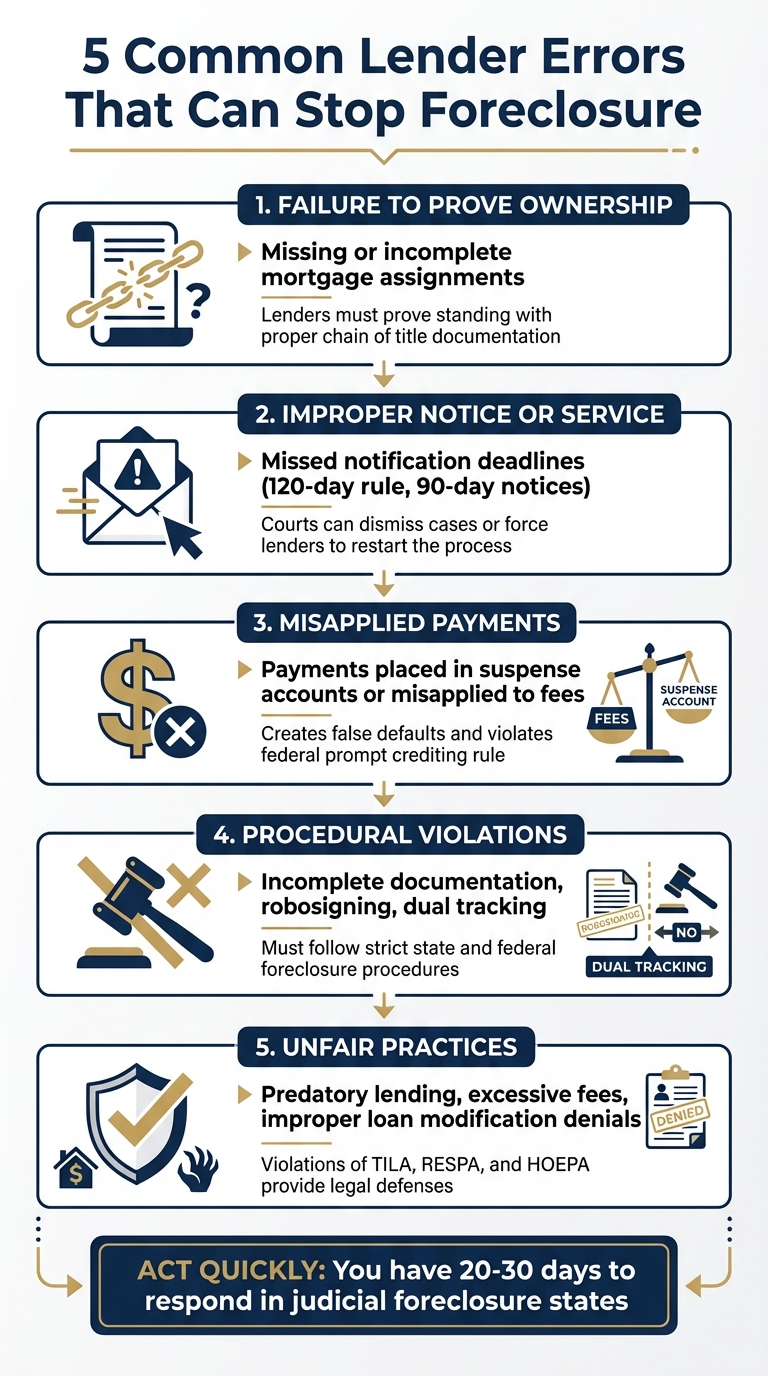

When lenders make mistakes during foreclosure, it can give homeowners opportunities to fight back. Courts take foreclosure cases seriously, and errors like missing documents, improper notices, or mishandled payments can delay or even stop the process. Here’s what you need to know:

- Proving Ownership: Lenders must show they own the mortgage before foreclosing. Missing or incomplete documents can invalidate their claim.

- Notification Errors: Borrowers must receive proper notices, like breach letters or foreclosure warnings, within specific timeframes. Mistakes here can force lenders to restart the process.

- Payment Mismanagement: Misapplied payments or unexplained fees can create false defaults. Federal laws protect against these errors.

