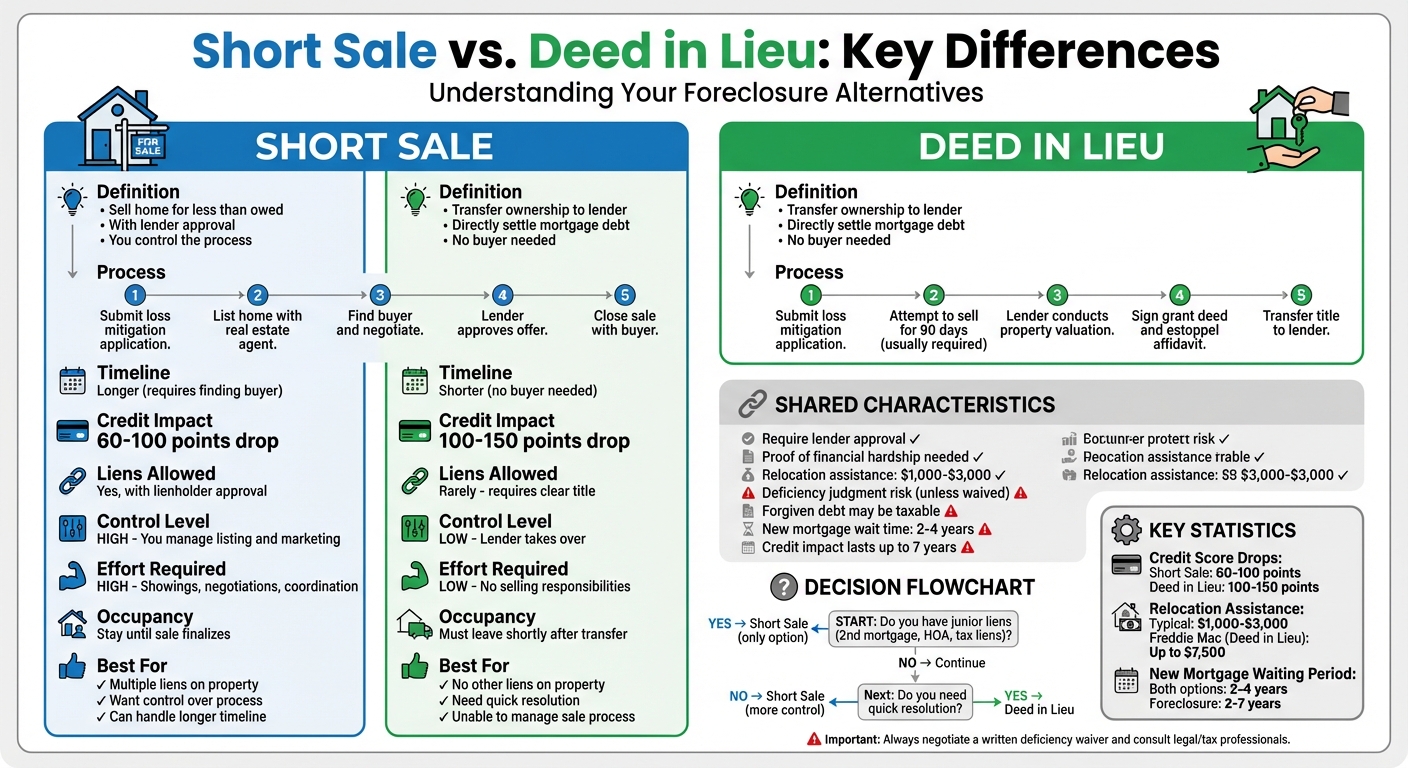

When struggling with mortgage payments, two alternatives to foreclosure are short sales and deeds in lieu of foreclosure. Both options can help you avoid the lengthy foreclosure process, but they work differently:

- Short Sale: You sell your home for less than what you owe, with lender approval. You stay involved in the process, market the home, and negotiate with buyers.

- Deed in Lieu: You transfer ownership of your home directly to the lender, avoiding the need to sell. This option is faster but requires a clear title with no other liens.

Key Considerations:

- Both impact your credit score (drops of 100+ points are common).

- Lenders may offer relocation assistance ($1,000–$3,000).

- Forgiven debt may be taxable unless exclusions like the Qualified Principal Residence Indebtedness (QPRI) apply.

- Short Sale: Better if you have multiple liens or want more control.

- Deed in Lieu: Better for quicker resolution if no other liens exist.

