The automatic stay is a legal protection that begins the moment you file for bankruptcy. It immediately halts foreclosure proceedings, creditor calls, wage garnishments, and repossessions. This gives homeowners a temporary pause to organize their finances and explore options to keep their property.

Key points:

- Filing for bankruptcy (Chapter 7, 11, 12, or 13) activates the stay.

- Stops foreclosure sales, creditor lawsuits, and utility disconnections for at least 20 days.

- Violations by creditors can result in penalties, including damages and legal fees.

- Duration depends on the type of bankruptcy and prior filings:

- Chapter 7: Lasts 3–5 months, offering a short delay.

- Chapter 13: Extends through a 3–5 year repayment plan, allowing homeowners to catch up on missed payments.

Exceptions:

- Does not stop criminal cases, child support collection, or certain tax actions.

- Creditors can request the court to lift the stay under specific conditions.

For personalized advice, consult legal professionals to understand how these protections apply to your situation.

How the Automatic Stay Stops Your Creditors | Learn About Law

sbb-itb-d613a70

How the Automatic Stay Works

The automatic stay kicks in the moment your bankruptcy petition is filed with the court clerk. This is outlined in 11 U.S.C. § 362(a), which ensures the stay becomes effective automatically – no judge’s signature, hearing, or additional court order is required.

Once active, the stay legally binds all creditors immediately, even before they’re officially notified of your bankruptcy filing. If creditors violate the stay after being notified, they can face court-imposed penalties under 11 U.S.C. § 362(k). To help prevent violations, it’s a good idea to notify creditors promptly and provide them with your case number.

What Activates the Automatic Stay?

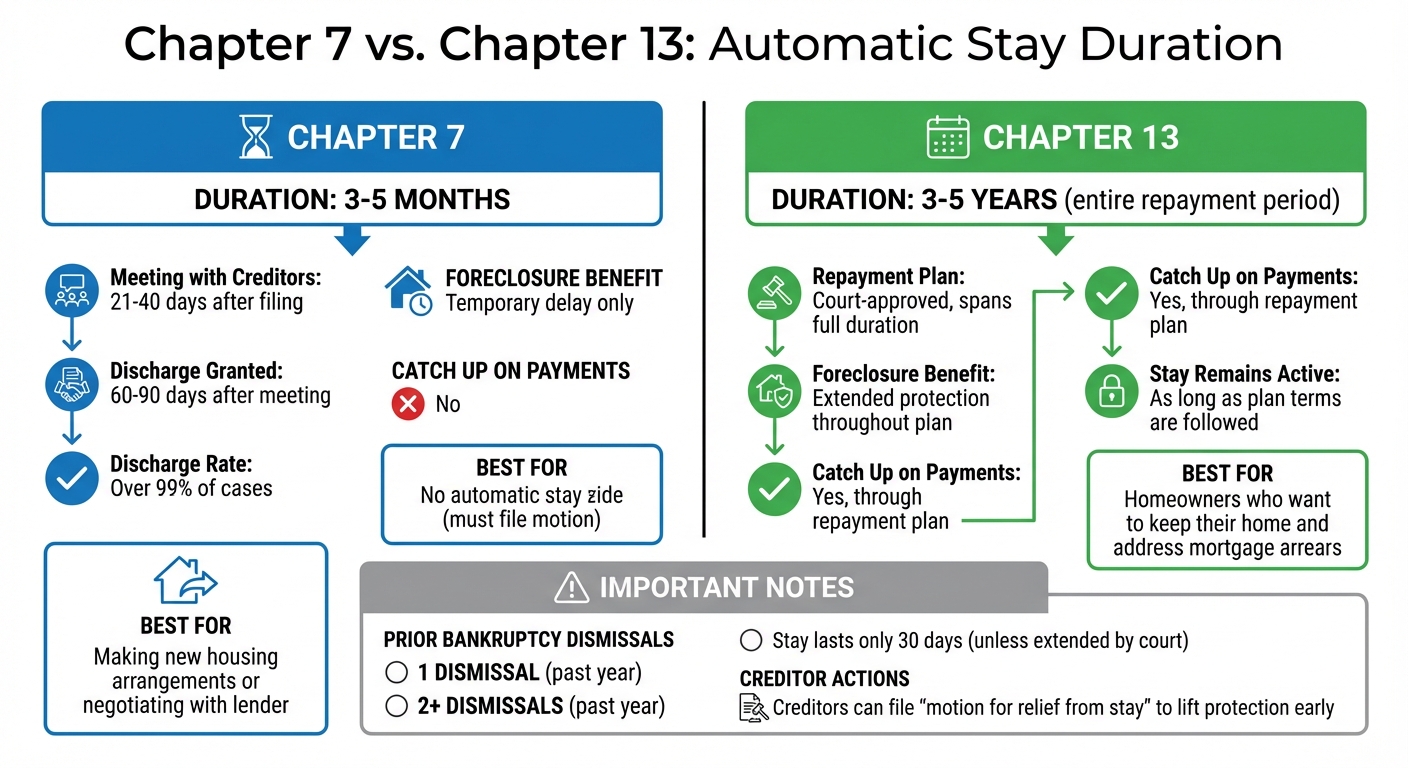

Knowing what triggers the automatic stay helps clarify when its protections begin. Filing for bankruptcy under Chapter 7, 11, 12, or 13 activates the automatic stay. However, this applies only to first-time filers who haven’t had a bankruptcy case dismissed in the last 12 months.

