Getting a mortgage after a short sale is possible, but it requires preparation and patience. A short sale impacts your credit and imposes waiting periods before you can apply for a new loan. Here’s what you need to know:

- Waiting Periods: Typically 2–7 years, depending on the loan type (FHA, VA, USDA, or conventional). Extenuating circumstances or a larger down payment can shorten this timeline.

- Credit Score Requirements: FHA loans require a minimum score of 500, while conventional loans usually need 620 or higher.

- Down Payment: FHA loans start at 3.5%, conventional loans at 3%, and VA/USDA loans may offer 0% options.

- Rebuilding Credit: Focus on paying bills on time, reducing debt, and keeping credit card usage below 30%.

To improve your chances, gather documentation for hardship events, save for a down payment, and monitor your credit report for errors. With the right steps, you can return to homeownership sooner than you think.

How Long After Short Sale Can I Buy A House? – CountyOffice.org

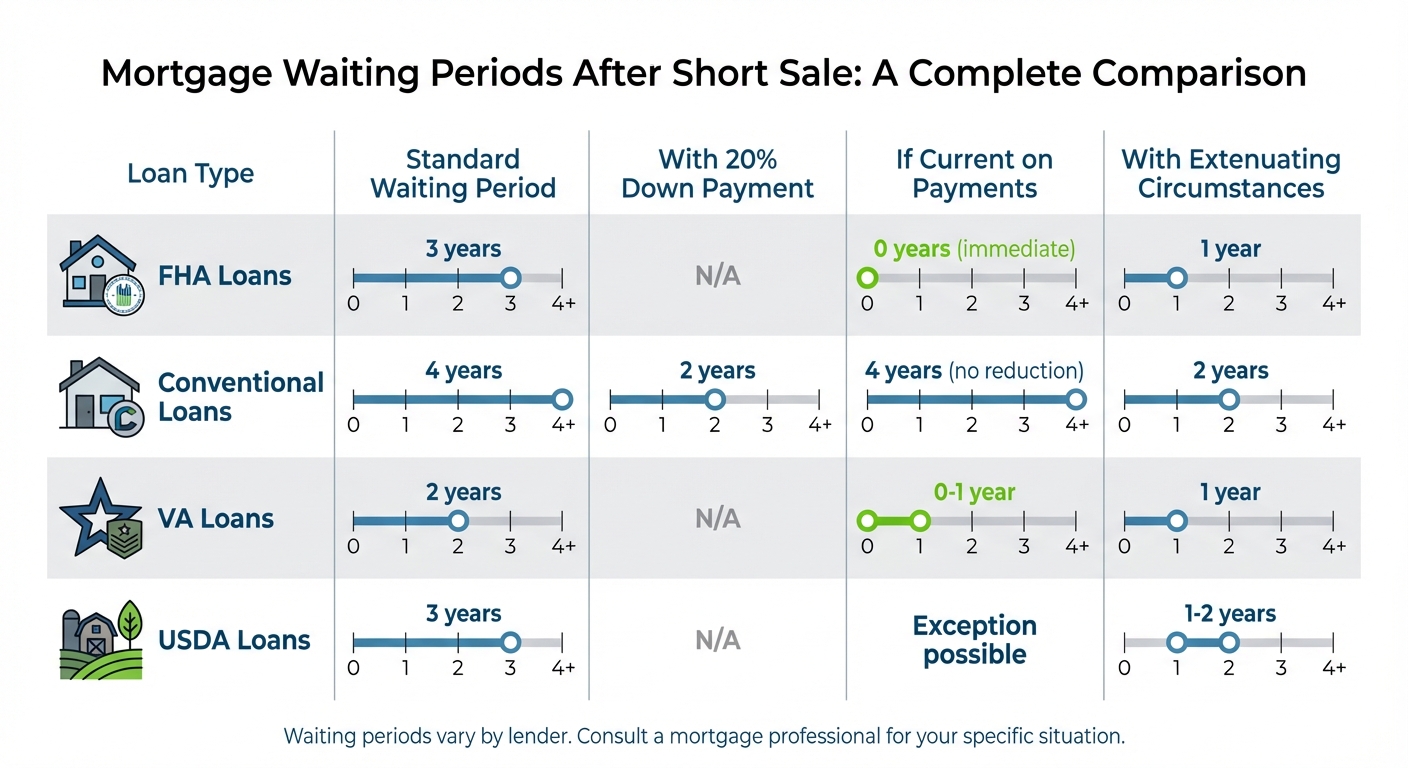

Waiting Periods for Different Mortgage Types

Mortgage Waiting Periods After Short Sale by Loan Type

The time you need to wait before applying for a new mortgage depends on the type of loan you’re pursuing. Let’s break down the waiting periods and requirements for FHA, conventional, VA, and USDA loans so you can better understand your options.

