Refinancing with poor credit is challenging, but it’s not impossible. Several programs cater to borrowers with low credit scores, offering ways to lower monthly payments, access home equity, or stabilize finances. Here’s a quick breakdown of the options:

- FHA Streamline Refinance: No equity required, lower rates, but only for current FHA borrowers and no cash-out allowed.

- FHA Cash-Out Refinance: Access up to 80% of your home’s value, but stricter credit and equity requirements apply.

- VA IRRRL: Exclusive to veterans with VA loans, focuses on payment history over credit scores.

- USDA Streamline Refinance: Designed for rural homeowners with USDA loans, no credit checks for certain options.

- Non-QM Loans: Flexible for those with recent financial issues but comes with higher rates and shorter terms.

- Private Lenders: Fast approval and no strict credit requirements, but higher costs and shorter loan terms.

Each option has unique benefits and limitations, so it’s important to match the program to your financial situation. Below is a comparison table to help you decide.

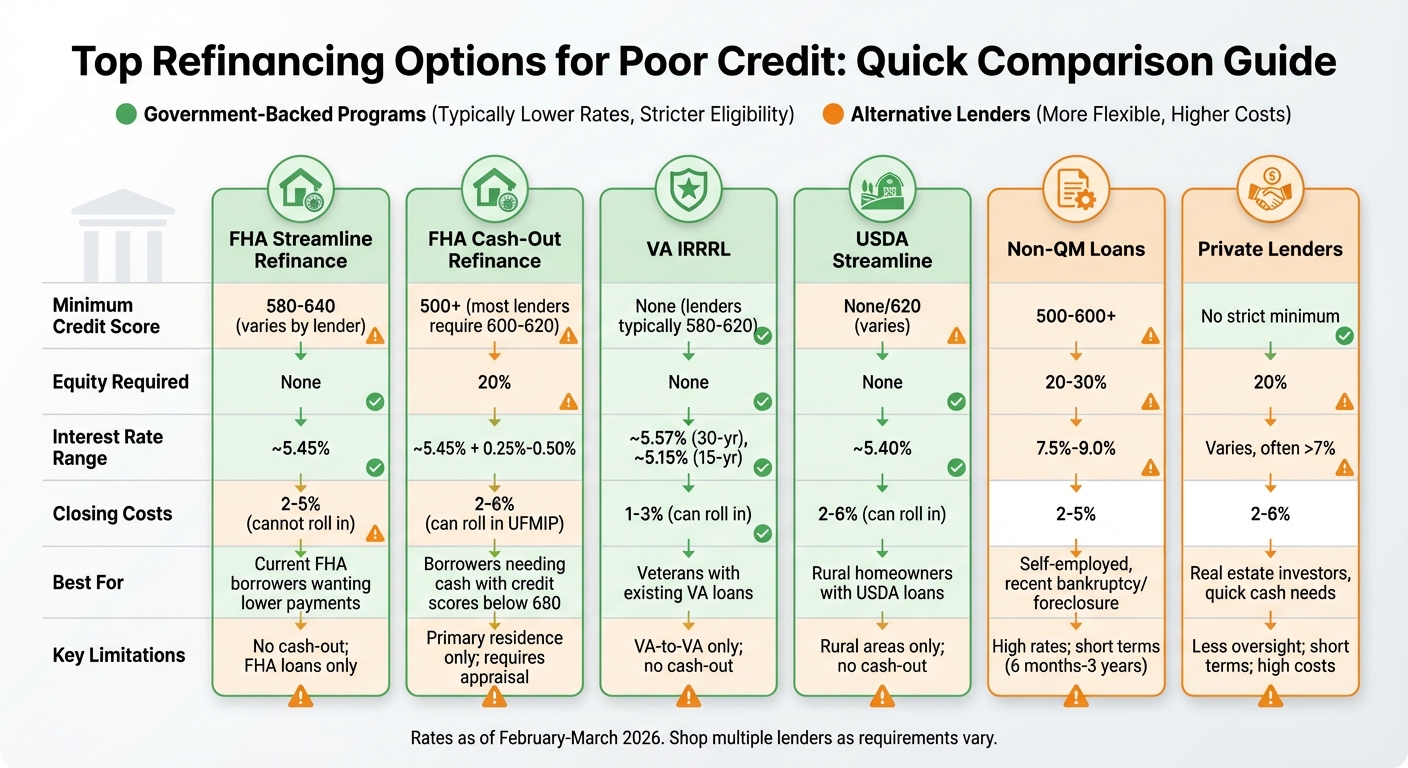

Quick Comparison

| Program | Min. Credit Score | Equity Required | Interest Rate Range | Best For | Key Limitations |

