If you’re behind on your mortgage and facing foreclosure, private lender refinancing could help you save your home. Unlike banks, private lenders focus on your home equity instead of your credit score or payment history. They can act quickly – often closing loans within 1–2 weeks – making them a viable option when time is running out. Here’s how it works:

- What It Is: A new loan from private lenders to pay off overdue mortgage payments and stop foreclosure.

- Who It Helps: Homeowners with missed payments, poor credit, or those already in foreclosure.

- Key Advantages: Faster processing, flexible qualification criteria, and focus on home equity over credit.

- Potential Downsides: Higher interest rates, shorter repayment terms, and limited legal protections.

Private refinancing can reinstate your mortgage and provide a fresh start, but it’s essential to act quickly. Pairing this option with legal assistance can further protect your rights and improve your chances of keeping your home.

Refinancing Out of Foreclosure

When to Consider Private Lender Refinancing

Private lender refinancing becomes a lifeline when missed mortgage payments make traditional banks turn you away. Even a single missed payment can hurt your credit score, as banks quickly report delinquencies to credit bureaus like Equifax, TransUnion, and Experian. Unlike banks that require all payments to be current, private lenders focus primarily on home equity.

If you’ve missed payments for 120 days, foreclosure proceedings can legally begin, making approval from traditional lenders almost impossible. This is where private lenders step in, offering options that banks won’t. They prioritize the equity in your home over your credit score or payment history, which means their qualification process looks very different from that of a bank.

Who Qualifies for Private Lender Refinancing

Private lender refinancing could be a solution if you’ve missed payments, have a credit score under 620, or are already facing foreclosure. Most private lenders look for a loan-to-value (LTV) ratio between 75% and 85% for new purchases and up to 80% for refinancing. This means having enough equity in your home is key.

"Private mortgages are designed for borrowers who may have a hard time qualifying for traditional financing." – Jamie Johnson, Personal Finance Expert

This option is often ideal for self-employed individuals, commission-based workers, or anyone without two years of consistent income. Private lenders are more flexible in verifying income, often accepting bank statements or other alternative documentation instead of traditional W-2s or tax returns. Since the property serves as the main collateral, the home’s value carries more weight than your job status.

Why Traditional Banks Deny Refinancing

The differences in qualification criteria explain why banks reject so many refinancing applications. For instance, most banks require a credit score of at least 620. They also reject applicants with high debt-to-income (DTI) ratios – typically anything above 43% to 50% – or insufficient home equity (less than 20%). If you’re "underwater" on your mortgage, meaning you owe more than your home’s worth, traditional refinancing is almost impossible.

"People with bad credit generally can’t qualify for a mortgage refinance, let alone one with better terms than they already have." – Amy Loftsgordon, Attorney

Once you’ve reached 120 days of missed payments and entered foreclosure, traditional refinancing becomes completely off the table. Common financial challenges that lead to bank denials include job loss, medical bills, divorce, adjustable rate resets, and even natural disasters. If you’re dealing with any of these hardships and a bank has already denied your application, turning to private lender refinancing might be your best chance to stop foreclosure before the sale date arrives.

