Florida Statutes § 702.015 sets strict requirements for foreclosure complaints in Florida, ensuring plaintiffs prove their legal right to enforce a mortgage. Here’s what you need to know:

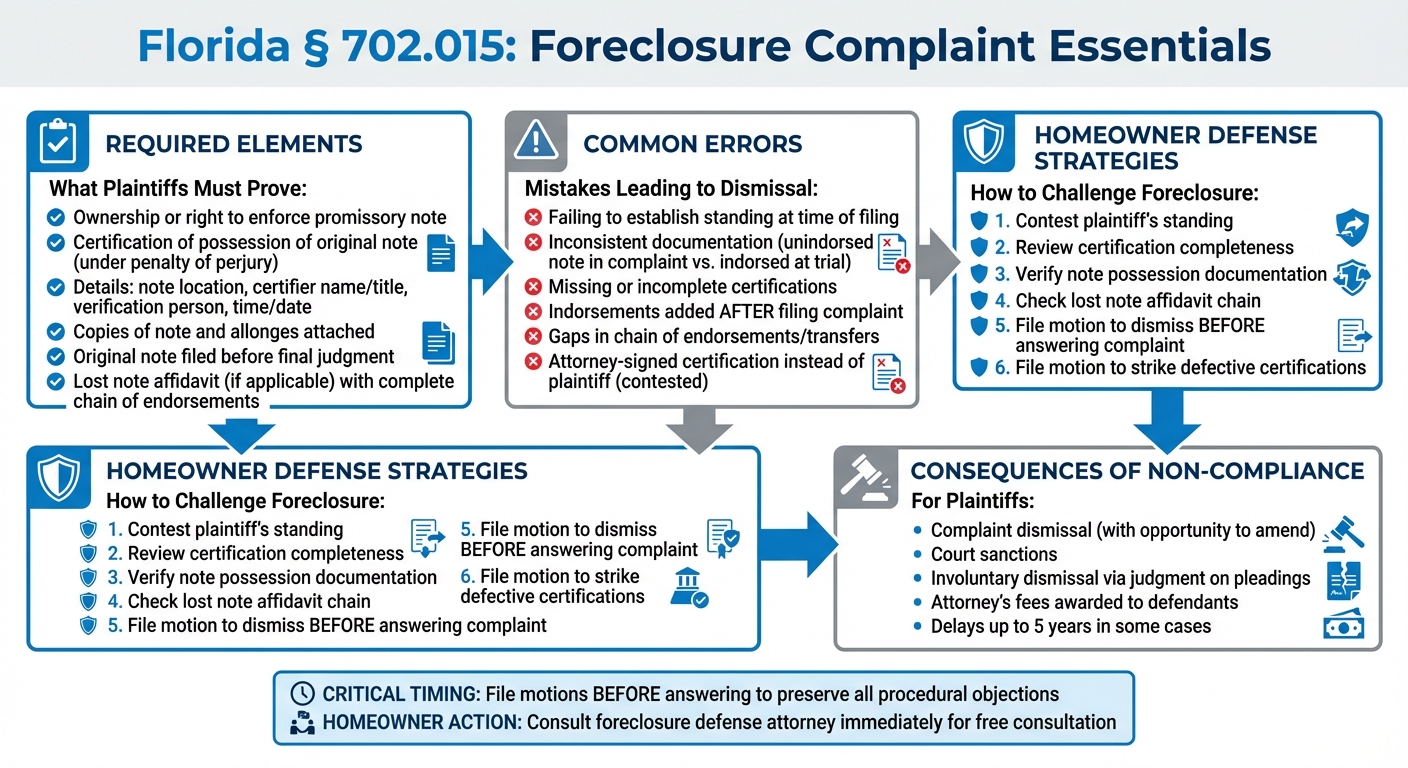

- Key Requirements: Plaintiffs must show ownership or the right to enforce the promissory note, certify possession of the original note, and follow specific procedures if the note is lost.

- Common Errors: Mistakes like failing to establish standing at the time of filing, inconsistent documentation, or incomplete certifications often lead to case dismissals.

- Defendant Protections: Homeowners can challenge foreclosure complaints by identifying gaps in standing, documentation, or compliance with legal standards.