Quick Comparison:

| Feature | Short Sale | Deed in Lieu |

|---|---|---|

| Process | Sell to a buyer with lender’s OK | Transfer title to lender |

| Time | Longer (requires finding a buyer) | Shorter (no buyer needed) |

| Liens Allowed | Possible with lienholder approval | Rarely allowed |

| Credit Impact | 60–100 points drop | 100–150 points drop |

| Relocation Assistance | Often available | Often available |

Both options require lender approval and proof of financial hardship. To choose the best option, consider your financial situation, timeline, and whether your property has additional liens. Always negotiate a deficiency waiver to protect against future debt collection and consult a legal or tax professional for guidance.

Short Sale vs Deed in Lieu: Complete Comparison Guide

Deed in Lieu vs Short Sale [Difference Between the Two]

What is a Short Sale?

A short sale allows you to sell your home for less than what you owe on your mortgage – provided your lender agrees. In this arrangement, the lender must approve the sale and release their lien, even though they won’t recoup the full amount you originally borrowed.

Unlike a foreclosure, where the bank takes ownership of your property through legal action, a short sale gives you more control. You work with a buyer to sell the home, and all proceeds go directly to your lender. From there, the lender decides whether to forgive the remaining balance or seek repayment for the difference.

How a Short Sale Works

The process begins with submitting a Request for Mortgage Assistance (RMA) and providing supporting documents like tax returns, pay stubs, bank statements, and a hardship letter. The hardship must stem from a recent event – such as losing your job, a divorce, or unexpected medical expenses – not from circumstances that existed when you first got the loan.

Once your lender reviews your application, you list your home for sale with a real estate agent. When a buyer makes an offer, the lender evaluates it – a step that can take several weeks. For the sale to close, all lienholders must approve the transaction.

"A short sale in real estate is an offer of a property at an asking price that is less than the amount due on the current owner’s mortgage." – Investopedia

While the process involves multiple steps, it offers a structured way to avoid foreclosure.

When to Consider a Short Sale

A short sale might be the right choice if your home is underwater (worth less than what you owe) and you’re facing financial hardship, especially if there are multiple liens on the property. Unlike foreclosure, which typically results in a waiting period of two to seven years before you can qualify for a new mortgage, some homeowners who complete a short sale may be eligible for a new loan in as little as two years. Another advantage is avoiding the term "foreclosure" on your credit report, although both options negatively impact your credit score.

It’s crucial to get written confirmation from your lender that they will waive the deficiency balance. Without this agreement, the lender could still pursue you for the difference between what you owed and the final sale price of the home.

Up next, we’ll look at other options, such as a deed in lieu of foreclosure, which may fit different financial situations.

What is a Deed in Lieu of Foreclosure?

A deed in lieu of foreclosure is a voluntary agreement between you and your lender where you transfer ownership of your home directly to the lender to settle your mortgage debt. This arrangement allows you to avoid the lengthy and public foreclosure process by handing over the property title and walking away from the mortgage.

"A deed-in-lieu of foreclosure is an arrangement where you voluntarily turn over ownership of your home to the lender to avoid the foreclosure process." – Consumer Financial Protection Bureau

For this option to work, both parties need to agree. The lender must accept the property, and you must be prepared to give up ownership. Unlike foreclosure, which becomes part of the public record, a deed in lieu remains a private agreement between you and the lender.

How a Deed in Lieu Works

The process starts by contacting your loan servicer to request a loss mitigation package. You’ll need to provide documentation such as two years of tax returns, recent pay stubs, bank statements, and a hardship affidavit explaining why you can no longer make your mortgage payments. The lender will then conduct a property valuation, typically through a Broker Price Opinion (BPO), and perform a title search to ensure there are no additional liens on the property.

Most lenders will only consider this option if the property has a clear title, free of second mortgages, tax liens, or homeowners association (HOA) judgments. Additionally, many lenders require you to first attempt to sell the home at fair market value for at least 90 days before they’ll agree to a deed in lieu.

If approved, you’ll sign a Grant Deed to transfer ownership and an Estoppel Affidavit to confirm the terms and your voluntary participation. While this process avoids foreclosure, it comes with its own challenges and requirements.

When to Consider a Deed in Lieu

A deed in lieu might make sense if you’ve unsuccessfully tried to sell your home for several months. It’s particularly appealing if your lender offers relocation assistance, such as "cash-for-keys" programs that provide up to $3,000 to cover moving expenses. Some programs, like Fannie Mae’s Mortgage Release, may even allow you to stay in the home rent-free for up to three months or lease it for up to 12 months.

