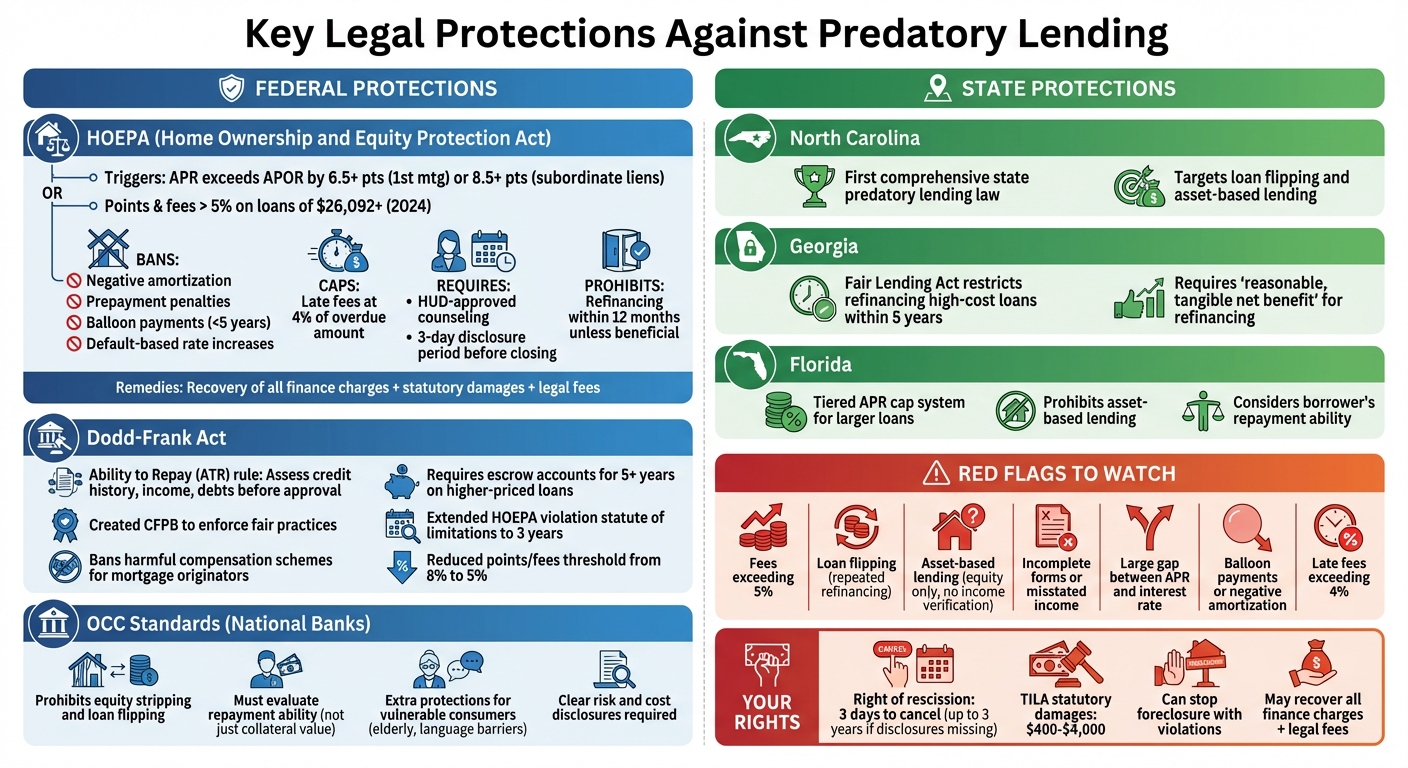

Predatory lending exploits borrowers through unfair terms, hidden fees, and abusive practices, often targeting vulnerable groups like low-income individuals and minorities. It can trap borrowers in cycles of debt, with tactics like loan flipping, equity stripping, and hidden costs in loans. Federal laws, such as HOEPA and the Dodd-Frank Act, alongside state-specific rules, help protect homeowners by requiring clear disclosures, banning harmful terms, and ensuring lenders assess a borrower’s ability to repay.

