If you’re facing foreclosure, managing debt effectively can help protect your home. Here’s what you need to know:

- Prioritize Secured Debts: Pay your mortgage and car loans first, as these are tied to assets like your home.

- Understand Your Financial Situation: Calculate your debt-to-income (DTI) ratio and evaluate your cash flow to identify areas for improvement.

- Use Debt Payment Strategies: Apply the snowball method (smallest debts first) or avalanche method (highest interest rates first) to tackle debt systematically.

- Explore Refinancing or Loan Modifications: Lower your mortgage payments or restructure your loan to make payments more manageable.

- Negotiate with Creditors: Request lower payments, forbearance, or settlement options to free up funds for your mortgage.

- Consider Legal Options: Bankruptcy (Chapter 7 or 13) or alternatives like short sales can provide relief and prevent foreclosure.

Act quickly. Missing payments can limit your options, but early action – like consulting a HUD-approved counselor or attorney – can help you navigate your situation effectively.

11 Options to Defend Your Home – New Jersey Foreclosure Defense Lawyers

Evaluating Your Current Financial Position

Start by gathering the essential documents related to your loan. This includes your mortgage or deed of trust, promissory note, billing and escrow statements, property tax records, and any correspondence from your loan servicer. Next, compile proof of income, such as recent pay stubs, federal tax returns, bank statements, and documentation for other income sources like Social Security benefits, alimony, or rental income.

With these documents in hand, you can calculate your debt-to-income (DTI) ratio. This is done by dividing your total monthly debt payments by your gross monthly income (your income before taxes and deductions). For instance, if your monthly debt payments total $2,000 and your gross income is $6,000, your DTI is 33%. This ratio is crucial because lenders use it to assess your eligibility for options like loan modifications or repayment plans. Knowing your DTI helps you understand your financial boundaries and informs your review of cash flow.

Equally important is evaluating your cash flow. According to Foreclosure Defense Group, tracking your monthly cash flow can pinpoint the financial challenges that may lead to missed payments and growing expenses. Compare all sources of monthly income against your expenses – this includes mortgage payments, utilities, food, car payments, HOA fees, and other costs. This exercise highlights whether you’re operating with a surplus or a deficit each month, which can directly influence your ability to negotiate with creditors or qualify for legal remedies.

Prioritizing Your Debts

Focus on your secured debts, such as your mortgage or car loan, before addressing unsecured obligations like credit cards or medical bills. Homeowners often make the mistake of responding to aggressive collection calls from unsecured creditors while neglecting their mortgage, which increases the risk of foreclosure. Instead, consider negotiating lower monthly payments on credit card debt to free up funds for your mortgage. By prioritizing your most important debts, you create a solid foundation for an effective financial plan.

Building a Workable Budget

A practical budget is essential for managing debt. Loan servicers typically require a detailed financial worksheet that outlines your income and expenses to determine your eligibility for loss mitigation options. This budget will show whether your income can cover your current mortgage payments and any additional amounts needed for repayment plans.

Start by calculating your total monthly income from all sources, including wages, overtime, Social Security, rental income, child support, and alimony. Then, track every expense. Cut back on discretionary spending to free up funds for your mortgage. While these adjustments might seem small, they can quickly add up, potentially redirecting hundreds of dollars toward your mortgage each month.

If you find budgeting difficult, reach out to a HUD-approved housing counselor for free assistance. Remember, federal law requires mortgage servicers to contact borrowers within 36 days of a missed payment. By the time you’re 45 days delinquent, the servicer must assign someone to assist you with loss mitigation options. Take advantage of these resources – they’re designed to help you keep your home.

Methods to Reduce Debt and Strengthen Your Defense

Once you’ve assessed your finances and created a budget, the next step is to apply debt reduction strategies. These approaches not only help free up cash for your mortgage but also reinforce your ability to defend against foreclosure.

Snowball and Avalanche Payment Strategies

Two popular methods for tackling debt are the snowball and avalanche strategies. The snowball method focuses on paying off the smallest debts first, offering quick, visible progress. On the other hand, the avalanche method prioritizes debts with the highest interest rates, saving you more on interest over time.

"If you’re motivated by saving the most money while still paying off your debts, the highest interest rate method might be the right choice for you. However, if you’re motivated by seeing progress quickly, then you may want to consider the snowball method." – Consumer Financial Protection Bureau

If you’re dealing with high-interest credit card debt, the avalanche method can free up more money for your mortgage payments. Both methods are effective tools to allocate resources toward protecting your home.

Consolidating and Refinancing Your Debts

Refinancing your mortgage can lower your monthly payments by replacing your current loan with one that has a lower interest rate or a longer term. For example, as of February 2, 2026, 30-year fixed-rate mortgages average 5.99%, while 15-year terms are around 5.37%. Refinancing works best before you miss payments, as maintaining a good credit score and home equity is crucial. Once foreclosure proceedings begin or your credit takes a hit, traditional refinancing options become much harder to access.