How to Refinance with Private Lenders

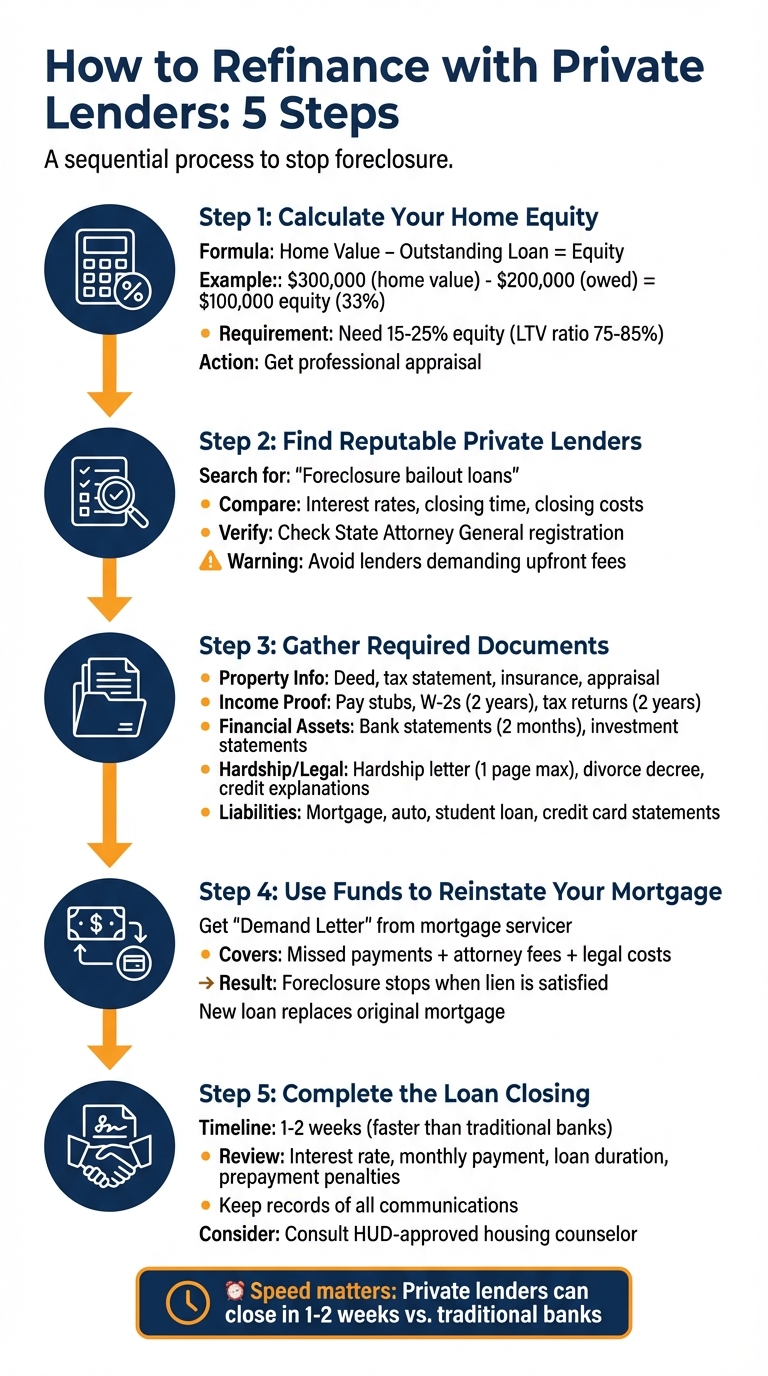

5 Steps to Refinance with Private Lenders and Stop Foreclosure

If banks have turned you down and you’re facing foreclosure, private lenders might be your solution. But acting quickly is key – foreclosure sales won’t wait. Here’s a step-by-step guide to navigate refinancing through private lenders effectively.

Step 1: Calculate Your Home Equity

Private lenders focus on equity, not credit scores. To figure out your equity, subtract your total outstanding loan balances from your property’s current market value. For example, if your home is worth $300,000 and you owe $200,000, your equity is $100,000 – about 33% of the home’s value. Most private lenders require a loan-to-value (LTV) ratio of 75% to 85%, meaning you’ll need at least 15% to 25% equity to qualify.

To confirm your home’s value, consider getting a professional appraisal or reviewing recent comparable sales in your area. Don’t forget to factor in closing costs when calculating equity – this step is essential, as insufficient equity could disqualify you even with private lenders.

Step 2: Find Reputable Private Lenders

Search for private lenders specializing in "foreclosure bailout loans", which are tailored for homeowners in urgent situations. Compare terms like interest rates, time to close, and whether closing costs can be included in the loan balance. Some lenders even offer rate locks for a fee, protecting you from rate changes during the application process.

Verify a lender’s legitimacy by checking their registration with your State Attorney General. Be cautious of lenders demanding upfront fees before providing services – this could be a sign of fraud.

