Deed-in-lieu of foreclosure can help you avoid a full foreclosure, but the process is rarely straightforward. Here are five common hurdles you might face:

- Lender Delays: Banks often take weeks or months to review requests, especially if documents are incomplete or the property title has issues.

- Junior Liens: Second mortgages, HOA dues, or other liens can derail approval since lenders need a clear title.

- Deficiency Judgments: Without a clear waiver, you could still owe the difference between your loan balance and your home’s value.

- Credit & Tax Impact: A deed-in-lieu affects your credit score and may lead to taxable income on forgiven debt.

- Appraisal Disputes: Disagreements over property value can lead to rejection or unexpected costs.

Each step requires careful preparation and negotiation to avoid surprises. Consulting a professional can help you navigate these challenges.

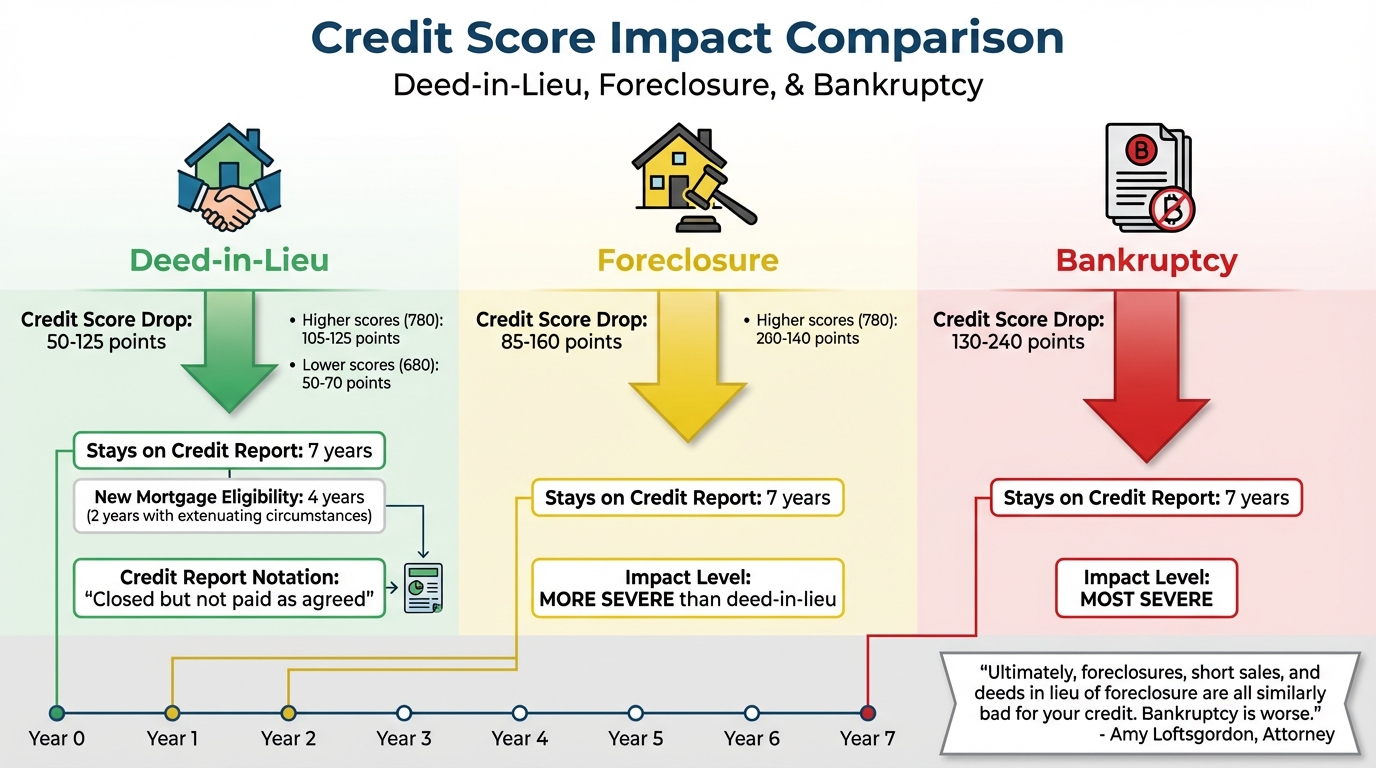

Credit Score Impact: Deed-in-Lieu vs Foreclosure vs Bankruptcy Comparison

How to Stop Foreclosure: Negotiating Deed in Lieu with Mortgage Holders

sbb-itb-d613a70

1. Lender Delays in Decision-Making and Approval

Lenders operate on their own schedule, not yours. When negotiating a deed in lieu of foreclosure, servicers often take weeks – or even months – to review a request. Unfortunately, this timeline rarely aligns with the urgency of homeowners already facing foreclosure. These delays are often worsened by missing paperwork or issues with the property title.

"The paperwork moves at the servicer pace, not your pace." – Damon Rittenhouse, EV Häs LLC

One major cause of delays is incomplete documentation. If even a single document – like a pay stub, bank statement, or tax return – is missing, the review process can be reset entirely. Additionally, lenders typically require proof that you’ve attempted to sell the property for at least 90 days before they even consider your application. This mandatory marketing period can eat up three months before negotiations even begin.

Title complications can drag things out even further. Lenders need to conduct a detailed title search to identify potential issues like second mortgages, judgment liens, or unpaid HOA fees. If the title isn’t clear, the process can stall indefinitely or even result in outright denial. On top of that, reviewing a Broker Price Opinion (BPO) or property appraisal adds more time to the process. All of this happens while foreclosure proceedings march forward, creating a race against time.

"Deed in lieu backfires when it becomes a delay tactic that does not actually stop the foreclosure timeline." – Mahmoud Faisal Elkhatib, Chicago Real Estate Lawyer