- Procedural Violations: Lenders must follow strict state and federal foreclosure rules. Skipping steps or filing incomplete paperwork can weaken their case.

- Unfair Practices: Predatory lending or improper denial of loan modifications can provide additional defenses for homeowners.

If you suspect errors, act quickly. Review all documents, request clarifications, and consider seeking legal help to challenge the foreclosure process.

5 Common Lender Errors That Can Stop Foreclosure

What Are Common Issues In A Foreclosure Case? – CountyOffice.org

sbb-itb-d613a70

Failure to Prove Mortgage Ownership

Before a lender can legally foreclose on your home, they must demonstrate that they own your mortgage. This concept, known as "standing," is a cornerstone of foreclosure law. As attorney Amy Loftsgordon from the University of Denver Sturm College of Law explains:

"The promissory note owner is the only party with the legal right (called ‘standing’) to collect payment on the debt."

The issue arises when lenders struggle to provide the necessary documentation. Mortgages are often sold or transferred multiple times, and with each transfer, the new owner should receive two key documents: the promissory note (your agreement to repay) and the mortgage or deed of trust (the security instrument). The note must be "endorsed" (signed over), and the mortgage must be "assigned" to the new holder. If these transfers weren’t properly documented, the lender may lack the legal authority to foreclose.

Chain-of-Title Problems

A complete and accurate chain of title is critical for a valid foreclosure. The chain of title is essentially the historical record of ownership transfers, tracing the mortgage from the original lender to the current holder. Victoria Araj from Rocket Mortgage explains:

"A chain of title should always reflect continuous, unbroken ownership."

Breaks or errors in this chain can make a lender’s foreclosure claim vulnerable. For example, in Robert McLean v. Chase Bank, Chase attempted to foreclose using a mortgage assignment from MERS (Mortgage Electronic Registration System) that was dated three days after filing the foreclosure complaint. The Florida Fourth District Court of Appeal overturned the foreclosure judgment, ruling that Chase failed to prove it had standing when the lawsuit was filed.

Timing plays a crucial role, as Maxwell Swinney, a foreclosure defense specialist, highlights:

"Standing is very important, and the plaintiff must have it at the time they file a foreclosure action against you."

In many states, lenders cannot correct a lack of standing once the foreclosure process has started. You can review the chain of title yourself by checking local land records to confirm whether mortgage assignments were recorded before the foreclosure began. Some states, such as Wyoming and Michigan, require a valid chain of recorded assignments as a prerequisite for initiating a nonjudicial foreclosure.

Missing or Incomplete Documents

Another critical issue is the lender’s ability to produce complete and accurate documentation. The original promissory note is particularly important. If a lender cannot provide it, they face a higher burden of proof. For instance, Florida law has required since July 1, 2013, that a foreclosing bank file a certification confirming possession of the original note at the time the foreclosure complaint is filed.

The 2010 mortgage crisis exposed widespread document issues, including the "robosigning" scandal, where affidavits were signed in mere seconds without verifying mortgage details. This scandal led to the 2012 National Mortgage Settlement, in which major banks like Wells Fargo and JPMorgan Chase paid $26 billion to settle claims involving fabricated foreclosure evidence.

If you suspect missing documentation, you can formally request information from your loan servicer to identify the current loan owner and check for gaps in the chain of title. Additionally, scrutinize affidavits of indebtedness – if the signer lacks firsthand knowledge of your loan’s history, the affidavit may be challenged. Federal laws like the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA) also require lenders to notify you of mortgage transfers. TILA mandates notification within 30 days of a transfer, while RESPA requires notice at least 15 days before a servicing transfer takes effect.

Improper Notice or Service of Default

Lenders are legally required to notify borrowers before initiating foreclosure. This notice gives homeowners a chance to address the default or explore other options. When lenders fail to follow these notification rules, courts can dismiss foreclosure cases or force the lender to restart the process. Just as incomplete paperwork can weaken a lender’s case, improper notice can further undermine their position. Let’s dive into specific notification missteps that can invalidate a foreclosure.