|---|---|---|---|---|---|

| FHA Streamline | 580-640 (varies) | None | ~5.45% | Current FHA borrowers | No cash-out; only for FHA loans |

| FHA Cash-Out | 500+ | 20% | ~5.45% + 0.25%-0.50% | Borrowers needing cash | Requires appraisal; higher equity |

| VA IRRRL | None (varies) | None | ~5.57% | Veterans with VA loans | No cash-out; VA-to-VA only |

| USDA Streamline | None/620 (varies) | None | ~5.40% | Rural USDA loan holders | Rural areas only; no cash-out |

| Non-QM Loans | 500+ | 20%-30% | 7.5%-9.0% | Recent financial challenges | High rates; short terms |

| Private Lenders | None | 20% | Varies, often >7% | Quick cash, real estate investors | High costs; short terms |

If your credit is poor, consider government-backed programs like FHA, VA, or USDA loans for lower rates and flexible requirements. For urgent cash or unique situations, Non-QM and private lenders can help, but they come with higher costs. Always shop around and calculate your break-even point to ensure refinancing makes financial sense.

Refinancing Options for Poor Credit: Program Comparison Chart

How to Get a Cash Out Refinance with Bad Credit | Top 3 Options

sbb-itb-d613a70

1. FHA Streamline Refinance

The FHA Streamline Refinance is a refinancing option that provides opportunities for borrowers with less-than-perfect credit. While it’s designed to be accessible, many lenders still require a credit score between 580 and 640. This program can be especially helpful if your credit score has dropped since you first bought your home.

Minimum Credit Score

For most lenders, a credit score between 580 and 640 is necessary to qualify. Dan Green from The Mortgage Reports highlights the FHA’s goal:

"It’s in the FHA’s best interest to help as many people as possible qualify for today’s competitive mortgage rates. Lower mortgage rates mean lower monthly payments, which, in theory, leads to fewer loan defaults."

Equity Required

One major advantage of this program is that no equity is required. Since a home appraisal isn’t necessary, lenders use your original purchase price as the current value of your home. This means even borrowers with little or no equity – or those underwater on their mortgage – can refinance. Skipping the appraisal also saves you $300–$1,000.

Interest Rate Range

As of late February 2026, the average 30-year fixed FHA refinance rate was about 5.45% (6.67% APR), which is lower than the 6.07% average for conventional refinances. To qualify, you’ll need to show that the refinance provides a financial benefit, such as lowering your combined interest rate and annual mortgage insurance premium by at least 0.5%. This structure makes it an appealing choice for eligible borrowers.

Closing Costs

Closing costs for an FHA Streamline Refinance usually range from 2% to 5% of the loan balance. For a $150,000 loan, this means costs of $3,000 to $7,500. These fees must typically be paid upfront, as they can’t be added to the new loan balance – though the 1.75% upfront mortgage insurance premium (UFMIP) can be financed. Some lenders offer "no-cost" refinances by covering fees in exchange for a slightly higher interest rate. Additionally, if you refinance within 36 months, you might qualify for a partial UFMIP refund, which decreases over time.

Best For

This option works well for homeowners with an existing FHA loan who want to lower their monthly payments without dealing with a lot of paperwork. It’s particularly helpful for borrowers dealing with poor credit, low equity, or reduced income. To qualify, at least 210 days must have passed since your last closing, and you need to have made at least six on-time payments.