This option is most suitable if you owe more on your mortgage than your home is worth, there are no other liens on the property, and you need a quicker resolution than a short sale. However, keep in mind that mortgage waiting periods after a deed in lieu typically range from two to four years, and your credit score could drop by 50 to 125 points, with the impact lasting up to seven years.

"It might not be worth doing a deed in lieu of foreclosure unless you can get the bank to agree to forgive or reduce the deficiency, you get some cash as part of the transaction, or you receive extra time to stay in the property." – Amy Loftsgordon, Attorney

Key Differences Between Short Sale and Deed in Lieu

Short sales and deeds in lieu offer two distinct ways to avoid foreclosure, each with its own process and requirements. In a short sale, you actively market your home – working with a real estate agent, hosting open houses, and negotiating with buyers – until you secure an offer, even if the sale price is less than your remaining mortgage balance.

A deed in lieu, on the other hand, skips the need for buyer negotiations. Instead, you transfer your property’s title directly to the lender. However, most lenders require the home to be listed for sale for at least 90 days before considering this option. As attorney Amy Loftsgordon explains:

"Banks would rather have you sell the house than have to sell it themselves".

Short sales can sometimes address subordinate liens if lienholders agree to partial payouts, while deeds in lieu usually require a clear title with no additional liens. The paperwork also differs: short sales involve a standard real estate closing, while deeds in lieu require a grant deed and an estoppel affidavit. The affidavit confirms that the transfer is voluntary and outlines whether the lender waives its right to pursue remaining debt.

These differences highlight unique aspects of each approach, from the process to the documentation and final outcomes.

Process Comparison Table

Here’s a side-by-side look at the key steps involved in each option:

| Feature | Short Sale | Deed in Lieu of Foreclosure |

|---|---|---|

| How it Starts | Submit a loss mitigation application and list the home for sale. | Submit a loss mitigation application; often, the home must be listed for 90 days. |

| Required Documents | Financial statement, tax returns, bank statements, hardship affidavit, and a purchase offer. | Financial statement, tax returns, bank statements, hardship affidavit, and an estoppel affidavit. |

| Lender Approval | Lender must approve the buyer’s purchase offer. | Lender must agree to take the title directly; typically, no other liens are allowed. |

| Property Marketing | Required; you must actively find a buyer. | Not required for the final transfer, though listing for a set period is often mandatory. |

| Title Transfer | Transferred from you to a third-party buyer. | Transferred directly to the lender. |

| Subordinate Liens | Possible if lienholders agree to a partial payout. | Rarely approved; most lenders require no other liens. |

Pros and Cons of Each Option

When deciding between a short sale and a deed in lieu of foreclosure, it’s important to weigh the trade-offs in cost, timing, and effort. Both options come with their own set of challenges and benefits.

A short sale gives you more control over the process. You’ll work with a real estate agent to market your home and negotiate with buyers. In some cases, lenders might cover closing costs and even offer relocation assistance. However, there’s a lot of work involved – hosting open houses, waiting for offers, and coordinating with multiple parties. If your property has junior liens, you’ll also need to get all lienholders to agree to accept less than what they’re owed, which can complicate matters.

On the other hand, a deed in lieu of foreclosure removes the responsibility of selling the property yourself. Attorney Amy Loftsgordon explains it well:

"One benefit to a deed in lieu is that you don’t have to take responsibility for selling your house."

This option usually offers quicker relief, but there are drawbacks. Most lenders won’t accept a deed in lieu if there are any other liens on the property, and you’ll likely need to vacate the home much sooner – often within weeks of transferring the title.

Credit and Tax Implications

Both options will have a notable impact on your credit score, potentially lasting up to seven years. A short sale typically results in a credit score drop of 60–100 points, while a deed in lieu can cause a drop of 100–150 points, similar to a foreclosure. Additionally, unless the lender provides a written waiver, they may still pursue the remaining balance. Forgiven debt may also be taxable unless you qualify for exclusions or insolvency conditions.