Step 3: Gather Required Documents

Private lenders will need documentation to verify your property’s value, income, and financial hardship. Here’s a quick overview of what to prepare:

| Document Category | Required Documents |

|---|---|

| Property Info | Recorded deed, property tax statement, homeowners insurance, recent appraisal |

| Proof of Income | Recent pay stubs, W-2s (2 years), tax returns (2 years) |

| Financial Assets | Bank statements (2 months), retirement/investment statements |

| Hardship/Legal | Hardship letter, divorce decree (if applicable), credit issue explanation letters |

| Liabilities | Current mortgage, auto loan, student loan, and credit card statements |

Your hardship letter is particularly important. Keep it concise – no more than one page – and stick to the facts. Explain the event that caused your financial hardship, such as job loss, medical issues, or divorce, without adding unnecessary personal details.

"A brief hardship letter works best. The letter definitely shouldn’t exceed one page. Just state the facts that are relevant to making your case." – Amy Loftsgordon, Attorney, University of Denver Sturm College of Law

Jon Meyer, a licensed mortgage loan originator, advises being over-prepared: "In terms of tax documents, have two years’ worth of W-2s and tax returns ready, just in case. It’s better to have more documentation than less." Self-employed borrowers should also prepare items like year-to-date financial statements, business licenses, and business tax returns.

Once your documents are ready, you can move on to reinstating your mortgage.

Step 4: Use Funds to Reinstate Your Mortgage

The funds from your private refinance will be used to cover all past-due amounts, including fees and legal costs. Your original mortgage servicer will provide a "Demand Letter" or "Notice to Accelerate", outlining the exact amount needed to stop foreclosure. This typically includes missed payments and any attorney fees if your case has reached the lender’s legal team.

Once you pay this amount using the refinance funds, the foreclosure process stops because the lien is satisfied. The private loan replaces your original mortgage, giving you a fresh start with new terms.

"The further behind you become, the harder it will be to reinstate your loan and the more likely that you will lose your house." – U.S. Department of Housing and Urban Development (HUD)

Step 5: Complete the Loan Closing

The final step is signing your new loan agreements and thoroughly reviewing the terms. Private lenders often move faster than traditional banks because they understand the urgency of foreclosure timelines. During closing, review the interest rate, monthly payment, loan duration, and any prepayment penalties. Make sure you fully understand all fees before signing.

Keep a detailed record of all communications with your lender. Once the closing is complete, your original mortgage is paid off, foreclosure is halted, and you begin making payments on the new private loan. While private loans often come with higher interest rates due to the increased risk, they can save your home from foreclosure.

Before committing to a high-interest private loan, consider consulting a HUD-approved housing counselor. These counselors offer free advice and can help you explore other options. Legal guidance may also be valuable to ensure you’re making the best decision for your financial future.

sbb-itb-d613a70

Pros and Cons of Private Lender Refinancing

Private lender refinancing can be a lifeline for homeowners facing foreclosure when traditional banks won’t step in, but it comes with its share of challenges. Here’s a closer look at what to expect.

Benefits of Private Lender Refinancing

One of the biggest advantages is speed. Private lenders can close deals in as little as 1 to 2 weeks, which is crucial when you’re on the brink of foreclosure.

Another key benefit is their flexibility with credit requirements. Unlike traditional lenders, which often demand a minimum credit score of 620 and a debt-to-income ratio below 43%, private lenders focus more on your home’s equity. This makes it possible to qualify even if you’ve missed multiple mortgage payments. For example, one private program successfully helped prevent over 1,200 evictions, preserving wealth within communities. These loans are often a last resort for homeowners who have been denied other options, such as loan modifications or forbearance.

While these benefits can provide much-needed relief, there are notable drawbacks to consider.

Drawbacks of Private Lender Refinancing

The most significant downside is cost. Private lenders typically charge higher interest rates than banks because they take on greater risk by lending to financially distressed homeowners. As BlueHub SUN explains:

"Your interest rate may be higher than the rates you see advertised by regular mortgage lenders because regular mortgage lenders usually require better credit than SUN clients have"

Closing costs can also be steep, often ranging from 2% to 6% of the loan amount.