Failure to Meet State Notification Deadlines

Federal law includes a 120-day rule, which generally prohibits servicers from starting foreclosure proceedings until a borrower is more than 120 days behind on payments. Additionally, lenders must send a breach letter that outlines the default, explains how to fix it, provides a deadline (typically at least 30 days), and warns of potential acceleration. Attorney Amy Loftsgordon highlights the importance of this step:

"If the lender or servicer neglects to send the breach letter and you raise this issue with the court, the court might order the lender to start the foreclosure over."

State laws add further requirements. For example, California mandates personal contact with the borrower at least 30 days before filing a Notice of Default, while New York requires a written notice 90 days before any legal action. Federal law also obligates servicers to contact borrowers by phone within 36 days of a missed payment and to send written information about loss mitigation options within 45 days.

In the case of Citimortgage v. Dente, a New York appellate court invalidated a foreclosure because the lender included unnecessary bankruptcy details in the 90-day notice. Under New York’s RPAPL § 1304, including unrelated information in the same envelope as the required notice violates the law.

Improper Delivery of Notices

How notices are delivered is just as important as when they are sent. Even if deadlines are met, using incorrect delivery methods can jeopardize the foreclosure process. Many states require notices to be sent via certified or registered mail, with return receipt requested. Federal law also requires notices to be sent at least 21 days before the foreclosure sale and delivered in this manner. Additionally, lenders are often required to publish a notice of sale in a local newspaper for three consecutive weeks.

To determine if your lender followed proper procedures, consider these steps:

- Check the mailing: In New York, including unrelated information in the same envelope as the 90-day notice violates RPAPL § 1304.

- Request diligence records: In California, if a lender cannot reach you, they must document efforts such as sending a first-class letter, making three phone call attempts at different times, and following up with a certified letter two weeks later.

Federal law considers notice properly delivered once it’s mailed to the recorded owner’s address at least 45 days before the sale. If the lender sent notices to an outdated address despite being informed of your updated contact information, this could be grounds for improper service.

Misapplied or Misappropriated Payments

Getting payments applied correctly is just as crucial to foreclosure defense as having proper documentation. When payments are mishandled, it can create false defaults. For instance, some servicers mistakenly place full payments into "suspense accounts" instead of applying them to your principal and interest. Others might improperly use your funds to cover fees before reducing your mortgage balance, which can violate both your mortgage contract and federal law.

Attorney Amy Loftsgordon highlights an important legal safeguard:

"Under federal mortgage servicing laws, the servicer must credit your payment to the account on the day it receives the payment. This requirement is called the ‘prompt crediting rule.’"

If a servicer delays crediting your payment beyond the day it’s received, they can only do so if the delay doesn’t lead to late fees or negative credit reporting. For payments that don’t follow specific written instructions, servicers have up to five days to process them. Now, let’s look at how escrow accounts and unexplained fees can cause further complications.

Escrow Payment Mismanagement

Errors in escrow account management can seriously affect your mortgage. Servicers are required to use escrow funds to pay property taxes and insurance premiums on time. When they fail to do so, it can lead to tax liens or canceled insurance policies – even if you’ve been making all your monthly payments. According to the Consumer Financial Protection Bureau (CFPB):

"Examiners found that, in some cases, mortgage servicers overcharged borrowers for services or added fees outside of their loan terms."

Another common issue is force-placed insurance. If your servicer believes you don’t have insurance, they might charge you for expensive "lender-placed" insurance – even if your current coverage is active and valid. To avoid this, review your annual escrow account statements closely. Confirm that taxes and insurance are being paid correctly and that the escrow "cushion" isn’t inflated beyond legal limits.

Unexplained Late Fees or Charges

Late fee pyramiding is a sneaky practice that can snowball into bigger problems. Justia explains it like this:

"Pyramiding happens when a lender uses part of the payment to cover the late fees. This means that the payment does not count as a full payment, and the lender then assesses additional late fees."

Under the Real Estate Settlement Procedures Act (RESPA), you have the right to send a formal "Notice of Error" to your servicer’s designated address. The servicer typically has 30 business days to either fix the issue or explain why they believe no error occurred. During the 60 days following your notice, they are prohibited from reporting negative information about the disputed payment to credit bureaus.