FHA Loan Waiting Period and Requirements

For FHA loans, the standard waiting period is 3 years from the date the property title was transferred. However, if you kept up with all mortgage and installment payments during the 12 months leading up to your short sale, you might qualify for a new FHA-insured loan right away. According to HUD 4000.1:

A Borrower is considered eligible for a new FHA-insured Mortgage if… all Mortgage Payments on the prior Mortgage were made within the month due for the 12-month period preceding the Short Sale.

If you can prove extenuating circumstances – like the death of a primary income earner or a serious illness – the waiting period may be reduced to 1 year. Additionally, you’ll need to show evidence of a 20% or more decline in household income lasting at least six months.

Conventional Loan Waiting Period and Requirements

For conventional loans backed by Fannie Mae or Freddie Mac, the typical waiting period is 4 years. However, if you can make a 20% down payment (resulting in an 80% loan-to-value ratio), Fannie Mae allows applications after just 2 years. On the other hand, if your loan-to-value ratio exceeds 90%, you may need to wait as long as 7 years.

If you’ve experienced extenuating circumstances, the standard 4-year wait could be shortened to 2 years. Unlike FHA loans, being current on payments before the short sale doesn’t automatically waive the waiting period, but it can improve your chances of approval.

VA and USDA Loan Options

For VA loans, which are available to eligible veterans and service members, the waiting period is generally 2 years. Some lenders may reduce this to 1 year if there were no late payments in the 12 months prior to the short sale.

USDA loans, designed for rural homebuyers, require a 3-year waiting period after the short sale. However, if your mortgage was current at the time of the short sale, you might qualify sooner. Non-qualifying (non-QM) mortgages, which often cater to borrowers with unique circumstances, may not require any waiting period, though they typically come with higher interest rates.

| Loan Type | Standard Wait | With 20% Down | If Current on Payments | With Extenuating Circumstances |

|---|---|---|---|---|

| FHA | 3 years | N/A | 0 years | 1 year |

| Conventional | 4 years | 2 years | 4 years | 2 years |

| VA | 2 years | N/A | 0–1 year | 1 year |

| USDA | 3 years | N/A | Exception possible | 1–2 years |

Now that you know the waiting periods, your next steps should focus on rebuilding your credit and gathering the necessary documentation to strengthen your mortgage application.

Steps to Rebuild Your Credit After a Short Sale

A short sale stays on your credit report for seven years from the date of your first missed payment. Rebuilding your credit during this time is essential if you want to qualify for a new mortgage. One of the first steps? Work on reducing your outstanding debts to improve your debt-to-income (DTI) ratio.

Paying Off Outstanding Debts

Lowering your outstanding debts can significantly improve your DTI ratio, which lenders typically prefer to be no higher than 43%. This ratio compares your monthly debt payments to your gross monthly income and is just as crucial as your credit score when you’re applying for a loan. Start by focusing on paying down credit card balances and installment loans. Even small balances paid on time show that you’re managing your finances responsibly. If you miss a payment, contact your creditors immediately to negotiate a solution. Missing a due date could drop your credit score by 100 points or more.

Building a Positive Payment History

"Payment history is the single most important factor used to calculate credit scores, so each month that passes without a late payment helps your credit scores improve".

Make it a priority to pay all your bills on time, including utilities and phone bills. You might also consider tools like secured credit cards or credit builder loans to establish a consistent record of on-time payments. Another tip? Keep your credit utilization low – ideally under 30% of your available credit. Those with excellent credit often maintain it below 10%. Lastly, monitor your credit report regularly to ensure your progress is accurately recorded.