Advantages and Disadvantages Comparison Table

Here’s a side-by-side look at the key differences between the two options:

| Feature | Short Sale | Deed in Lieu of Foreclosure |

|---|---|---|

| Control Over Process | You handle listing and marketing the home. | Lender takes over; you transfer the title. |

| Timeline | Can take months to sell and close. | Generally faster than a short sale or foreclosure. |

| Effort Required | High – requires showings, negotiations, and coordinating buyers. | Low – no selling responsibilities. |

| Junior Liens | Possible if all lienholders agree to partial payouts. | Rarely approved; lenders usually require a clear title. |

| Credit Score Drop | Typically 60–100 points (up to 150 in some cases). | Typically 100–150 points, similar to foreclosure. |

| Occupancy | You stay in the home until the sale is finalized. | You must leave shortly after the title transfer. |

| Relocation Assistance | Often includes $1,000–$3,000 or more. | May be offered, typically starting around $1,000. |

| Deficiency Risk | High unless waived in writing. | High unless waived in writing. |

| Tax Liability | Forgiven debt may be taxable via a 1099-C. | Forgiven debt may be taxable via a 1099-C. |

| Lender Preference | Preferred by most banks. | Less preferred; requires the lender to manage and sell the property. |

sbb-itb-d613a70

Eligibility Requirements and Proof of Financial Hardship

If you’re considering a short sale or a deed in lieu of foreclosure, you’ll need to demonstrate long-term financial hardship that makes keeping up with your mortgage impossible. Lenders typically look for life-altering events beyond your control – think job loss, a severe illness, divorce, the death of a co-borrower, or a drastic drop in income.

Start by contacting your mortgage servicer to request loss mitigation forms. Be ready to provide key documents like two years of tax returns, two months of recent bank statements, current pay stubs or profit and loss statements, and a clear, factual hardship affidavit. Attorney Amy Loftsgordon explains that a hardship is "a circumstance beyond your control that results in a situation where you can’t afford to make the required mortgage payments". When writing your hardship explanation, stick to the facts – include dates and specific details, and avoid emotional language.

Once you’ve gathered your hardship documentation, the eligibility criteria for a short sale or a deed in lieu will come into play.

For a short sale, your home must be worth less than the remaining mortgage balance (commonly referred to as being "underwater"). You’ll also need a legitimate purchase offer from a third-party buyer before most lenders will even consider your application. If there are junior liens (like a second mortgage), all lienholders must agree to take reduced payouts.

For a deed in lieu, the process is often more stringent. As Loftsgordon notes, "Generally, a bank will approve a deed in lieu only if the property has no liens other than the mortgage". Lenders also typically require proof that you’ve tried to sell the property at fair market value for at least 90 days without success. Additionally, the property must be in good condition – major repairs or structural damage could result in a denial. On a positive note, Freddie Mac offers up to $7,500 in relocation assistance to eligible homeowners who meet specific criteria.

Credit Impact and Deficiency Judgment Risks

Both a short sale and a deed in lieu can significantly impact your credit score, often lowering it by 100 points or more. According to attorney Amy Loftsgordon, these options are nearly as damaging as a foreclosure. However, one major benefit is avoiding the "foreclosure" label on your credit report. This distinction matters because a foreclosure carries a stigma with lenders and typically results in longer wait times before you can qualify for new financing.

When it comes to deficiency judgments, the risks vary depending on the option you choose. In a short sale, the deficiency is the gap between your mortgage balance and the sale price of the home. For a deed in lieu, the deficiency is calculated as the difference between your total debt and the property’s fair market value. In most states, lenders can legally pursue you for this shortfall unless you negotiate a written waiver. Some states, like California, prohibit deficiency judgments after short sales by law, while others, such as Nevada and Washington, have statutes that limit these judgments.

It’s crucial to ensure your agreement explicitly waives any deficiency judgment and confirms that your debt is fully satisfied. Keep in mind that if you have a second mortgage or an HOA lien, those lienholders may still pursue you for unpaid balances unless you negotiate separate waivers.

Another important consideration is the tax implications of forgiven debt. If the forgiven amount is $600 or more, you’ll receive a Form 1099-C, and this amount may be treated as taxable income unless exclusions apply. Fortunately, the Qualified Principal Residence Indebtedness (QPRI) exclusion protects many homeowners from this tax burden for debts forgiven through January 1, 2026. Additionally, if your total debts exceed your total assets at the time of forgiveness, you might qualify for the insolvency exception.