Key protections include:

- HOEPA: Caps fees, bans negative amortization, and mandates counseling for high-cost loans.

- Dodd-Frank Act: Introduces the Ability to Repay (ATR) rule and establishes the CFPB to enforce fair practices.

- State laws: North Carolina, Georgia, and Florida enforce additional safeguards like APR caps and restrictions on loan flipping.

To fight predatory lending, borrowers should watch for red flags like excessive fees or misleading terms and seek legal help to challenge violations. These protections empower homeowners to defend against abusive lending practices and avoid foreclosure.

Key Federal and State Protections Against Predatory Lending

What Are Your Rights Against Illegal Predatory Loan Practices? – America First Democrats

sbb-itb-d613a70

Federal Laws Protecting Homeowners from Predatory Lending

Federal laws set clear boundaries for lenders, ensure transparency through required disclosures, and give borrowers legal options to fight against abusive lending practices.

Home Ownership and Equity Protection Act (HOEPA)

HOEPA focuses on curbing exploitative practices in high-cost loans. These loans are identified when the annual percentage rate (APR) exceeds the Average Prime Offer Rate by more than 6.5 percentage points for first mortgages or 8.5 percentage points for subordinate liens. For loans of $26,092 or more (as of 2024), they also qualify if points and fees exceed 5% of the total loan amount.

The law outright bans several harmful practices. For instance, it prohibits negative amortization, where loan balances grow due to insufficient payments, and eliminates prepayment penalties for high-cost mortgages. It also outlaws balloon payments on loans with terms under five years and caps late fees at 4% of the overdue amount. Additionally, lenders cannot increase interest rates simply because a borrower defaults.

Borrowers taking high-cost mortgages must receive HUD-approved counseling and written disclosures at least three business days before closing. This ensures they fully understand the loan terms. Refinancing a HOEPA loan into another within 12 months is also prohibited unless the new loan offers clear benefits to the borrower.

Initially, HOEPA only applied to refinances and home equity loans. However, the Dodd-Frank Act expanded its protections to include purchase-money mortgages and Home Equity Lines of Credit (HELOCs). Lenders must now verify a borrower’s ability to repay using their income, employment status, and debts rather than relying solely on the home’s value. If a lender violates HOEPA, borrowers can recover all finance charges and fees paid, along with statutory damages, court costs, and attorney fees.

Dodd-Frank Act Mortgage Reforms

The Dodd-Frank Act introduced major changes after the 2008 financial crisis to reduce risky lending practices. One of its key provisions is the Ability to Repay (ATR) standard, which requires lenders to assess a borrower’s credit history, income, and financial obligations before approving a loan.

The Act also established the Consumer Financial Protection Bureau (CFPB) to enforce rules against deceptive mortgage practices. CFPB Director Richard Cordray emphasized its importance, stating:

"Today’s changes will better help consumers to understand the real costs of owning a home while protecting them from harmful practices that can trap them into high-cost mortgages."

Other reforms include banning compensation schemes that incentivize mortgage originators to push borrowers toward unaffordable loans. For higher-priced loans, creditors must set up escrow accounts for at least five years to cover property taxes and insurance. The statute of limitations for HOEPA violations was also extended to three years, and the points and fees threshold for high-cost mortgages was reduced from 8% to 5% for loans of $20,000 or more.

These reforms work alongside other federal measures to strengthen borrower protections.

OCC Anti-Predatory Standards for National Banks

The Office of the Comptroller of the Currency (OCC) enforces strict lending guidelines for national banks and federal savings associations. Under its Guidelines for Residential Mortgage Lending Practices (12 CFR Appendix C to Part 30), the OCC prohibits practices like equity stripping – charging excessive fees that drain a homeowner’s equity – and loan flipping, where refinancing offers no real financial benefit.

