking with an experienced attorney can help you understand your options and safeguard your rights as a homeowner.

Related Blog Posts

- 7 Legal Rights Every Florida Homeowner Should Know

- 3 Ways to Stop Foreclosure in Florida

- How Chapter 13 Stops Foreclosure

- Deficiency Judgments in Florida: Key Facts