Limitations

The FHA Streamline Refinance is strictly for borrowers with an existing FHA loan, so it’s not available for conventional mortgages. It also doesn’t allow for cash-out refinancing, except for a small amount (up to $500). If you’re removing a borrower (unless due to death or divorce) or if your new payment increases by more than 20%, you’ll need to go through the credit-qualifying version, which requires full income and credit verification.

2. FHA Cash-Out Refinance

The FHA Cash-Out Refinance program lets homeowners tap into their home equity by refinancing their existing mortgage – whether it’s an FHA or conventional loan. Unlike the FHA Streamline Refinance, this option allows borrowers to access up to 80% of their home’s appraised value, with the difference paid out as cash. This makes it a practical choice for homeowners with lower credit scores who need funds for purposes like consolidating debt, making home improvements, or covering major expenses.

Minimum Credit Score

Although the FHA officially sets the minimum credit score at 500, most lenders require a higher score for cash-out refinances – usually between 600 and 620. Tim Lucas from The Mortgage Reports clarifies:

"The official FICO credit score minimum for all FHA loans is 500. However, a realistic minimum that lenders will actually allow is somewhere between 600 and 660 or higher."

Borrowers with credit scores between 500 and 579 will face stricter conditions, while those with scores of 580 or higher can qualify for the full 80% loan-to-value (LTV) ratio.

Equity Requirements

To qualify, you must retain at least 20% equity in your home, which means the maximum loan-to-value ratio is 80%. Additionally, the property must serve as your primary residence, and you need to have lived there for at least 12 months. A clean payment history is critical – no more than one 30-day late payment in the past year, and none within the last three months.

Interest Rate Range

As of late February 2026, the average 30-year fixed FHA refinance rate was around 5.45% (6.67% APR). FHA cash-out refinance rates are typically 0.25%–0.50% higher than standard FHA refinance rates, but they tend to be more stable for borrowers with lower credit scores. Kevin Walsh, a production coach and former loan officer at Refi.com, explains:

"Most homeowners, except those with the highest credit scores, will likely be quoted lower cash-out rates with an FHA-backed loan."

Closing Costs

Expect closing costs to range from 2% to 6% of the loan amount. While some fees must be paid upfront, the Upfront Mortgage Insurance Premium (UFMIP) of 1.75% can be rolled into the loan balance. Annual mortgage insurance premiums, which range from 0.5% to 0.8%, typically remain in place for at least 11 years, adding to your monthly expenses.

Best For

This option is particularly appealing to homeowners with credit scores below 680 who need access to their home equity but may not qualify for competitive rates elsewhere. It’s especially useful for debt consolidation. Stan Reinford, a mortgage loan originator at Movement Mortgage, explains:

"This loan is definitely more helpful for people who can’t qualify for other cash loans where they need access to the equity in their home."

Limitations

While the FHA Cash-Out Refinance expands access to home equity, there are some hurdles to consider. This program is limited to primary residences – it’s not available for second homes or rental properties. A full appraisal is required, which adds both time and cost to the process. Borrowers must also meet a debt-to-income (DTI) ratio limit of 43%, although some lenders may stretch this to 50% if compensating factors, such as high cash reserves, are present. Additionally, FHA mortgage insurance may remain for the life of the loan, so borrowers should weigh the potential benefits of a lower interest rate against the long-term cost of insurance.

3. VA Interest Rate Reduction Refinance Loan (IRRRL)

The VA Interest Rate Reduction Refinance Loan (IRRRL) offers veterans and service members a chance to refinance their existing VA loans, even if their credit has taken a hit. Instead of focusing on your current credit score, this program prioritizes your payment history, making it an accessible option for borrowers who might otherwise face challenges refinancing.

Minimum Credit Score

The Department of Veterans Affairs doesn’t impose a minimum credit score requirement for the IRRRL program. That said, most lenders typically look for scores between 580 and 620. If your score has dropped but you’ve consistently made on-time payments, you may still qualify.

Equity Required

One of the standout features of the VA IRRRL is that no equity is required. You can refinance even if your home’s value has decreased and you owe more than it’s worth. Since no appraisal is necessary, the program relies on the performance of your current VA loan instead of your home’s market value or credit score.