Credit and Deficiency Risk Comparison Table

| Feature | Short Sale | Deed in Lieu |

|---|---|---|

| Credit Score Drop | Severe (often 100+ points) | Severe (often 100+ points) |

| Credit Report Notation | "Settled for less than full balance" | "Satisfied" or "Deed in lieu" |

| Deficiency Calculation | Total debt minus sale price | Total debt minus fair market value |

| Deficiency Risk | High, unless waived in writing or prohibited by state law | Moderate to high, depending on agreement terms |

| State Protections | Prohibited in some states (e.g., California) | Rarely prohibited by law (exceptions in Nevada, Washington) |

| Tax Liability (1099-C) | Forgiven debt may be taxable income | Forgiven debt may be taxable income |

| New Mortgage Wait Time | 2–4 years | 2–4 years |

Understanding these differences in credit and deficiency risks is essential in deciding which option best suits your financial needs.

How to Choose Between a Short Sale and Deed in Lieu

Deciding between a short sale and a deed in lieu depends on your specific lien situation, how much time you have, and what your lender requires. If your property has additional liens – like a second mortgage, HOA dues, or tax liens – a deed in lieu is usually not an option. Lenders rarely accept a deed when the title has other claims attached. In such cases, a short sale is often your only practical choice.

Your timeline and willingness to manage the sales process also play a key role. A short sale involves listing your property, finding a buyer, and negotiating with your lender, which can take time. On the other hand, a deed in lieu is typically quicker once your lender agrees, but many lenders require you to attempt selling the property for at least 90 days before considering this option. Banks often prefer short sales because it spares them the hassle of managing the property and handling the sale themselves.

Whether you choose a short sale or a deed in lieu, make sure to negotiate a written deficiency waiver. Without it, your lender could pursue the remaining balance between what you owe and the amount recovered – either from the sale price (in a short sale) or the property’s value (in a deed in lieu). Some lenders might also offer relocation assistance, often between $1,000 and $3,000, to help with moving expenses. Be sure to inquire about "cash for keys" programs when discussing your agreement. Weigh these factors carefully against your broader financial situation to make an informed decision.

You should also check if you qualify for tax relief on forgiven debt. The Qualified Principal Residence Indebtedness (QPRI) exclusion, available through January 1, 2026, can shield you from having to pay taxes on forgiven mortgage debt. If QPRI doesn’t apply, see if you qualify under the insolvency exception, which applies if your total debts exceeded your total assets when the debt was forgiven. Consulting a tax professional or CPA is a smart step to avoid any unexpected tax liabilities.

Finally, seek advice from experienced legal professionals to guide you through lender negotiations, safeguard your rights, and ensure all agreements are properly documented. For personalized assistance, Foreclosure Defense Group offers expertise in evaluating short sales and deeds in lieu, helping homeowners secure favorable terms and avoid costly errors during this complex process.

Working with Legal Professionals

Navigating a short sale or deed in lieu without the guidance of a legal expert can be a risky move. Banks often don’t waive deficiency judgments, and laws vary from state to state. This is where an experienced foreclosure attorney becomes essential. As attorney Amy Loftsgordon explains: "To ensure that the bank can’t get a deficiency judgment against you following a short sale, you need to make sure that the short sale agreement expressly says that the transaction is in full satisfaction of the debt and that the bank waives its right to the deficiency".

Legal professionals also play a crucial role in coordinating with multiple lienholders. If your property has a second mortgage, unpaid HOA dues, or tax liens, every lienholder must agree to release their claim. Junior lienholders, in particular, are often reluctant to cooperate since they may receive little to nothing from the sale proceeds. Here, an attorney can step in to negotiate a carve-out from the first mortgage holder, ensuring the deal moves forward. This process naturally involves a careful review of all relevant documents.

Attorneys meticulously examine documents like estoppel affidavits and short sale agreements to protect you from hidden clauses that might allow the bank to pursue a deficiency later. State laws can vary widely. For instance, in California, deficiency judgments are prohibited after short sales and deeds in lieu. A lawyer familiar with your state’s foreclosure laws can determine if you’re already protected or if additional negotiation is required.

Beyond document review, legal counsel can uncover foreclosure defenses that may strengthen your negotiating position. Errors or procedural violations by your mortgage servicer could provide leverage, encouraging the lender to accept your short sale or deed in lieu under better terms. Attorneys can also negotiate for relocation assistance – often ranging from $1,000 to $3,000 – through cash-for-keys programs that banks sometimes offer to avoid drawn-out foreclosure proceedings. With this level of legal support, you can approach the process with clarity and confidence.

For those seeking experienced legal representation, Foreclosure Defense Group (https://foreclosuredefensegroup.com) offers comprehensive services. Their attorneys handle lender negotiations, ensure agreements include proper deficiency waivers, and work with junior lienholders to secure the best possible outcomes.