The rules are stricter for those who’ve filed before. If you’ve had one bankruptcy case dismissed in the past year, the automatic stay lasts for just 30 days, unless you file a motion and the court agrees to extend it. For those with two or more dismissals within a year, no automatic stay takes effect. In such cases, you’ll need to file a motion requesting the court to impose a stay.

Now that you know how it activates, let’s explore the types of creditor actions the stay puts on hold.

What Actions Does the Automatic Stay Stop?

Once in place, the automatic stay halts a wide range of creditor actions, especially those that could lead to foreclosure. In judicial foreclosure states, the stay stops courts from issuing orders to sell your home. In nonjudicial foreclosure states, it blocks lenders from completing necessary steps, such as publishing sale notices in newspapers.

The stay also puts an immediate stop to wage garnishments for debts incurred before filing, vehicle repossessions, debt collection lawsuits, and all forms of creditor communication, including phone calls and letters. Utility companies are prohibited from disconnecting essential services like water, electricity, gas, or phone service for at least 20 days after you file, even if you’re behind on payments. To keep these services beyond 20 days, you’ll need to provide a deposit or some form of assurance.

However, there are exceptions. The automatic stay does not apply to criminal cases, actions to establish or collect child support or alimony, IRS audits, tax deficiency notices, or requests for tax returns. Additionally, mortgage lenders can file a “motion for relief from stay” to move forward with foreclosure if you lack equity in your home or fail to protect their financial interest.

How the Automatic Stay Stops Foreclosure

The automatic stay puts an immediate halt to foreclosure proceedings as soon as you file a bankruptcy petition. This protection, outlined in 11 U.S.C. § 362, prevents lenders from taking any action to seize or control property included in the bankruptcy estate. Here’s how it disrupts foreclosure processes.

Immediate Halt to Foreclosure Sales

The moment the stay takes effect, any scheduled foreclosure sales are canceled – whether the foreclosure process is judicial or nonjudicial. In states with nonjudicial foreclosures, the stay blocks lenders from completing the required steps before an auction. Lenders cannot set a new auction date or move forward unless they obtain permission from the bankruptcy court to lift the stay.

Even if the court grants temporary relief by lifting the stay, homeowners still benefit from an additional 14-day protection under Federal Rule of Bankruptcy Procedure 4001. This extra time allows homeowners to respond or file an appeal.

Temporary Relief for Homeowners

The automatic stay doesn’t just stop foreclosure – it also gives homeowners valuable time. The length and type of relief depend on the bankruptcy chapter you file under.

- Chapter 7: This delays foreclosure for about 3 to 4 months, giving you time to make new housing arrangements or negotiate with your lender. However, it doesn’t provide a way to catch up on missed payments.

- Chapter 13: With Chapter 13, you can create a repayment plan that spans three to five years. This plan allows you to address overdue payments while staying current on your mortgage. During this period, the automatic stay remains in effect, giving you a chance to keep your home.

How Long Does the Automatic Stay Last?

Chapter 7 vs Chapter 13 Bankruptcy: Automatic Stay Duration and Foreclosure Protection

The length of the automatic stay depends on the type of bankruptcy you file and your previous bankruptcy history. Understanding these timelines can help you plan your next steps.

Duration by Bankruptcy Chapter

In a Chapter 7 bankruptcy, the automatic stay typically lasts for the entire duration of the case, which is about 3 to 5 months. After filing, a meeting with creditors usually takes place within 21–40 days, and the discharge is granted 60–90 days later. For most Chapter 7 cases – over 99% – a discharge is issued, and at that point, the stay ends.

For Chapter 13 bankruptcy, the stay lasts much longer. It remains in effect for the entire repayment period, which usually spans 3 to 5 years. This extended stay allows debtors to address issues like mortgage arrears over the course of the repayment plan.

While these are the standard durations, certain circumstances can either shorten or extend the automatic stay.

Limits and Exceptions to the Stay

There are scenarios where the automatic stay may not offer full protection or may end sooner than expected. For instance, if you’ve had prior bankruptcy cases dismissed, the stay might be reduced or even eliminated.

Creditors can also ask the court to lift the stay early. This often happens if they argue that there’s not enough equity in your property or that their financial interests aren’t adequately safeguarded. If the court agrees, creditors can resume actions like foreclosures.

It’s also important to note that the automatic stay doesn’t apply to every situation. For example, it won’t stop:

- Criminal proceedings

- Collection of child support or alimony

- Certain tax audits

Additionally, in a Chapter 7 case, if you fail to file a Statement of Intent for your property within 30 days of filing, the stay might end early for that specific asset.