Interest Rate Range

As of March 1, 2026, the average 30-year fixed VA refinance rate was 5.57% (5.71% APR), while the 15-year fixed rate averaged 5.15% (5.36% APR). VA rates are generally 0.5% to 1.0% lower than conventional mortgage rates. To qualify, the refinanced rate must drop by at least 0.5% for fixed-to-fixed loans or 2% when switching from a fixed to an adjustable rate. These competitive rates, combined with flexible closing cost options, make the program appealing to many borrowers.

Closing Costs

Closing costs for a VA IRRRL typically range from 1% to 3% of the loan amount. This includes a 0.5% VA funding fee and an origination fee of up to 1%. The good news? These costs, along with the funding fee, can be rolled into your new loan balance, allowing you to refinance without paying out-of-pocket. About 35% to 40% of borrowers qualify for a funding fee exemption, such as those receiving disability compensation or surviving spouses of veterans who passed away from service-related disabilities.

Lenders also require that the monthly savings from your refinanced loan cover the closing costs within 36 months. Jodi Ulrich, Area Manager at Novus Home Mortgage, sums it up well:

"The best refinance is the one that pays for itself. If the math clears the 36-month mark, the choice is clear."

Best For

This program is a solid choice for veterans with an existing VA loan who want to lower their monthly payments or switch from an adjustable to a fixed rate. It’s particularly helpful for those dealing with credit challenges or declining home values.

Limitations

The IRRRL is only available to borrowers who currently hold a VA loan – it can’t be used to refinance conventional, FHA, or USDA loans. Additionally, the program doesn’t allow cash-back at closing, except for up to $6,000 earmarked for energy-efficient home improvements. To qualify, borrowers must have made at least six consecutive monthly payments on their current loan, and at least 210 days must have passed since the first payment due date. The new loan term cannot exceed the original term by more than 10 years, with a maximum term of 30 years and 32 days.

4. USDA Streamline Refinance

The USDA Streamline Refinance program is designed to help rural homeowners reduce their monthly mortgage payments. Among its options, the Streamline-Assist stands out, especially for borrowers with less-than-perfect credit. This option eliminates credit checks, income verification, and debt-to-income requirements, making it an accessible choice for many homeowners. Below are its key details.

Minimum Credit Score

One of the most flexible aspects of the Streamline-Assist Refinance is that it doesn’t require a credit check or a minimum credit score. This makes it an excellent option for borrowers whose credit has worsened since they first took out their loan. By comparison, other USDA refinance programs, like the Standard Streamline, generally require a minimum credit score of 640.

Equity Required

No home equity is required to qualify. Since appraisals are waived, you can refinance even if you owe more than your home is currently worth. This feature is particularly helpful for homeowners in areas where property values have dropped.

Interest Rate Range

USDA refinance loans offer competitive rates. For example, the average rate for a 30-year fixed USDA refinance is 5.40%, which is lower than the 6.07% seen with standard 30-year fixed-rate loans. If you have a USDA Direct loan, rates as of December 1, 2025, were 5%, with subsidies potentially reducing them to as low as 1%. To qualify for the Streamline-Assist, your new loan must reduce your monthly payment by at least $50.

Closing Costs

Expect closing costs to range between 2% and 6% of the loan amount. These costs include a 1% upfront guarantee fee, which can be rolled into the loan balance, allowing for a no-cash-out-of-pocket refinance. Additionally, an annual fee of 0.35% of the loan balance is applied and is typically included in your monthly payments.

Best For

This program is ideal for current USDA loan holders who may have experienced income reductions, accumulated higher debt, or seen their credit scores decline. However, borrowers must have made on-time payments for at least 12 months to qualify.

Limitations

The USDA Streamline Refinance is limited to borrowers with existing USDA loans. Cash-out refinancing is not allowed, and the property must remain your primary residence. Additional requirements include meeting USDA household income limits, which are generally set at 115% of the area median income, and holding your current loan for at least 12 months. For the Streamline-Assist option, you also cannot have had any late payments in the last year.