For those already behind on payments, a loan modification can provide relief. This process consolidates overdue amounts, penalties, and fees into your principal balance. Programs like Fannie Mae or Freddie Mac‘s Flex Modification can reduce monthly mortgage payments by up to 20% for eligible borrowers. To see if your loan qualifies, use the lookup tools on the Fannie Mae or Freddie Mac websites.

Reducing your monthly payments through refinancing or modification not only alleviates financial pressure but also strengthens your ability to keep your home.

Working with Creditors to Adjust Terms

If refinancing or loan modifications aren’t enough, negotiating directly with creditors can provide additional options. Many unsecured creditors may agree to settle for 30% to 50% of the total debt if you’re able to offer a lump-sum payment.

"A bird in the hand is worth two in the bush. Creditors are usually more willing to take an offer of cash today rather than have to wait for multiple smaller payments over time." – Linda Thompson, Attorney

For your mortgage, ask your servicer about options like forbearance, repayment plans, or additional loan modifications. Forbearance can temporarily suspend payments for three to six months. A repayment plan allows you to gradually catch up on missed payments by spreading the overdue balance across your regular payments. If you have an FHA-insured loan, you might qualify for a partial claim – an interest-free loan from HUD that brings your mortgage current, with repayment deferred until the home is sold or the primary mortgage is paid off.

To streamline the process, prepare a hardship package that includes your financial statement, proof of income, and a brief explanation of your situation. By working with creditors to adjust terms, you can ensure more consistent mortgage payments – a critical step in defending against foreclosure.