You can also send a "Request for Information" to get a detailed payment history that shows exactly how your funds were applied. The CFPB emphasizes:

"A servicer shall not charge a fee, or require a borrower to make any payment that may be owed on a borrower’s account, as a condition of responding to a notice of error."

It’s important to keep copies of all correspondence, including dates and the names of anyone you speak with. If the issue remains unresolved, consider filing a complaint with the CFPB and consulting a foreclosure defense attorney for further assistance.

Procedural Violations in Foreclosure Filing

When borrowers fall behind on payments, lenders are still required to follow strict legal procedures outlined by state foreclosure laws. If they fail to comply, courts can dismiss the case or force the lender to start over. Attorney Amy Loftsgordon explains the importance of these rules:

"Major violations of the law, like if the lender failed to send you a notice of default as required by state law or a breach letter as required by the deed of trust, will probably cause the lender to have to start the foreclosure over."

Since the 2008 financial crisis, courts have become more cautious about approving foreclosure actions without proper scrutiny, making adherence to these procedures more critical than ever. Knowing these rules can help you determine if your lender has overstepped. Next, let’s look at how incomplete filings can weaken a lender’s case.

Failure to File Complete Documentation

In judicial foreclosures, lenders must file a lawsuit and back it up with accurate documentation. One of the most glaring violations involves robosigning, where bank employees sign affidavits of indebtedness without actually reviewing the files or verifying the debt amounts .

Attorney Amy Loftsgordon explains why these affidavits are critical:

"The idea behind the affidavit requirement is to prevent foreclosures on homes when the foreclosing bank can’t prove that it owns the mortgage or when the homeowner isn’t in default to the degree asserted in the foreclosure papers."

If you’re dealing with judicial foreclosure, carefully review the affidavit of indebtedness for errors in the principal balance, interest rates, or late fees. Also, ensure that the summons and complaint were properly served. Incorrect figures can lead to an unfair judgment, and improper service is a valid defense that could get the case dismissed . Beyond documentation, lenders must also comply with specific state foreclosure laws.

Non-Compliance with Local Foreclosure Laws

In addition to filing the right paperwork, lenders must meet the requirements of state-specific foreclosure laws. Missing even one pre-foreclosure step can derail their case. For instance, in New York, lenders must send a 90-day pre-foreclosure notice that includes a list of five housing counseling agencies . They’re also required to provide a "Help for Homeowners in Foreclosure" notice printed in bold, large type on colored paper. Failing to meet these exact requirements can serve as a procedural defense.

California has its own set of strict rules. Starting January 1, 2025, trustees cannot sell residential properties for less than 67% of their fair market value during the initial foreclosure sale. If no bid meets this threshold, the sale must be delayed by at least seven days. Additionally, lenders in California must contact homeowners at least 30 days before recording a notice of default .

Federal law provides further safeguards. For example, servicers cannot initiate foreclosure proceedings until a borrower is more than 120 days behind on payments . They are also prohibited from dual tracking, which means moving forward with a foreclosure sale while a loss mitigation application is still under review . If you’ve submitted a loan modification application at least 37 days before a scheduled sale, the servicer must complete its review before proceeding .

To uncover possible violations, you can submit a formal Request for Information under RESPA to obtain copies of your promissory note, deed of trust, and payment history . Check local land records to confirm that notices were recorded and mailed within the required timeframes. In nonjudicial foreclosure states, you may need to file your own lawsuit to bring these violations to the court’s attention . Seeking advice from a foreclosure defense attorney, such as those at Foreclosure Defense Group, can help you identify any state-specific rules your lender may have overlooked.

Unfair Lending and Servicing Practices

Errors in documentation can weaken foreclosure claims, but predatory practices go a step further, tipping the legal scales in favor of homeowners. Beyond procedural missteps, unethical lending behaviors give homeowners additional grounds to fight foreclosures.

Predatory lending tactics – like loan flipping or steering borrowers into expensive subprime loans – can create opportunities to challenge a foreclosure under laws like the Truth in Lending Act (TILA) and the Home Ownership and Equity Protection Act (HOEPA). According to the Office of the Comptroller of the Currency, predatory lending involves "the aggressive marketing of credit to prospective borrowers who simply cannot afford the credit on the terms being offered". Under TILA, lenders are required to provide accurate information on annual percentage rates (APR), finance charges, and payment schedules. Even minor errors, such as a $35 discrepancy, can result in statutory damages ranging from $400 to $4,000.