Checking Your Credit Report Regularly

You can get free credit reports from Equifax, Experian, and TransUnion at AnnualCreditReport.com. Right now, you’re allowed to check these reports weekly at no cost. Reviewing your reports frequently can help you catch errors like misapplied payments, duplicate accounts, or debts that don’t belong to you (such as those from a former spouse). Since a short sale can already lower your score significantly, any mistakes could make things worse. If you spot an error, file a dispute with the credit bureau and contact the creditor involved. The bureau must verify the information, and if it can’t be confirmed, the error has to be corrected or removed.

sbb-itb-d613a70

Documenting Extenuating Circumstances

If your short sale happened because of an unforeseen crisis, providing proper documentation can help shorten your waiting period for a new loan. FHA, VA, USDA, and conventional loans may offer shorter timelines, depending on your lender’s specific underwriting rules. This not only lowers the lender’s risk but also aids in your overall credit recovery.

What Qualifies as Extenuating Circumstances?

"Extenuating circumstances are nonrecurring events that are beyond the borrower’s control that result in a sudden, significant, and prolonged reduction in income or a catastrophic increase in financial obligations."

- Fannie Mae Borrower Eligibility Fact Sheet

Events that typically qualify include job loss, a severe illness, or the death of the primary wage earner. In some cases, divorce may also meet the criteria – especially if your mortgage was up to date at the time of separation, but your ex-spouse, who was awarded the property, later defaulted. The key is that the event must be a one-time, unexpected occurrence that caused a major financial setback, from which you have since recovered.

How to Provide Proper Documentation

Once you’ve identified a qualifying event, gather the necessary paperwork to back your claim. Lenders will need verifiable proof of your circumstances. For example:

- Job loss: Termination or layoff notices work as strong evidence.

- Serious illness: Medical bills or hospital records can substantiate your claim.

- Death of a wage earner: A death certificate will be required.

- Divorce: Provide your divorce decree along with proof that the mortgage was current at the time of separation.

"Anything that a customer puts on the mortgage application today, we are going to ask for paperwork to verify."

- Ray Rodriguez, Regional Mortgage Sales Manager, TD Bank

Additionally, submit a concise, one-page hardship letter explaining the event and your financial recovery. Keep it factual and emphasize how you’ve rebuilt your finances since the incident. Lenders generally expect 12–24 months of positive credit history following the event before approving a new loan.

If you need help compiling your documentation or navigating the mortgage process after a short sale, reach out to Foreclosure Defense Group.

Meeting Lender Credit Score and Down Payment Requirements

Once you’ve completed the waiting period and documented your financial hardship, the next step is meeting the credit score and down payment criteria set by lenders. These requirements differ depending on the type of loan, so it’s essential to familiarize yourself with them early on to set realistic financial goals. Here’s a closer look at what you need to know about credit scores and down payments for different loan types.

Minimum Credit Score Requirements

For FHA loans, a FICO score of at least 580 qualifies you for a low 3.5% down payment. If your score is between 500 and 579, you can still qualify, but you’ll need to make a 10% down payment. Unfortunately, scores below 500 won’t meet FHA financing standards.

Conventional loans require a minimum credit score of 620. While VA loans don’t have an official minimum set by the Department of Veterans Affairs, most lenders expect a score of around 620. For USDA loans, a credit score of 640 is required for automated approval.

Keep in mind that some lenders may have stricter credit score requirements than the minimums listed here.

"A score is certainly important, but it isn’t the be all, end all. There are other things in place that could potentially slow your loan."

- Bob Walters, Chief Economist, Quicken Loans

To maintain or improve your credit score, aim to keep your credit card balances below 30% of your available limit and avoid applying for new credit before seeking a mortgage. These steps can help protect your score during the application process.

Saving for a Down Payment

Once you’ve met the credit score requirements, the next hurdle is saving for the down payment. The amount you’ll need varies by loan type and credit score. For example:

- FHA loans require a 3.5% down payment if your credit score is 580 or higher, but if your score is between 500 and 579, you’ll need to put down 10%.

- Conventional loans start with a 3% down payment, but if you’re utilizing extenuating circumstances to shorten the waiting period to three years, you’ll need to provide a 10% down payment. Additionally, a 20% down payment eliminates the need for private mortgage insurance (PMI).

- VA and USDA loans offer 0% down payment options for eligible borrowers.

In addition to the down payment, you’ll also need cash reserves for closing costs, taxes, insurance, and ongoing home maintenance. Building an emergency fund that covers three to six months of expenses is highly recommended. This financial cushion not only provides peace of mind but also reassures lenders, especially if you’re working with a lower credit score or a shorter waiting period.