To avoid unnecessary delays, make sure your documentation is complete. This includes two recent pay stubs (or a profit and loss statement if you’re self-employed), two years of tax returns, two months of bank statements for all accounts, and a hardship letter. It’s also smart to do a preliminary title search to catch any junior liens that could cause problems. Think of the deed-in-lieu process as a carefully managed timeline project, not a last-minute solution. Having a backup plan in place is equally important.

2. Junior Liens or Encumbrances on the Property

Junior liens are a major roadblock for deed-in-lieu requests. These include second mortgages, home equity lines of credit (HELOCs), unpaid HOA dues, mechanic’s liens, and judgment liens. Unlike foreclosure, which legally wipes out these claims, a deed in lieu is a voluntary transfer. This means the lender takes on responsibility for any unresolved liens still tied to the property.

Lenders require a clear title. If they acquire a property with outstanding junior liens, they’ll need to settle those debts before selling the home. This is why lenders often prefer judicial foreclosure – it clears subordinate liens, ensuring the property has a clean, marketable title.

Start with a detailed title search to avoid surprises. Unresolved issues like old judgments, unpaid HOA fees, or contractor bills can surface and derail your application. Identifying these liens early gives you the chance to negotiate settlements and secure lien releases. Even small debts, like unpaid association dues, can block approval, so addressing these upfront is crucial to moving forward.

A notable example is the 2015 case of Decon Group, Inc. v. Prudential Mortgage Capital Co., LLC. Prudential accepted a deed in lieu but included an "anti-merger clause" to keep their mortgage lien intact. This allowed them to foreclose later and eliminate a junior lien held by Decon Group. Most homeowners won’t have access to such legal tools, so resolving liens yourself is essential to avoid denial.

3. Deficiency Judgments and Liability Release

Deficiency judgments can be a major hurdle when negotiating a deed in lieu of foreclosure.

In simple terms, a deficiency judgment is the gap between what you owe on your mortgage and the fair market value of your home. For instance, if your mortgage balance is $300,000 but your home is only worth $225,000, that $75,000 difference is considered the deficiency. If your agreement doesn’t explicitly waive this debt, your lender could come after you to recover it.