What to Do if Creditors Violate the Automatic Stay

The automatic stay is a powerful tool that stops creditors from pursuing collection actions once you file for bankruptcy. But what happens if a creditor ignores this protection? Whether the violation is accidental or intentional, it’s essential to act quickly to safeguard your rights and financial stability.

How to Recognize Stay Violations

To prove a violation of the automatic stay, three things must be established: the stay is in effect (which begins the moment you file for bankruptcy), the creditor knows about your bankruptcy, and they continue with actions prohibited by the stay. Examples of violations include:

- Proceeding with a foreclosure sale

- Sending collection notices or letters

- Making harassing phone calls

- Garnishing wages

- Repossessing property without court approval

"A willful violation of the stay occurs when a creditor knows of the bankruptcy filing and continues to contact a debtor."

- Aiden Murphy, Esq., Attorney, Scura Law

Keep detailed records of any creditor interactions after filing. Note dates, times, names of representatives, and save copies of letters, emails, or other communications. If a creditor garnishes your wages or takes money from your bank account after your filing, those funds must be returned immediately. Regularly reviewing your financial accounts can help you spot violations early.

Once you’ve gathered evidence, you can take steps to enforce your rights.

Legal Options for Violations

If a creditor contacts you after your bankruptcy filing, provide your case number, filing date, and court location. Follow up with a written notice to create a clear paper trail.

If the violations continue, your attorney can file a motion for an "order to show cause" or initiate an adversary proceeding to hold the creditor accountable. Courts take these violations seriously and may impose penalties, including:

- Reimbursement for actual damages

- Compensation for emotional distress

- Attorney’s fees

- Punitive damages

In some cases, courts have awarded up to $10,000 in total damages, including approximately $5,500 for legal fees and $3,500 for emotional distress, with punitive damages reaching as high as $25,000.

Additionally, if the creditor’s actions also breach the Fair Debt Collection Practices Act (FDCPA) or state consumer protection laws, you may be able to pursue further legal action for additional penalties.

For personalized legal advice – especially if you’re dealing with foreclosure – consult experienced professionals like the Foreclosure Defense Group (https://foreclosuredefensegroup.com). Their expertise can help ensure your rights are fully protected.

Conclusion: Using the Automatic Stay to Protect Your Home

The automatic stay is one of the strongest legal tools available to homeowners facing foreclosure. Once you file for bankruptcy, it immediately halts foreclosure sales and other creditor actions. This pause provides much-needed breathing room to sort out your finances without the constant stress of collection efforts.

If your goal is to keep your home, Chapter 13 bankruptcy is often the better option. Unlike Chapter 7, which only provides a temporary delay, Chapter 13 establishes a three- to five-year court-approved repayment plan. During this time, the automatic stay remains active, shielding you from foreclosure as long as you follow the plan’s terms. This makes choosing the right bankruptcy chapter critical for long-term protection.

"The automatic stay doesn’t just stop the legal process of collection. It stops the psychological assault. The phone goes quiet. The mailbox is just a mailbox again."

- Steve Rhode, Consumer Debt Expert

However, it’s important to remember that prior bankruptcy dismissals can impact these protections. In some cases, lenders may request the court to lift the stay early.

Given these challenges, working with a legal professional is key to making the most of the automatic stay. Foreclosure Defense Group (https://foreclosuredefensegroup.com) provides expert guidance to help homeowners choose the right bankruptcy chapter and respond to attempts to lift the stay. With the right plan and support, the automatic stay can be the first step toward regaining financial stability and saving your home.

FAQs

Can I file bankruptcy the day before a foreclosure sale?

Yes, it’s possible to file for bankruptcy the day before a foreclosure sale. When you do, it activates the automatic stay, which temporarily halts the foreclosure process. This can give homeowners some breathing room, but it’s important to note that this pause isn’t indefinite. To fully understand your rights and the best course of action, it’s essential to consult with a legal professional.

Will the automatic stay stop foreclosure if I’ve filed before?

Yes, filing for bankruptcy typically triggers an automatic stay, which pauses foreclosure proceedings temporarily – even if you’ve filed in the past. However, how long the stay lasts and how effective it is can vary based on your individual situation and any prior bankruptcy filings. It’s important to consult with a legal expert to fully understand your rights and the protections available to you.

How do I keep my home after the stay ends?

When the automatic stay ends, taking swift action is crucial to keeping your home. Start by addressing any missed mortgage payments or financial difficulties head-on. You might consider options like negotiating a loan modification, requesting a forbearance, or even filing for Chapter 13 bankruptcy to manage overdue payments.

It’s essential to work directly with your lender to discuss repayment plans or explore foreclosure prevention programs they may offer. Additionally, reaching out to a foreclosure defense attorney can provide valuable guidance, helping you navigate potential legal solutions to safeguard your home.

Related Blog Posts

- 7 Legal Rights Every Florida Homeowner Should Know

- How Chapter 13 Stops Foreclosure

- How Bankruptcy Impacts Foreclosure in Florida

- 5 Reasons Automatic Stay May Be Lifted