5. Non-QM Lender Programs for Bad Credit

After exploring government-backed options, Non-QM programs provide an alternative path for borrowers who don’t meet traditional lending criteria.

Non-Qualified Mortgage (Non-QM) loans are designed for homeowners who fall outside the standard requirements for conventional refinancing. These loans sidestep the usual Qualified Mortgage rules, allowing manual underwriting and the use of alternative documentation, such as bank statements, instead of W-2s or tax returns. As of 2026, Non-QM loans account for about 4.5% of the U.S. mortgage market, catering to self-employed individuals, real estate investors, and those recovering from financial difficulties.

Minimum Credit Score

Most Non-QM lenders accept credit scores ranging from 580 to 600, but certain programs may go as low as 500. To qualify at the lower end, borrowers often need compensating factors like substantial cash reserves or a sizable down payment.

Equity Requirements

Non-QM loans come with higher equity demands due to increased risk. Typically, borrowers need 20% to 30% equity in their home, translating to a loan-to-value (LTV) ratio of 70-80%. For those with lower credit scores, a 25% equity cushion or more is often required. Unlike government programs with minimal equity requirements, this ensures lenders minimize their risk exposure.

Interest Rates

Interest rates for Non-QM loans are higher than traditional mortgages. In 2026, general Non-QM rates range between 5.5% and 8.5% APR, while borrowers with poor credit can expect rates from 7.5% to 9.0% APR. These rates are generally 0.5% to 2% higher than those of conforming loans. For example, a borrower with a 580 credit score secured an 8.0% APR Non-QM refinance, using a 60% LTV loan to consolidate mortgage and credit card debt, saving around $400 per month.

Closing Costs

Closing costs for Non-QM loans typically fall between 2% and 5% of the loan amount. In the earlier example, the borrower paid $9,600 in closing costs (4% of the loan), which was added to the loan balance.

Best For

Non-QM loans are ideal for:

- Self-employed individuals who can provide 12-24 months of bank statements to document income.

- Real estate investors relying on DSCR (Debt Service Coverage Ratio) loans based on rental income.

- Borrowers with high debt-to-income ratios exceeding 50%.

- Those with recent credit challenges, as some programs allow refinancing as soon as one day after bankruptcy or foreclosure.

Limitations

The flexibility of Non-QM loans comes at a price. Borrowers face higher interest rates and may encounter terms like interest-only payments or balloon payments. The market for Non-QM lenders is smaller, so comparing offers from at least three to five providers is critical, as terms can vary widely. Since these loans are not sold to Fannie Mae or Freddie Mac, each lender sets its own criteria. Non-QM loans are best viewed as a short-term solution, giving borrowers time to improve their credit and refinance into a lower-rate conventional loan later.

6. Private Lender Refinancing Options

Private lenders provide refinancing options tailored for homeowners with poor credit, focusing more on property value and available equity than rigid credit score requirements. This approach, often referred to as asset-based lending, makes these loans accessible to borrowers with FICO scores as low as 500, even for those who have faced bankruptcy or foreclosure.

Minimum Credit Score

Unlike traditional lenders, private lenders typically don’t enforce strict minimum FICO score requirements. Instead, they evaluate the borrower’s overall financial situation and the value of the property being refinanced .

Equity Required

For cash-out refinancing, private lenders generally require at least 20% equity in the property, resulting in an 80% loan-to-value (LTV) ratio. For instance, in February 2026, a mining engineer with a $45,000 debt agreement refinanced his $455,000 property despite having no credit score. A specialist lender approved a $373,500 loan (83% LTV) with a variable interest rate of 4.69%, which was lower than the 5.59% offered by other lenders at the time.

Interest Rate Range

Interest rates from private lenders tend to be higher compared to traditional mortgages, reflecting the increased risk. In 2026, borrowers with poor credit often faced rates exceeding 7%, while borrowers with good credit enjoyed rates below 6.5%. Some private lenders, especially unregulated ones, charged between 2% and 6% per month, translating to annualized rates of 24% to 72%. Non-QM mortgage rates also ran about two percentage points higher than those offered by traditional financial institutions.