- Legal Consequences: Non-compliance can result in dismissals, delays, or sanctions against plaintiffs.

Understanding these rules is critical for homeowners facing foreclosure. Acting early and consulting legal experts can help protect your rights and potentially halt foreclosure proceedings.

Florida Foreclosure Complaint Requirements Under § 702.015

Answering the foreclosure complaint is essential

sbb-itb-d613a70

Required Elements in Foreclosure Complaints Under § 702.015

Foreclosure complaints need to include specific details to establish the plaintiff’s legal right to enforce the mortgage.

Allegations of Note Ownership or Right to Enforce

The plaintiff must clearly outline their connection to the promissory note, demonstrating either possession of the note or the legal right to enforce it under § 673.3091. It’s not enough to simply claim ownership; the complaint must include detailed evidence of how the note was acquired and the plaintiff’s standing. Courts carefully review these allegations, as many foreclosure defenses focus on whether the plaintiff can prove their right to enforce the note from the very start of the case.

Original Note Certification Requirements

According to § 702.015(3), the plaintiff must certify possession of the original promissory note. This certification should detail the note’s current location and include copies of the note and any related allonges. While these copies can initially be submitted, the original note must be filed with the court clerk before the final judgment. This process is designed to prevent multiple parties from attempting to foreclose on the same property with duplicate documents. If the original note is unavailable, strict procedures must be followed to confirm its loss.

Procedures for Lost Notes

If the original note has been lost, destroyed, or stolen, the plaintiff must provide an affidavit under penalty of perjury that explains the entire chain of endorsements, transfers, or assignments. As vLex United States explains:

To enforce a lost or destroyed promissory note, the plaintiff must show that it was entitled to enforce the note at the time that the note was lost, or that it directly or indirectly acquired ownership of the note from someone who was entitled to enforce the note when the note was lost.

The affidavit must include supporting documents, such as audit reports confirming receipt of the original note or other evidence of its acquisition and ownership. Additionally, before the final judgment, the plaintiff must offer sufficient protection to the borrower to guard against potential claims from other parties who might later try to enforce the same note.

Frequent Errors in Foreclosure Complaints

Filing a foreclosure complaint under § 702.015 requires precision, yet many plaintiffs stumble over key requirements. These mistakes can derail cases, often because plaintiffs fail to establish standing at the outset. Courts have made it clear: standing must exist when the lawsuit is filed – it cannot be fixed later. As highlighted in Rigby v. Wells Fargo Bank, N.A.:

A plaintiff in a foreclosure "must have standing to file suit at its inception and may not remedy this defect by subsequently obtaining standing."

Another common issue is inconsistent documentation. For example, plaintiffs might attach an unindorsed note to the initial complaint but later present an indorsed version at trial. This discrepancy undermines their case. A notable example is Seidler v. Wells Fargo Bank, N.A., where the Florida First District Court of Appeal reversed a foreclosure judgment. Wachovia Bank filed a complaint in 2008 with an unindorsed note, but Wells Fargo, as the successor, presented a blank-indorsed note at trial. The court found no evidence that the original plaintiff had possession of the indorsed note when the suit began, ruling the evidence insufficient.

Timing also plays a critical role. Plaintiffs must demonstrate that any indorsements – whether blank or special – were added to the note before filing the complaint. In Kiefert v. Nationstar Mortgage, LLC, the court emphasized:

The plaintiff must establish that the note was indorsed before the filing of the complaint in order to prove its standing as a holder.

Errors related to mergers or transfers of ownership further complicate matters. If the plaintiff is substituted during the case, they must prove the original filer had standing at the time the complaint was submitted. These missteps often lead courts to scrutinize foreclosure complaints closely.

How Courts Review Compliance with § 702.015

Courts take a detailed approach when reviewing foreclosure complaints, especially when defendants challenge the plaintiff’s standing. Once standing is disputed, the burden shifts to the plaintiff to prove their right to enforce the note. The court in Ham v. Nationstar Mortg., LLC explained:

Once a defendant contests the plaintiff’s standing as the proper party to enforce a note via foreclosure, the plaintiff’s right to bring suit on the note at the requisite time becomes a disputed issue the plaintiff must prove.

Judges examine several factors to ensure compliance with § 702.015, including:

- Whether the complaint includes certifications made under penalty of perjury.