Additionally, private loans often come with shorter repayment terms. Many are structured as temporary bridge loans, lasting up to two years, and may include balloon payments that require refinancing or a large lump sum at the end. Legal protections are also limited compared to conventional loans. Financial writer Jamie Johnson notes:

"Private mortgages don’t offer the same legal protections you’ll receive from a licensed financial institution"

Contracts may include strict default clauses, high late fees, and prepayment penalties, which can add financial strain.

Lastly, the risk of foreclosure doesn’t disappear. If you fail to meet the new payment terms, private lenders can still foreclose on your home. In cases of debt forgiveness (a "short refinance"), your credit score may take a hit, and the forgiven amount could be considered taxable income by the IRS. After a foreclosure, homeowners may face a waiting period of 2 to 7 years before qualifying for another mortgage.

Comparison Table: Private Lender Refinancing Pros and Cons

| Advantages | Disadvantages |

|---|---|

| Quick closing – 1 to 2 weeks | Higher interest rates due to increased risk |

| Approval based on home equity, not credit score | Closing costs typically range from 2% to 6% of the loan amount |

| Accessible during foreclosure or bankruptcy | Short repayment terms with potential balloon payments |

| Can reinstate your mortgage quickly | Limited legal protections compared to traditional loans |

| Some programs require no down payment | Debt forgiveness may affect credit and result in taxable income |

Weighing these pros and cons is crucial to determining whether private lender refinancing aligns with your foreclosure defense strategy.

Combining Private Refinancing with Legal Defense

Teaming up private lender refinancing with skilled legal representation creates a powerful approach to managing foreclosure. Refinancing provides the funds to settle your overdue mortgage, while an attorney ensures you have the legal backing to delay foreclosure long enough for the refinancing process to finalize. This combination not only buys time but also helps protect your legal rights. Let’s dive into how foreclosure defense services can enhance your refinancing efforts.

Using Refinancing with Foreclosure Defense Services

When paired with private refinancing, foreclosure defense services can significantly strengthen your strategy to avoid losing your home. Attorneys specializing in foreclosure defense can identify lender violations, such as dual tracking – where the foreclosure process continues even though your application is still under review – and ensure all mitigation applications are properly handled to support your refinancing efforts.

"Violations of HBOR [Homeowner Bill of Rights] can give homeowners grounds to challenge foreclosure in court." – Sternberg Law Group

Having legal representation ensures that all applications for mitigation are complete and accurate, which can prevent foreclosure from advancing due to technical errors. Additionally, filing for Chapter 13 bankruptcy can trigger an automatic stay, effectively pausing foreclosure proceedings and providing critical breathing room.

Why Legal Guidance Helps

While refinancing addresses the financial aspect, legal guidance tackles procedural hurdles. Attorneys work to protect homeowners from mistakes and unfair practices during the foreclosure process. They meticulously document communications with mortgage servicers – an essential step if legal action becomes necessary. Furthermore, they negotiate directly with servicers to ensure compliance with federal loss mitigation regulations, often helping homeowners secure more favorable terms.

"Lenders may be willing to ‘bend’ if you have an experienced negotiator, like a foreclosure lawyer, working on your case." – StopForeclosuresHelp

In California, homeowners have the right to reinstate their mortgage up to five business days before the trustee’s sale, making timely legal intervention critical. Firms like Foreclosure Defense Group offer free consultations to assess your situation and craft a strategy tailored to your needs. Moreover, legal representation helps shield homeowners from foreclosure rescue scams – fraudulent schemes that charge upfront fees without providing real assistance.

Taking Action to Stop Foreclosure

Key Takeaways

If you’re facing foreclosure, time is of the essence. Federal law gives you a 120-day grace period after your first missed payment before formal foreclosure proceedings can start. This window is critical – it allows you time to explore refinancing options with private lenders and secure legal assistance. Acting quickly can help you avoid mounting fees, legal expenses, and interest that could worsen your financial situation. Also, keep in mind that after a foreclosure is finalized, you may need to wait 2 to 7 years before being eligible for another mortgage.