National banks must evaluate a borrower’s ability to repay rather than relying on the foreclosure or liquidation value of the home. The OCC guidelines state:

"Loans that involve… mortgage loans based predominantly on the foreclosure or liquidation value of the borrower’s collateral without regard to the borrower’s ability to repay the loan according to its terms, will involve violations of OCC regulations."

The OCC also requires lenders to take extra care when offering products to vulnerable consumers, such as the elderly or those with language barriers. Disclosures must clearly explain risks and costs. These rules apply to loans secured by owner-occupied homes, including cooperative units and mobile homes.

If you believe a national bank has engaged in abusive practices, you can file a complaint through the OCC’s portal at HelpWithMyBank.gov. Since federal standards typically override state predatory lending laws for national banks, understanding these protections is crucial when dealing with federally chartered institutions.

State Laws Protecting Against Predatory Lending

Federal laws provide a foundation for protecting homeowners, but many states have added their own rules to address specific needs and close any gaps. These state laws often reflect local market conditions and offer tailored safeguards that go beyond federal protections.

Florida Anti-Predatory Lending Provisions

Florida enforces a tiered system for APR (Annual Percentage Rate) caps to limit excessive interest rates on larger loans. Additionally, the state prohibits asset-based lending, which involves approving loans solely based on a home’s equity rather than the borrower’s income. This ensures that lenders consider a homeowner’s ability to repay before issuing a loan.

North Carolina and Georgia State Laws

North Carolina led the way in combating predatory lending by implementing one of the first comprehensive state laws. This legislation directly addresses harmful practices like loan flipping and asset-based lending.

Georgia’s Fair Lending Act takes a strong stance against loan flipping as well. It prohibits refinancing high-cost home loans within a five-year period unless the borrower gains a "reasonable, tangible net benefit" from the new loan. This rule helps protect homeowners from losing equity through repeated and unnecessary refinancing.

These state-specific measures aim to curb abusive lending practices while also setting limits on overall credit costs.

State APR Caps and Enforcement

APR caps vary from state to state, setting maximum limits on the total cost of credit. The level of protection homeowners receive often depends on these local regulations.

| State | Key Protection Feature |

|---|---|

| North Carolina | Comprehensive measures targeting loan flipping and asset-based lending |

| Georgia | Restricts refinancing high-cost loans within five years unless it benefits the borrower |

| Florida | Tiered APR cap system and restrictions on asset-based lending |

Strong enforcement mechanisms ensure lenders adhere to these rules, preventing them from exploiting loopholes in state laws.

Using Legal Protections to Fight Predatory Lending

Recognizing Predatory Lending Practices

Spotting predatory lending starts with identifying the red flags. For example, if fees exceed 5%, it could signal predatory behavior that legal protections are designed to address. Another common tactic is loan flipping, where lenders push borrowers to refinance repeatedly, racking up fees each time. Similarly, asset-based lending, which approves loans based on home equity rather than the borrower’s ability to repay, is another warning sign.

"Predatory lending involves forcing high-cost loan terms and excessive fees upon unsuspecting borrowers usually through aggressive and deceitful lending tactics."

– Robert Rafii, Esq.

Be cautious of deceptive sales tactics, like being asked to sign incomplete forms or documents with misstated income. Watch for altered interest rates at closing, balloon payments, or negative amortization, which can lead to spiraling debt. One helpful tip: compare your APR to your interest rate – if there’s a big gap, hidden costs might be lurking. Under HOEPA regulations, late fees cannot legally exceed 4% of the overdue payment.

Recognizing these practices helps you know when it’s time to seek legal support.

Getting Legal Help

Navigating homeowner laws at the federal and state levels can be overwhelming without professional guidance. Experienced attorneys are skilled at spotting violations, such as improper APR disclosures or missing rescission notices under TILA. The right of rescission allows borrowers to cancel a loan within three days – or even up to three years if key disclosures were missing.

"Rescission voids a creditor’s lien, eliminating the creditor’s foreclosure remedy and ultimately taking away that creditor’s leverage."

