Struggling with Mortgage Payments? Explore Loan Modification Options

Homeownership can be a dream until financial challenges strike, leaving you worried about losing your home. If you’re finding it hard to keep up with mortgage payments due to unexpected hardships like job loss or medical bills, a loan modification might be a lifeline. This process adjusts the terms of your loan to make it more manageable, potentially saving you from foreclosure.

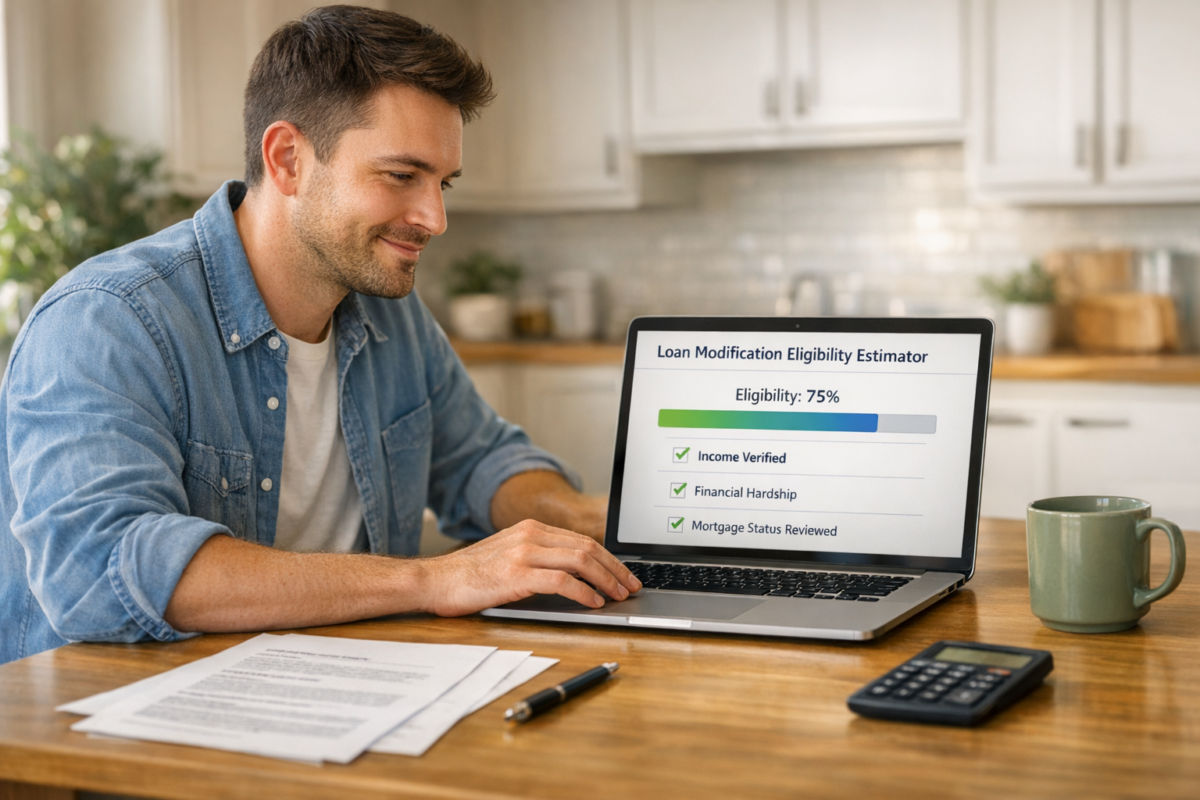

How to Know If You Qualify for Help

Eligibility for mortgage relief often depends on factors like your debt-to-income ratio, the type of loan you have, and the nature of your financial struggle. Programs vary—FHA loans might qualify for specific federal assistance, while conventional loans could have different pathways. The key is understanding where you stand. Tools like our estimator can provide a quick glimpse into whether you might meet the basic thresholds for a revised payment plan.

Taking the Next Step

If you’re curious about your options, start by gathering details about your income, expenses, and loan. Then, reach out to your lender or a trusted housing counselor. They can guide you through the specifics and help secure a solution tailored to your situation. Remember, acting early can make all the difference in protecting your home.

FAQs

What exactly is a loan modification?

A loan modification is a change to your existing mortgage terms, often to make payments more affordable. This could mean lowering your interest rate, extending the loan term, or even reducing the principal. It’s typically offered to homeowners facing financial hardship who want to avoid foreclosure. Our tool helps you gauge if you might qualify based on general criteria like debt-to-income ratio and documented struggles.

How accurate is this eligibility estimator?

This tool provides an estimate based on widely used guidelines for loan modification programs. It looks at factors like your income, expenses, and hardship reason to give you a sense of your chances—High, Moderate, or Low. That said, every lender and program has unique rules, so this isn’t a guarantee. We always recommend reaching out to your lender or a HUD-approved counselor for a definitive answer.

What should I do if my eligibility result is Low?

Don’t lose hope if your result shows a Low likelihood. This just means your current financial picture might not align with typical modification criteria. You can still explore other options like forbearance or refinancing. Contacting your lender directly is a great next step—they often have alternative solutions. Also, a HUD counselor can offer free, personalized advice to help you navigate this.