Here’s the catch: signing a deed in lieu doesn’t automatically erase your debt. While transferring the property gets rid of the mortgage lien, it doesn’t cancel the promissory note tied to your loan. To fully protect yourself, your agreement must clearly state that the promissory note is "satisfied in full" as part of the deal.

"Acceptance of a lieu deed terminates the liability of the borrower and all other persons liable for the mortgage debt unless there is an agreement to the contrary made contemporaneously with the lieu deed transaction."

- 735 ILCS 5/15-1401, Illinois Compiled Statutes

To safeguard against future liability, make sure you secure a written agreement – like an estoppel affidavit or settlement agreement – that confirms the lender has forgiven the deficiency and releases you from any further obligations. Addressing these details early in the negotiation process can also help you avoid unexpected tax issues or risks to other assets. Be sure to verify whether your loan is categorized as recourse or non-recourse. Most residential loans fall under recourse debt, meaning the lender could go after your other assets if needed.

There’s one more thing to keep in mind: forgiven debt often comes with tax consequences. The IRS usually treats canceled debt as taxable income, and lenders may report it using Form 1099-C. Consulting a tax professional can help you figure out if you qualify for any exemptions. While paying taxes on forgiven debt may not be ideal, it’s usually a better outcome than dealing with ongoing collection efforts for unpaid deficiencies.

To navigate these legal and financial complexities, consider reaching out to Foreclosure Defense Group for professional advice.

4. Credit Impact and Tax Implications

When considering a deed-in-lieu of foreclosure, it’s important to understand how it affects both your credit score and tax obligations.

A deed-in-lieu will negatively impact your credit, though not as severely as a full foreclosure. For example, your FICO score could drop by 50–125 points, depending on your starting score. Homeowners with higher scores (around 780) might see a larger drop of 105–125 points, while those with lower scores (around 680) may experience a smaller decline of 50–70 points. For comparison, a foreclosure typically results in a 85–160 point drop, while bankruptcy can cause a decline of 130–240 points.

On your credit report, the deed-in-lieu will be recorded as "closed but not paid as agreed" or "not paid in full." This notation can remain for up to seven years from the date of your first missed payment. However, you may still qualify for a new conventional mortgage in as little as four years, or even two years if you can prove extenuating circumstances.

"Ultimately, foreclosures, short sales, and deeds in lieu of foreclosure are all similarly bad for your credit. Bankruptcy is worse."

- Amy Loftsgordon, Attorney, Nolo

There’s also the tax side to consider. If your lender forgives the deficiency amount, the IRS may treat that forgiven debt as taxable income. Be sure to consult a tax professional to understand potential consequences, including any Form 1099-C filings, and to check if you qualify for exemptions under the Consolidated Appropriations Act.

To reduce the impact on your credit, you can request that your lender report the account as having a $0 balance once the deed-in-lieu is finalized. Rebuilding your credit can also be achieved with tools like secured credit cards or credit-builder installment loans. For additional guidance, organizations like Foreclosure Defense Group can assist with navigating both the credit and tax challenges associated with a deed-in-lieu agreement.

5. Property Valuation and Appraisal Disputes

After navigating lender delays and lien issues, the appraisal process often introduces its own set of challenges in deed-in-lieu negotiations.

Disagreements over a property’s appraised value can quickly derail these negotiations. Lenders usually require an independent third-party appraisal to establish the fair market value (FMV) before agreeing to accept the deed. If the appraisal comes in lower than anticipated, it can disrupt the process and lead to a significant deficiency balance.

On the other hand, if the appraisal determines the property is worth more than the mortgage balance, lenders may reject the deal to avoid accusations of fraudulent conveyance from other creditors or bankruptcy courts. If the appraised value is significantly lower than the mortgage balance, you might face a large deficiency balance. Essentially, the appraisal not only verifies the market value but also helps address disputes related to the property’s condition.