HOEPA, on the other hand, enforces strict rules for high-cost loans. For example, it limits late fees to 4% of the overdue amount and generally bans balloon payments. Violating these rules might allow borrowers to rescind the loan entirely, though this remedy typically applies to non-purchase loans like refinances or home equity lines of credit. As Attorney Amy Loftsgordon notes:

"Rescinding the mortgage will stop a foreclosure, but this tactic usually only works if you can arrange a refinance to return the remaining loan principal to the lender".

Excessive Fees or Charges

Some loan servicers may tack on unauthorized fees – like inflated inspection costs, excessive late fees, or force-placed insurance – that increase your loan balance and make it harder to reinstate your mortgage. Attorney Amy Loftsgordon explains:

"An overstated amount might prevent you from keeping your home. For example, if the mortgage holder says you owe $4,500 to reinstate… when in fact you owe only $3,000, you may not have been able to take advantage of reinstatement".

To dispute these fees, you can send a written Notice of Error (NOE) to your loan servicer under the Real Estate Settlement Procedures Act (RESPA). The servicer is required to acknowledge your letter within five business days and must correct the issue or provide an explanation within 30 business days. Additionally, you can submit a Request for Information (RFI) to review account ledgers and confirm that your payments were applied correctly. Keep an eye on your monthly statements for unexplained suspense accounts – where servicers hold partial payments instead of applying them to your balance. This practice can lead to wrongful late fees and other complications. Resolving these disputes quickly is crucial to maintaining control over your loan and avoiding foreclosure.

Improper Denial of Loan Modifications

Federal law prohibits "dual tracking", meaning that if you’ve submitted a loan modification application at least 37 days before a scheduled foreclosure sale, the servicer must complete the review process before moving forward with the sale. However, servicers sometimes deny modifications improperly or fail to respond within the required timeframes. If this happens, you can raise the denial as a defense in court (in states with judicial foreclosure processes) or file a lawsuit in states with nonjudicial foreclosures.

"With the CFPB essentially shut down, the proposed rule has been scuttled… homeowners and borrowers will have to more heavily rely on legal representation to defend their rights and challenge wrongful foreclosures".

If you suspect unfair practices, consulting foreclosure defense experts – like those at Foreclosure Defense Group – can help you assess whether these issues can delay or halt a foreclosure.

How Homeowners Can Challenge Lender Errors

If you’ve identified errors made by your lender, there are specific steps you can take to dispute them effectively. Here’s how to proceed.

Document Review and Dispute Process

Start by carefully reviewing your mortgage statements. Look for issues like unexplained fees, payments that were misapplied, or charges that seem incorrect. If anything seems off – such as discrepancies in your account balance or payment history – send a Request for Information (RFI). This formal request should ask for key documents like the promissory note, mortgage assignments, and a detailed payment ledger.

Once you’ve pinpointed a specific error, such as a misapplied payment or an incorrect payoff amount, follow up with a written Notice of Error (NOE). Send this to the address listed on your mortgage statement. Be sure to include your name, account number, and a clear description of the error. According to the Real Estate Settlement Procedures Act (RESPA), your servicer must acknowledge the letter within five business days. They then have 30 business days to either correct the issue or explain why they believe no error occurred. During this review period, they cannot charge fees or report missed payments related to the dispute.

If you’re facing an imminent foreclosure sale, timing becomes even more critical. In states with judicial foreclosure processes, you must file an "Answer" within 20–30 days to avoid a default judgment. In nonjudicial foreclosure states, you may need to take the initiative by filing a lawsuit and requesting a Temporary Restraining Order (TRO) to halt the sale while your dispute is being resolved. Attorney Amy Loftsgordon emphasizes the importance of acting quickly:

"Generally, if you don’t point out errors or omissions in the paperwork or procedures, the court will accept them as sufficient evidence, award the lender a default judgment, and order a foreclosure sale".

For more complex issues, professional legal help is often necessary.