- If the attached note aligns with the original documentation.

- Whether lost note affidavits meet the evidentiary standards of § 673.3091.

- If the chain of endorsements and transfers establishes the plaintiff’s authority to enforce the note.

If the documentation is incomplete, inconsistent, or fails to prove standing at the time of filing, courts often grant motions that challenge the complaint’s validity.

Consequences of Non-Compliance

Failing to meet the requirements of § 702.015 can lead to serious repercussions for plaintiffs. The most immediate consequence is dismissal of the complaint, though courts often allow plaintiffs to amend and correct errors. Defendants can also file motions to strike pleadings if certifications or affidavits are missing or defective.

In some cases, courts impose sanctions against plaintiffs who fail to comply with statutory mandates. If defendants file motions for judgment on the pleadings due to standing violations, the case could face involuntary dismissal. Additionally, when defendants are represented by attorneys, courts may award attorney’s fees for motions addressing the plaintiff’s non-compliance.

Timing is especially critical for homeowners. Jacqueline Alicia Salcines, a Real Estate Attorney, warns:

If you do nothing and go to trial the judge may ignore it. Consult an attorney immediately to preserve your rights.

Defendants must act early to protect their rights. Filing an answer without first challenging deficiencies in the complaint can waive procedural objections. To avoid this, defendants should file motions to strike or dismiss before responding to the complaint. This ensures all procedural challenges are preserved.

Using § 702.015 in Foreclosure Defense

Homeowners can use § 702.015 to challenge foreclosure complaints that fail to meet legal requirements. By focusing on the statute’s specific demands and common mistakes made by plaintiffs, homeowners and their attorneys can identify weaknesses in the case early on. This law establishes clear guidelines that plaintiffs must follow, and any failure to do so can provide an opening for a strong defense.

The legislative intent behind § 702.015 is clear:

"The Legislature intends that this section expedite the foreclosure process by ensuring initial disclosure of a plaintiff’s status and the facts supporting that status, thereby ensuring the availability of documents necessary to the prosecution of the case."

This means plaintiffs must provide complete and accurate documentation from the start. If they fail to do so, homeowners can use this to their advantage, holding plaintiffs accountable for any gaps or errors.

Contesting Standing and Note Possession

One of the most effective ways to challenge a foreclosure case under § 702.015 is by questioning the plaintiff’s standing. The statute requires plaintiffs to explicitly state their status as the holder of the original note or explain their legal right to enforce it under § 673.3011. Defense attorneys can carefully review whether these claims are detailed and backed by proper documentation.

The certification of possession requirement is another area ripe for scrutiny. Plaintiffs must certify, under penalty of perjury, specific details such as the note’s location, the certifier’s name and title, the person verifying possession, and the exact time and date of verification. Missing any of these elements can render the complaint invalid.

Past cases highlight how these technicalities can impact foreclosure lawsuits. For example:

- Bank of Am., N.A. v. Leonard (2016): A trial court dismissed a foreclosure case because the certification required by § 702.015 was signed by the plaintiff’s attorney instead of the plaintiff. While the Florida 1st District Court of Appeal later ruled that an attorney’s certification was sufficient, this case demonstrates how defense attorneys can leverage such deficiencies at the trial level.

- RBS Citizens N.A. v. Reynolds (2017): A trial court dismissed a complaint because the plaintiff’s certification wasn’t notarized. The 2nd District Court of Appeal clarified that notarization isn’t required, only a declaration under penalty of perjury. This underscores the importance of strict compliance with the statute.

Defense attorneys should also confirm that certifications include all necessary elements, such as allonges, to establish the plaintiff’s holder status. If the plaintiff is a loan servicer rather than the note holder, defendants can demand proof of authority, such as a Power of Attorney or Servicing Agreement.

For cases involving lost notes, plaintiffs must provide an affidavit showing an unbroken chain of endorsements. Any gaps in the chain can undermine their right to enforce the note. Defense attorneys should scrutinize these affidavits carefully to ensure they meet the legal requirements.

The timing of standing is also critical. As the court stated in Wells Fargo Bank v. Diz:

"Standing to foreclose must be demonstrated with competent, substantial evidence at the time of filing the lawsuit."