sbb-itb-d613a70

Legal Options for Debt Management and Foreclosure Prevention

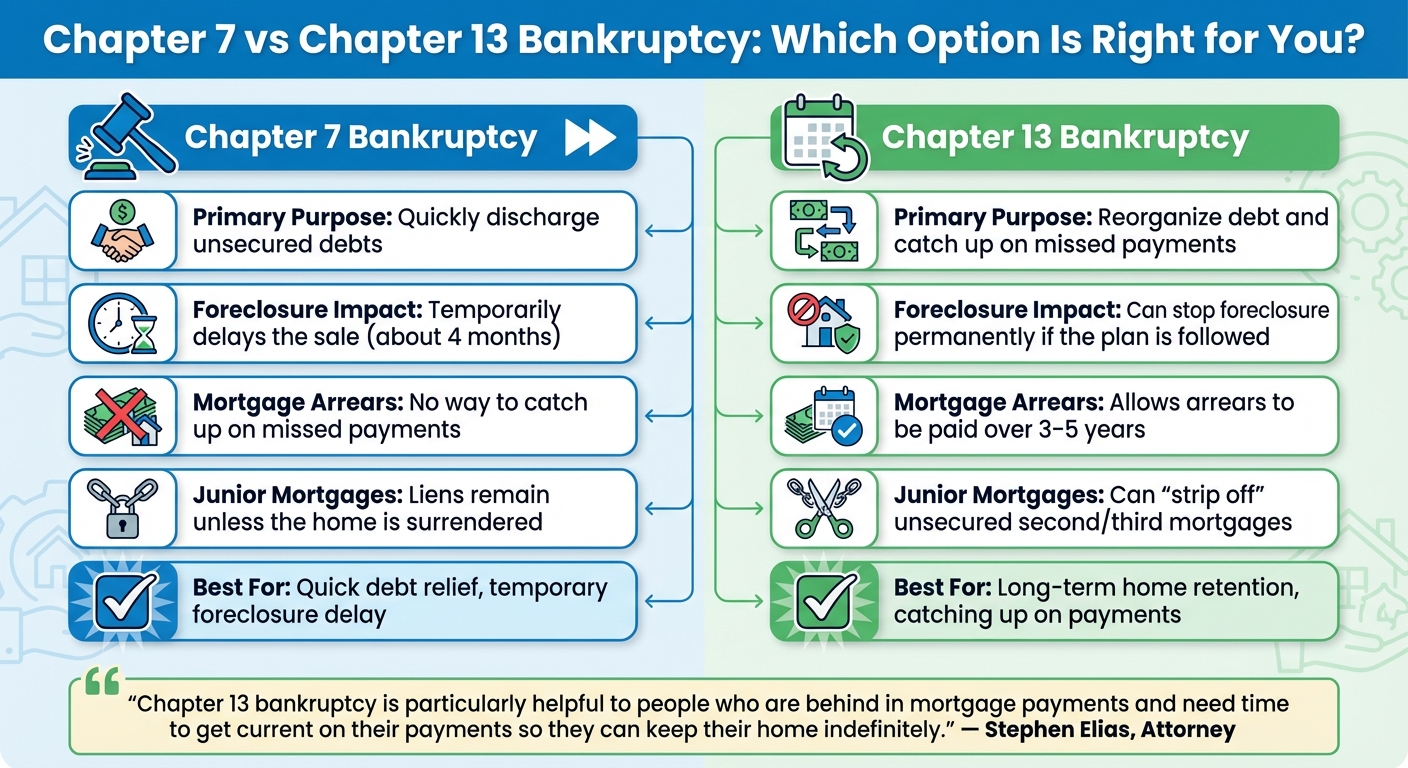

Chapter 7 vs Chapter 13 Bankruptcy for Foreclosure Defense Comparison

When working with creditors doesn’t resolve your financial challenges, legal options can provide a lifeline for managing debt and protecting your home. These solutions range from temporary protections to long-term restructuring, offering a way to stabilize your financial situation. Below, we’ll explore how bankruptcy and other legal remedies can complement your efforts to reduce debt and avoid foreclosure.

Bankruptcy is one of the most powerful legal tools available, as it activates an automatic stay under 11 U.S.C. § 362. This stay immediately halts foreclosure proceedings once you file. Depending on the type of bankruptcy, the outcomes can vary significantly:

- Chapter 7 bankruptcy provides temporary relief, delaying foreclosure for about four months while eliminating personal liability for deficiency judgments. However, it doesn’t offer a way to catch up on missed mortgage payments.

- Chapter 13 bankruptcy, on the other hand, lets you pay off overdue mortgage payments over three to five years while keeping your home. It also allows for the possibility of "stripping off" second or third mortgages if your home’s value is less than the balance of your first mortgage. This converts those junior mortgages into unsecured debt, which may be discharged.

"Chapter 13 bankruptcy is particularly helpful to people who are behind in mortgage payments and need time to get current on their payments so they can keep their home indefinitely." – Stephen Elias, Attorney

Here’s a quick comparison of the two bankruptcy options:

| Key Factor | Chapter 7 Bankruptcy | Chapter 13 Bankruptcy |

|---|---|---|

| Primary Purpose | Quickly discharge unsecured debts. | Reorganize debt and catch up on missed payments. |

| Foreclosure Impact | Temporarily delays the sale (about 4 months). | Can stop foreclosure permanently if the plan is followed. |

| Mortgage Arrears | No way to catch up on missed payments. | Allows arrears to be paid over 3–5 years. |

| Junior Mortgages | Liens remain unless the home is surrendered. | Can "strip off" unsecured second/third mortgages. |

If bankruptcy isn’t the right fit, loan modifications and forbearance agreements offer alternative paths. A forbearance agreement temporarily reduces or suspends your payments – usually for three to six months – helping you recover from short-term challenges like illness or job loss. Meanwhile, a loan modification restructures your mortgage more permanently. This might include lowering your interest rate, extending the loan term, or rolling missed payments into your principal balance. To maximize your options, ensure your application is submitted at least 37 days before any scheduled foreclosure sale to qualify for federal protections.

If keeping your home is no longer feasible, short sales and deed-in-lieu agreements provide alternatives to foreclosure. A short sale allows you to sell your property for less than you owe, with the lender’s approval. A deed in lieu, on the other hand, involves transferring ownership directly to the lender, bypassing the need to list and sell the property. Both options are most effective when you negotiate a written waiver of any deficiency – the difference between the sale price and your total debt. For FHA-insured loans, this can be especially helpful, as FHA guidelines prohibit lenders from pursuing deficiency judgments after these transactions.

"A ‘deed in lieu of foreclosure’ is a negotiated remedy between borrower and lender. The borrower transfers title to the property to the lender, and the lender cancels the foreclosure." – Amy Loftsgordon, Attorney

Getting Professional Legal Help

Advantages of Working with Legal Experts

Foreclosure defense can be a maze of legal intricacies, with rules that differ from one state to another. A seasoned attorney can spot defenses that might escape notice, such as errors in the chain of title, instances of robosigning on affidavits, or breaches of federal lending laws.

Lawyers bring more than just technical know-how – they wield negotiation skills and ensure critical deadlines are met. As Ben Hillard from The Castle Group puts it:

"The defense is to have the lender bear some responsibility".

When lenders realize they might face a prolonged legal battle, they often become more open to negotiating a loan modification or reaching a settlement. This is especially true if your home is "upside down" (worth less than the amount owed), which raises their financial risk. Federal law also provides key protections: servicers must wait 120 days after your first missed payment before initiating foreclosure. Additionally, submitting a complete loss mitigation application at least 37 days before a scheduled sale can halt dual tracking. With legal expertise, these protections can be leveraged effectively for timely negotiations and decisive action.