Conclusion

When weighing the choice between a short sale and a deed in lieu, it’s clear that both options come with serious consequences and considerations. Each can impact your credit, potentially lead to tax liabilities, and carry the risk of deficiency judgments unless explicitly waived in writing. If the difference between your total debt and what the lender recovers isn’t addressed in your agreement, you could even face legal action for the remaining balance.

The best option depends entirely on your financial situation. For instance, if your property has multiple liens or you want to maintain control over the sale process, a short sale might be the way to go. On the other hand, if you need a quicker solution and your home has no junior lienholders, a deed in lieu might be the simpler choice. These decisions highlight the importance of seeking professional advice.

It’s also essential to remember that forgiven debt is taxable unless it qualifies for exclusions like the Qualified Principal Residence Indebtedness exclusion. Consulting a tax expert can help you navigate this complex area.

State laws can significantly influence your decision. For example, California prohibits deficiency judgments after short sales, but many other states don’t offer the same protection. Given these differences, working with an experienced foreclosure attorney is invaluable. They can review your agreements, negotiate with lienholders, and ensure you fully understand the terms before signing. As Bills.com editor Mark Cappel wisely points out:

"An attorney’s time is not cheap, but will be a bargain compared to signing an agreement you do not understand and are surprised later to realize its implications".

For those in need of legal assistance, Foreclosure Defense Group (https://foreclosuredefensegroup.com) provides skilled representation to handle lender negotiations, secure deficiency waivers, and safeguard your financial future. Taking the time to carefully evaluate your options with the help of professionals can make all the difference between a manageable fresh start and years of financial challenges.

FAQs

What should I consider when deciding between a short sale and a deed in lieu of foreclosure?

When choosing between a short sale and a deed in lieu of foreclosure, understanding how each option aligns with your financial circumstances and long-term goals is essential. Both approaches aim to prevent foreclosure, but they work differently and have unique implications.

A short sale involves selling your home for less than the remaining mortgage balance, with your lender agreeing to the terms. On the other hand, a deed in lieu of foreclosure allows you to hand over ownership of the property directly to the lender, bypassing the foreclosure process entirely.

Here are some key points to think about:

- Impact on Credit: Both options will affect your credit score, but a short sale may have a slightly smaller impact, especially if handled properly.

- Lender Requirements: Each option comes with specific approval criteria set by the lender. It’s important to understand what your lender requires before moving forward.

- Future Mortgage Opportunities: If you’re planning to buy another home down the line, a short sale might make you eligible for a new mortgage sooner compared to a deed in lieu, depending on the situation.

To navigate these options and make an informed decision, consulting professionals like the team at Foreclosure Defense Group can provide valuable guidance tailored to your unique financial situation.

How do I negotiate a deficiency waiver with my lender?

To work toward a deficiency waiver, your first step should be reaching out to your lender as soon as you realize you’re facing financial difficulties. Be upfront about your situation and back up your claims with supporting documents. These might include recent pay stubs, tax returns, a detailed budget, and a hardship letter explaining why you’re no longer able to keep up with your mortgage payments. Lenders are often willing to consider waiving the deficiency if a short sale or deed in lieu of foreclosure can save them the higher expenses tied to foreclosure.

When negotiating, aim for a complete release from the deficiency balance – this is the gap between what you owe on the mortgage and the sale price of the property. If the lender resists, you might suggest settling for a reduced amount instead. Whatever terms you agree upon, make sure everything is documented in writing and signed by an authorized representative before completing the short sale or deed in lieu. This written agreement is crucial for protecting yourself from potential collection efforts down the line.

Because the process can be tricky and lenders often have strict rules, working with an experienced legal professional can make a big difference. A legal expert can help you gather the right documents, handle negotiations with your lender, and secure a deficiency waiver that helps protect your financial future.

Will forgiven mortgage debt affect my taxes?

Yes, forgiven mortgage debt is usually treated as taxable income by the IRS. However, thanks to the Mortgage Forgiveness Debt Relief Act, which is extended through 2025, you might be able to exclude this amount from your federal taxes if it meets certain criteria. To navigate this and ensure you’re following IRS rules, it’s a good idea to consult with a tax professional who can guide you based on your unique circumstances.

Related Blog Posts

- Deed in Lieu vs. Short Sale: Understanding Your Options

- Checklist for Negotiating Deed-in-Lieu with Lenders

- Lender Requirements for Deed-in-Lieu Documents

- Top 3 Scenarios for Deed-in-Lieu Over Foreclosure