– Amy Loftsgordon, Attorney

Legal help becomes even more critical if you’re facing foreclosure. Federal and state laws offer protections that can stop foreclosure proceedings. For instance, when a loan is already in foreclosure, even a small finance charge error – sometimes as little as $35 – can trigger rescission rights. Attorneys can also file RESPA requests to obtain closing documents, which may reveal additional violations. Courts may order lenders to modify loan terms, cancel debts, or even cover your legal fees if violations are proven.

These legal tools give borrowers the power to stand up to unfair practices.

How Foreclosure Defense Group Helps Homeowners

Foreclosure Defense Group specializes in protecting homeowners from predatory lending and foreclosure by utilizing legal protections. Their attorneys carefully review loan documents to uncover violations of TILA, HOEPA, or state laws. They handle everything from negotiating loan modifications to representing clients in court, using tools like rescission to eliminate creditor liens and stop foreclosures.

The firm offers free consultations to explore your options. Whether you’re dealing with excessive fees, misleading loan terms, or the threat of losing your home, they tailor their strategies to your specific situation. Services include foreclosure defense, bankruptcy assistance, loan modification, and forbearance programs – all aimed at helping you protect your home and regain financial stability. Visit https://foreclosuredefensegroup.com to schedule your free consultation and take the first step toward safeguarding your rights.

Conclusion

Federal and state laws provide crucial tools for homeowners to combat predatory lending practices. Key regulations like the Truth in Lending Act (TILA), HOEPA, and the Dodd-Frank Act’s Ability to Repay rule ensure lenders clearly disclose loan terms and verify a borrower’s repayment ability before issuing loans. On top of that, states such as North Carolina and Georgia often enforce even stricter safeguards, offering an added layer of protection for borrowers.

Understanding your rights and taking action promptly is essential. With the Consumer Financial Protection Bureau (CFPB) scaling back its supervision and enforcement efforts as of February 2025, federal oversight may no longer catch violations as effectively. This shift places a heavier burden on homeowners to seek legal support when facing questionable lending practices.

"Homeowners and borrowers will have to more heavily rely on legal representation to defend their rights and challenge wrongful foreclosures."

– Amy Loftsgordon, Attorney

If you suspect predatory lending or are dealing with foreclosure, don’t wait to act. Legal professionals can identify violations – such as improper APR disclosures or missing rescission notices – and use them to halt foreclosures, renegotiate loan terms, or even cancel debt. Under TILA, statutory damages can range from $400 to $4,000, offering some financial relief.

FAQs

Does my mortgage qualify as a high-cost (HOEPA) loan?

If your mortgage’s interest rate or fees exceed specific thresholds, it might fall under the category of a high-cost (HOEPA) loan. For instance, this could happen if the interest rate is more than 8 percentage points above the treasury rate for first-lien loans or 10 percentage points above for second-lien loans. Similarly, if the total points and fees go beyond certain limits, your loan might also qualify. To be sure, it’s a good idea to review the criteria carefully or consult a legal professional for clarification.

What documents should I gather if I suspect predatory lending?

If you think you might be dealing with predatory lending, it’s important to gather documentation that highlights the loan terms and the process you went through. Key documents to collect include:

- Loan applications and any disclosures to confirm the original terms offered.

- The Loan Estimate and Closing Disclosure, which detail costs and fees associated with the loan.

- Promissory notes, payment histories, and amortization schedules to keep track of payments and loan progress.

- Any correspondence with the lender to have a record of your communications.

These documents not only help you evaluate the fairness of the loan but can also serve as crucial evidence if legal action becomes necessary.

Can I rescind my mortgage loan after closing?

Yes, if your mortgage is a non-purchase money loan – like a refinance or a home equity loan – you have a three-business-day window to cancel it. This is called the right of rescission and takes effect after the loan closes. However, it does not apply to purchase money mortgages, which are loans used to buy a home.

Related Blog Posts

- How Attorneys Help Resolve Mortgage Disputes

- Foreclosure Defense: Preventing Costly Errors

- Wrongful Foreclosure: Key Legal Rights Explained

- Common Lender Errors in Foreclosure Cases