"It is imperative that lenders obtain an independent third-party appraisal to substantiate the value of the property in relation to the amount of debt being forgiven."

- Meghan A. Hayden, Member, Harris Beach Murtha

The condition of the property plays a critical role in determining its appraised value. Homes that are damaged, poorly maintained, or require environmental cleanup often receive lower valuations. Even if you believe your property is in good shape, lenders might still account for the cost of necessary repairs to make the title marketable. Keeping your property well-maintained before the appraisal can improve your chances of securing a favorable valuation.

If you disagree with the lender’s appraisal, closely review the report and check public records for errors, such as incorrect legal descriptions or outdated ownership details. Should the appraisal indicate equity in the property, you might negotiate compensation for the difference or explore a traditional sale. Additionally, if the appraisal values your property below the outstanding debt, ensure your deed-in-lieu agreement includes a written waiver of any deficiency balance.

Conclusion

Deed-in-lieu negotiations involve much more than just transferring a property title. Challenges like lender delays, lien complications, deficiency judgments, credit score impacts, and appraisal disagreements require careful planning. These agreements are highly negotiable, and the strength of your bargaining position can play a big role in determining the final outcome.

Without proper guidance, you could face unfavorable terms, surprise tax bills on forgiven debt, or ongoing deficiency claims. As Meghan A. Hayden from Harris Beach Murtha explains:

"A deed in lieu of foreclosure can be a faster and more economical alternative to the long and protracted foreclosure process".

However, this is only true when the agreement is structured correctly. The complexity of these negotiations makes expert legal advice essential.

Legal professionals can help secure deficiency waivers, include anti-merger clauses to protect against liens, and clarify whether the debt is recourse or non-recourse, reducing future liability and potential tax issues . This is where the Foreclosure Defense Group comes in.

Foreclosure Defense Group specializes in providing experienced legal support for deed-in-lieu negotiations. Their attorneys work to speed up lender approval by ensuring all documentation is complete, structuring deals to fit your needs, and fostering cooperation throughout the process – all starting with a free consultation.

FAQs

Does a deed-in-lieu stop foreclosure immediately?

A deed-in-lieu of foreclosure won’t put an immediate halt to the foreclosure process. Instead, it’s an option where you voluntarily transfer ownership of your property to the lender to sidestep the lengthy foreclosure proceedings. However, its success hinges on your lender’s approval and the details of your situation. While this can be a useful alternative, it requires close coordination with your lender and may take some time to complete.

How do I find and clear junior liens before applying?

To address junior liens before pursuing a deed-in-lieu, the first step is conducting a title search. This helps identify any secondary liens on the property, such as second mortgages or tax liens. After identifying these liens, the next move is to negotiate with lienholders. Work towards paying off or settling the amounts owed to clear the liens. Once agreements are reached, ensure all liens are officially released and properly recorded. Finally, it’s important to perform another title search to confirm the property is now free of junior liens.

How can I make sure I won’t owe a deficiency afterward?

When considering a deed in lieu of foreclosure, it’s crucial to protect yourself from owing any leftover debt, known as a deficiency. To do this, make sure the lender provides a written agreement stating they will accept the deed as full payment of your mortgage. This written assurance should also confirm that they won’t pursue a deficiency judgment against you.

Additionally, pay attention to any junior liens, such as second mortgages or home equity loans, as these can complicate the process. Addressing these liens upfront is essential to avoid future financial headaches.

For peace of mind, consult a legal professional to review your agreement. They can help ensure it includes a clear release from all deficiency liabilities, safeguarding you from unexpected obligations down the road.

Related Blog Posts

- Deed in Lieu vs. Short Sale: Understanding Your Options

- Checklist for Negotiating Deed-in-Lieu with Lenders

- Lender Requirements for Deed-in-Lieu Documents

- Top 3 Scenarios for Deed-in-Lieu Over Foreclosure