Understanding these points can empower you to take proactive steps to protect your home.

Next Steps for Homeowners

The moment you realize you might have trouble making mortgage payments, reach out to your mortgage servicer. Early communication can unlock loss mitigation programs that might not be available once foreclosure proceedings begin. Additionally, assess your home equity to see if refinancing is an option. You’ll need sufficient equity to qualify for a private loan that can cover your overdue payments.

Be cautious when researching private lenders – steer clear of scams that demand large upfront fees. For extra support, seek advice from HUD-approved housing counselors who can guide you through your options. Combining a private refinancing plan with legal assistance can significantly improve your chances of keeping your home. Work closely with your foreclosure defense attorney to identify any lender violations and safeguard your rights during the refinancing process. For personalized help, Foreclosure Defense Group offers free consultations to help you craft a strategy that integrates refinancing with legal protection.

FAQs

How can I tell if I have enough equity to refinance with a private lender?

To figure out if you have enough equity for private lender refinancing, you’ll first need to calculate your home equity. Start by subtracting your current mortgage balance from your home’s estimated market value. For instance, if your home is valued at $350,000 and your mortgage balance is $250,000, your equity comes out to $100,000.

The next step is to determine your loan-to-value (LTV) ratio. To do this, divide the loan amount you’re seeking (including any cash-out) by your home’s appraised value, then multiply the result by 100. Private lenders typically prefer an LTV of 80% or less, which means you should aim to keep at least 20% equity in your property. If your LTV is above this threshold, you may need to lower the loan amount, pay down your mortgage principal, or wait for your property’s value to increase.

If foreclosure is a concern, Foreclosure Defense Group can help you explore your options, including refinancing or other strategies to safeguard your home and financial stability.

What challenges come with higher interest rates and shorter terms when refinancing with private lenders?

Refinancing with private lenders often leads to higher interest rates, which can make a big dent in your monthly budget. For example, even a small increase in rates on a $1,500 monthly payment could add hundreds of dollars, making it tougher to keep up with your financial commitments. On top of that, many private loans come with adjustable rates, meaning your payments could rise unexpectedly if the index they’re tied to goes up.

Another challenge is the shorter repayment terms, typically around 5 to 7 years. Unlike the extended timeline of a standard 30-year mortgage, these shorter terms require homeowners to pay off the loan much faster. This results in higher monthly payments, which can create financial pressure, lead to missed payments, or even leave you facing a large balloon payment at the end of the term.

To navigate these risks, it’s a smart move to consult experienced legal professionals, like the team at Foreclosure Defense Group. They can help you negotiate better terms and develop a plan to safeguard your home and maintain financial stability.

How does legal support improve the success of private lender refinancing to stop foreclosure?

Legal support plays a crucial role in making private lender refinancing a smoother and more effective process for homeowners. Attorneys help borrowers fully grasp their rights and navigate their options, ensuring they’re in the best position to make informed decisions. They can evaluate whether a homeowner qualifies for refinancing and steer them toward loans with better terms – like reduced interest rates or longer repayment periods – that can lower monthly payments and help avoid foreclosure.

Lawyers also bring value by crafting detailed hardship letters that clearly explain financial struggles, such as job loss or unexpected medical bills. These letters can strengthen a borrower’s case for approval. Additionally, attorneys carefully review loan agreements to spot and negotiate the removal of problematic terms, such as hidden fees or penalties, which might cause trouble down the road.

If refinancing hits roadblocks or foreclosure proceedings persist, legal professionals can step in with strategies like invoking loss mitigation rights or exploring bankruptcy options. These measures can delay foreclosure, buying homeowners more time to secure the financing they need. With skilled legal guidance, private lender refinancing becomes a more dependable way to regain financial footing.

Related Blog Posts

- How Attorneys Help Resolve Mortgage Disputes

- How to Refinance from ARM to Fixed-Rate Mortgage

- Top 3 Scenarios for Deed-in-Lieu Over Foreclosure

- Emergency Motion to Halt Foreclosure Sale