Consulting Foreclosure Defense Professionals

While straightforward errors can often be resolved through dispute letters, more complicated problems – like chain-of-title issues, robosigned documents, or dual tracking violations – require legal assistance. Attorneys specializing in foreclosure defense can uncover hidden mistakes by using tools like the discovery process to request internal lender records, original promissory notes, and other critical documents. This is especially important in nonjudicial foreclosure states, where homeowners bear the burden of proof. In these cases, legal experts can draft lawsuits and file emergency motions to stop a sale.

With limited federal oversight in the foreclosure process, having a skilled attorney can make all the difference when challenging wrongful actions by lenders. For example, firms like Foreclosure Defense Group specialize in identifying lender errors, navigating complex procedures, and protecting homeowners’ rights. A free consultation with such professionals can help you determine whether the mistakes in your case are enough to delay or even stop the foreclosure process entirely.

Conclusion

Examining common lender mistakes – like document errors, misapplied payments, and procedural missteps – highlights practical ways to challenge a foreclosure. These errors can create opportunities to contest the process or negotiate better terms.

Acting quickly is essential. In judicial foreclosure states, homeowners usually have just 20–30 days to respond before risking a default judgment. In nonjudicial states, you might need to file your own lawsuit and request emergency relief to pause the sale. The further the process advances, the harder it becomes to stop. Attorney Geoff Walsh emphasizes:

"The deeper you get into the foreclosure process, the harder it will be to stop it".

This urgency makes a prompt legal review crucial. With the Consumer Financial Protection Bureau (CFPB) described as "essentially nonfunctional" by 2025, homeowners must rely on experienced attorneys to safeguard their rights. These legal professionals can identify lender errors, enforce protections under RESPA and TILA, and even compel lenders to restart the foreclosure process when they violate legal requirements.

FAQs

What can I do if my lender cannot prove they own my mortgage?

If your lender cannot prove they own your mortgage, you might have grounds to challenge the foreclosure in court. Lenders are required to show they have the legal standing to foreclose on your property.

By disputing their ownership claim, you could potentially get the foreclosure case dismissed. To fully understand this option and safeguard your rights as a homeowner, it’s crucial to consult with an experienced legal professional.

How can I spot and challenge errors in foreclosure notices?

Carefully reviewing foreclosure notices is crucial to ensure that all legal procedures have been followed. Some common mistakes that may appear include:

- Failure to provide proper notice: The lender might not have notified you in the way required by law.

- Standing issues: The lender must prove they have the legal right to foreclose.

- Missing documentation: Key documents, like the promissory note, may be absent.

These errors can provide a basis for disputing the foreclosure.

Procedural errors are another area to examine. For instance, if the lender improperly served documents or violated specific state laws, you might have grounds to challenge the notice. Additionally, homeowners can raise legal defenses based on violations of federal regulations, such as the Real Estate Settlement Procedures Act (RESPA).

To navigate these challenges effectively, consulting with a legal professional who specializes in foreclosure defense is highly recommended. They can help you identify potential errors and build a case to safeguard your rights.

What can I do if my loan modification application was unfairly denied?

If your loan modification application was denied unfairly, you might have the option to challenge the decision through legal action. Start by examining whether your lender or mortgage servicer adhered to all necessary procedures and complied with both federal and state laws. Common issues include mishandling your application, errors during the review process, or violations of loss mitigation regulations.

You can dispute the denial by filing a notice of error or a formal complaint under federal laws like the Real Estate Settlement Procedures Act (RESPA). Doing so may temporarily delay or even pause foreclosure proceedings while your case is reviewed. If the problem remains unresolved, consulting a legal expert in foreclosure defense can help you identify your next steps. Options may include requesting a reassessment of your application or filing a lawsuit to safeguard your rights.

For personalized help, consider reaching out to a legal team like Foreclosure Defense Group, which focuses on assisting homeowners in navigating foreclosure issues and protecting their rights.

Related Blog Posts

- How Attorneys Help Resolve Mortgage Disputes

- Wrongful Foreclosure: Key Legal Rights Explained

- Emergency Motion to Halt Foreclosure Sale

- Top Legal Cases on Loan Modification Breaches