This means plaintiffs cannot fix standing issues after filing, making it essential to identify these problems early.

Filing Motions to Dismiss for Statutory Violations

After identifying standing or documentation issues, the next step is filing motions to address these deficiencies. If a foreclosure complaint doesn’t meet § 702.015’s requirements, defendants should file a motion to dismiss before responding to the complaint. This motion should clearly outline the specific violations, such as missing certifications or incomplete allegations about standing.

Defendants can also file motions to strike defective or incomplete certifications and affidavits. Under § 702.015, courts can impose sanctions on plaintiffs who fail to meet the statute’s pleading and certification standards. In some cases, this can lead to dismissal of the complaint, although courts may allow plaintiffs to amend their filings.

Florida foreclosure cases operate under equitable principles outlined in § 702.01, giving courts broad discretion. Additionally, § 702.07 allows courts to set aside foreclosure decrees before a sale occurs. This means homeowners may still have opportunities to challenge compliance with § 702.015 even after the case has advanced.

When filing motions, attorneys must cite specific violations of § 702.015. For example, if a certification is missing the time and date of verification, the motion should reference this omission and explain its significance. Similarly, if the plaintiff fails to provide documentation proving delegated authority, this should also be clearly outlined.

Foreclosure Defense Group offers legal representation to homeowners facing foreclosure. Their attorneys specialize in identifying statutory violations and crafting defense strategies based on § 702.015. Homeowners can schedule a free consultation to explore whether their case has grounds for dismissal or other defenses under Florida law. These targeted motions, grounded in § 702.015’s requirements, are a key part of the broader defense strategy outlined in this guide.

Conclusion

Florida Statutes § 702.015 provides important protections for homeowners facing foreclosure by requiring plaintiffs to demonstrate their legal authority to enforce a mortgage from the very beginning. This ensures that only those with proper standing can pursue foreclosure, reducing the risk of wrongful claims.

Strict enforcement of § 702.015 can sometimes result in significant delays – up to 5 years in some cases – while disputes over statutory violations are resolved. These delays can place financial pressure on lenders, often leading them to offer reduced principal balances or lower interest rates to reach settlements that homeowners can better manage.

For homeowners, these protections highlight the need for immediate and proactive steps. Responding promptly to a foreclosure complaint is essential. Filing a formal answer not only asserts defenses but also compels the lender to prove compliance with legal requirements. Keeping detailed records of all interactions, payments, and notices from lenders or servicers can further bolster a defense against any statutory shortcomings in the foreclosure process.

Seeking legal guidance is another key move. An experienced attorney can evaluate the case, identify potential violations of § 702.015, negotiate on behalf of the homeowner, and provide representation in court. Firms like Foreclosure Defense Group offer free consultations to help homeowners explore their legal options and determine if their case could be dismissed due to non-compliance with statutory requirements.

Without proper legal assistance, homeowners face the risk of losing their property to parties that may not have the legal authority to enforce the debt. However, by understanding and utilizing the safeguards of § 702.015, homeowners can turn a challenging situation into an opportunity to build a strong defense and explore alternative solutions.

FAQs

What does “standing at inception” mean in a Florida foreclosure?

In Florida foreclosure cases, "standing at inception" means the plaintiff must demonstrate they had the legal authority to initiate the foreclosure at the time the complaint was filed. This involves proving they held a valid interest in the mortgage or note at the start of the case, as required by Florida Statutes § 702.015.

How can I tell if the lender’s note certification under § 702.015 is defective?

To determine whether the lender’s note certification under § 702.015 is flawed, ensure it was submitted under penalty of perjury. The certification must confirm that the lender possesses the original promissory note and provide essential information, including the note’s location and the certifier’s authority, as required by Florida law.

If the lender claims the note is lost, what proof do they need to provide?

If a lender asserts that a note is lost, they are required to submit an affidavit detailing specific facts to establish their right to enforce the note. This affidavit should include evidence such as proof of prior possession or authorization to act on behalf of the noteholder, in accordance with Florida Statutes § 702.015.

Related Blog Posts

- 7 Legal Rights Every Florida Homeowner Should Know

- Deficiency Judgments in Florida: Key Facts

- Private Mortgage Foreclosure Process in Florida

- Lost Note Affidavits in Florida Foreclosures