Services Offered by Foreclosure Defense Group

Foreclosure Defense Group uses these legal tools to help you manage foreclosure challenges. Their services go beyond debt reduction and negotiations, ensuring that no crucial deadlines are missed.

Their approach includes challenging a lender’s right to foreclose and thoroughly reviewing loan documents for procedural mistakes that could delay or stop the process. For those considering bankruptcy, they assist with filing Chapter 7 to temporarily pause foreclosure or Chapter 13 to create a structured repayment plan.

They also work to secure loan modifications, adjusting mortgage terms to make payments more manageable. For short-term financial struggles, they negotiate forbearance agreements to provide temporary relief. If keeping the property isn’t feasible, they help arrange short sales or deed-in-lieu agreements as alternatives. Plus, a free consultation gives you the opportunity to discuss your unique situation and explore tailored strategies without any upfront commitment.

Conclusion

Facing foreclosure can feel overwhelming, but it’s important to remember – you still have options. Acting quickly is key to protecting your home. Federal guidelines require lenders to reach out promptly and delay foreclosure proceedings, giving you a critical opportunity to take action.

As the New York State Unified Court System emphasizes:

"The earlier you work with the lender the better, since negotiating a workable deal becomes more and more difficult as time passes and arrears add up."

The longer arrears pile up, the harder it becomes to negotiate repayment plans, and missed payments can damage your credit, limiting refinancing opportunities. Federal protections require that loss mitigation applications be submitted at least 37 days before a foreclosure sale – so don’t wait to start the process.

By combining proactive strategies and legal options, you can build a stronger financial foundation. Whether it’s through debt reduction techniques like the snowball method, direct negotiations with creditors, or exploring legal solutions such as bankruptcy or loan modification, expert legal guidance can make all the difference. Research shows that homeowners who participate in foreclosure mediation are 1.7 times more likely to avoid foreclosure than those who go it alone.

If you’ve missed a payment, take action now. Contact a HUD-approved housing counselor for free assistance, or consult with experienced attorneys who specialize in your state’s foreclosure laws. Foreclosure Defense Group offers a free consultation to help you explore tailored strategies – no upfront commitment required.

FAQs

What’s the difference between Chapter 7 and Chapter 13 bankruptcy when defending against foreclosure?

Chapter 7 bankruptcy can offer a temporary break from foreclosure by wiping out unsecured debts. However, it doesn’t address overdue mortgage payments, which often results in losing the home.

On the other hand, Chapter 13 bankruptcy provides a way to catch up on missed mortgage payments through a structured repayment plan, typically lasting three to five years. This option can help homeowners avoid foreclosure and work towards regaining financial stability.

If foreclosure is a concern, understanding these bankruptcy options is essential. Seeking guidance from seasoned professionals, like the team at Foreclosure Defense Group, can make a significant difference in protecting your home.

Should I choose refinancing or a loan modification to manage my mortgage payments?

Deciding between refinancing and a loan modification comes down to your financial situation and what you hope to achieve.

Refinancing involves replacing your current mortgage with a new one. Homeowners often choose this route to lock in a lower interest rate, improve loan terms, or shorten the repayment period. This option works best for those with stable finances, strong credit, and enough home equity, especially if long-term savings are the goal.

A loan modification, however, adjusts the terms of your existing loan to make payments more manageable. This is often a lifeline for those facing financial difficulties, such as job loss or unexpected expenses. It’s especially helpful if you have limited equity or recent credit issues.

If you’re dealing with temporary financial hardship, a loan modification might provide the relief you need. But if you qualify for refinancing and want to lower your interest rate or change your loan term, refinancing could be the smarter choice. To make the right decision, consider consulting a financial or legal professional who can guide you based on your unique circumstances.

How can I effectively negotiate with creditors to manage my debt?

Negotiating with creditors can be an effective way to tackle debt and possibly steer clear of foreclosure. Here’s how to approach the process:

- Double-check the debt: Confirm that the debt details are accurate and ensure you’re dealing with the right creditor or collection agency.

- Evaluate your finances: Take a close look at your budget to figure out what you can realistically afford to pay before entering discussions.

- Present a proposal: Suggest a settlement amount or request more manageable payment terms. Be ready to handle counteroffers.

- Get it in writing: Always secure written documentation for any agreements or payment plans to avoid disputes or confusion later.

When negotiating, stay polite yet firm, and highlight your commitment to resolving the debt within your financial capabilities. Following these steps can help ease your debt load and reinforce your efforts to prevent foreclosure.

Related Blog Posts

- 7 Legal Rights Every Florida Homeowner Should Know

- How Attorneys Help Resolve Mortgage Disputes

- How Legal Help Improves Debt Settlements

- Foreclosure Defense: Preventing Costly Errors