Lastly, avoid making significant purchases while preparing for your mortgage. Lenders value stability in your financial accounts and may view large withdrawals or new debts as red flags.

| Loan Type | Minimum Down Payment | Minimum Credit Score |

|---|---|---|

| FHA | 3.5% (with a 580+ score) / 10% (with a 500–579 score) | 580 (for 3.5% down) / 500 (for 10% down) |

| Conventional | 3% (or 10% with extenuating circumstances) | 620 |

| VA | 0% | Around 620 (varies by lender) |

| USDA | 0% | 640 (for automated approval) |

Conclusion: Next Steps Toward Getting a New Mortgage

Securing a mortgage after a short sale requires careful planning and a thorough understanding of lender expectations. Waiting periods differ based on the type of loan, but factors like a larger down payment or proof of financial hardship can sometimes reduce these timelines.

Once you’re clear on the waiting period, your next priority should be improving your financial standing. Focus on rebuilding your credit by paying bills on time and keeping your credit utilization low. At the same time, work on saving for a bigger down payment, which can strengthen your application and potentially speed up the approval process.

While the journey back to homeownership is entirely possible, navigating lender requirements and gathering the necessary documentation can feel overwhelming. If you’re uncertain about your circumstances or need help identifying the best loan program for your situation, seeking guidance from a professional can be incredibly helpful. For example, Foreclosure Defense Group offers free consultations to help homeowners explore their options and create a tailored plan for qualifying for a mortgage after a short sale. With expert advice and a clear strategy, you can approach the process with confidence.

To get started, review your credit report, collect any hardship documentation, and continue saving for your down payment. With the right preparation and support, you’ll be well on your way to qualifying for a new mortgage and reclaiming homeownership.

FAQs

Can extenuating circumstances shorten the waiting period for a mortgage after a short sale?

Yes, certain extenuating circumstances – like a serious medical emergency or the death of a primary wage earner – can sometimes shorten the typical waiting period for getting a mortgage after a short sale. While conventional loans usually require a waiting period of at least two years, other loan programs, such as FHA, VA, or USDA loans, may offer exceptions in these kinds of situations.

To be considered, you’ll need to provide solid documentation, such as medical records or a death certificate, to prove the hardship was beyond your control and not tied to poor financial decisions. Lenders will also evaluate your financial recovery, looking for a clean credit history since the short sale and evidence of a stable income. If you’re unsure how to navigate this process, the Foreclosure Defense Group can help you compile the necessary documents and work with lenders to strengthen your case.

How can I rebuild my credit after a short sale?

Rebuilding your credit after a short sale isn’t an overnight process, but with a well-thought-out plan, you can make steady progress. Start by focusing on the basics: pay all your bills on time. Since payment history carries the most weight in your credit score, setting up automatic payments or reminders can help ensure you never miss a due date. It’s also smart to create a budget that prioritizes essential expenses while carving out a strategy to pay down any lingering debts.

If you’re looking to rebuild or strengthen your credit, consider tools like a secured credit card or a credit-builder loan. Use these responsibly by keeping your balances low – preferably under 30% of your credit limit – and aim to pay them off in full each month. Alongside this, make it a habit to review your credit reports regularly. Spotting and disputing any errors can lead to quick improvements in your score.

Be mindful of applying for new credit, as too many hard inquiries can temporarily lower your score. At the same time, keep older accounts open to maintain a longer credit history, which also benefits your credit profile. If navigating the aftermath of a short sale feels overwhelming or you need legal guidance, Foreclosure Defense Group offers expert support to help safeguard your financial future.

What are the down payment requirements for FHA, VA, and conventional loans after a short sale?

FHA loans come with a minimum down payment of 3.5%, and the good news is that this amount can often be covered through a gift or down payment assistance programs – even after experiencing a short sale.

VA loans, designed for eligible veterans and service members, stand out as the only option that doesn’t require any down payment, provided the required waiting period has been completed.

Conventional loans usually call for a minimum of 3% down, but if you’re able to put down 20%, you can skip private mortgage insurance (PMI) and potentially lock in better loan terms. After a short sale, lenders might ask for larger down payments due to the added risk, but these baseline requirements still hold.

Related Blog Posts

- Short Sale Guide: Options for Underwater Mortgages

- How Long Foreclosure Stays on Credit Reports

- Short Sale Document Requirements Explained

- Checklist: FHA Foreclosure Relief Eligibility