Closing Costs

Closing costs for private lender refinancing typically range from 2% to 6% of the loan amount. These costs cover various fees, including appraisals, origination, and administrative expenses. To offset the higher risk, private lenders often charge elevated origination fees.

Best For

This refinancing option suits real estate investors, self-employed individuals with unpredictable income, and borrowers needing quick access to cash for business purposes. The approval process is notably fast, often taking just 1 to 2 weeks, compared to the 30 to 60 days required by traditional banks.

Limitations

Despite its advantages, private lender refinancing comes with drawbacks. Loan terms are typically short, ranging from 6 months to 3 years, which may pressure borrowers to refinance or sell their property quickly. Many private lenders also don’t report payments to credit bureaus, so making timely payments won’t necessarily boost your credit score. Additionally, the private lending market has less regulatory oversight, so borrowers must carefully review loan terms to avoid predatory practices. There’s also a heightened risk of losing the property if it fails to generate expected returns or if refinancing isn’t secured before the loan term ends. These loans are often used as a short-term solution to improve credit before transitioning to conventional refinancing.

"Lenders perceive you as a higher risk. You may need to provide more documentation and prove a stable income. Expect a possibly longer underwriting and closing process, too."

- Dennis Shirshikov, Head of Content, Awning.com

Private lender refinancing can be a quick fix for those in urgent need of liquidity while working toward qualifying for traditional loans in the future.

Comparison of Refinancing Options

Refinancing can be a powerful tool, but the right choice depends on your financial circumstances. Below is a breakdown of refinancing programs tailored to homeowners with poor credit, highlighting their features and restrictions.

| Refinance Program | Min. Credit Score | Equity Required | Interest Rate Range | Closing Costs | Best For | Key Restrictions |

|---|---|---|---|---|---|---|

| FHA Streamline | None (lender varies) | None | Low | 2–5% (cannot be rolled in) | Current FHA borrowers seeking lower rates | Must show net tangible benefit; no cash-out allowed |

| FHA Cash-Out | 500–580 | 20% | Low | 2–5% (can be rolled in) | Homeowners needing cash with poor credit | Maximum 80% LTV; requires appraisal |

| VA IRRRL | None (lender varies) | None | Lowest available | 0.5% funding fee + 2–5% | Veterans refinancing existing VA loans | VA-to-VA only; no cash-out |

| USDA Streamline | None/620 (lender varies) | None | Low | 2–5% (can be rolled in) | Rural homeowners with USDA loans | Must save at least $50/month; rural areas only |

| Non‑QM Lender | Flexible (500+) | 20% | Highest (market rate + 2%) | 2–6% | Recent bankruptcy/foreclosure; self‑employed | Short loan terms (6 months to 3 years) |

| Private Lender | No strict minimum | 20% | Highest (market rate + 2%) | 2–6% | Real estate investors; quick cash needs | Less regulatory oversight; short terms |

| RefiNow/Refi Possible | None | 3% | Competitive | 2–5% (includes $500 appraisal credit) | Low‑to‑moderate income borrowers | Income ≤100% area median; DTI ≤65% |

Each program offers distinct benefits, so understanding their nuances can help you make an informed decision.

For veterans and service members, VA loans are a standout option due to their exceptionally low rates. As Maggie Overholt from The Mortgage Reports explains:

"VA loan rates tend to be significantly lower than conventional refinance rates."

This makes VA loans particularly appealing for those eligible.

Borrowers with credit scores between 500 and 620 might find FHA loans more accessible than conventional loans, which often require a minimum score of 620. Additionally, conventional loans may impose higher rates due to risk-based pricing for lower credit scores.

If you’ve faced recent financial setbacks like bankruptcy or foreclosure, Non-QM lenders and private lenders provide flexibility. However, these options come with higher interest rates – typically about 2% above traditional mortgage rates – and shorter terms, making them more suitable for specific needs like quick cash or investment opportunities.

Government-backed streamline programs, such as FHA Streamline, VA IRRRL, and USDA Streamline, often skip appraisals and income verification. However, they require proof of a "net tangible benefit", like a minimum 0.5% rate reduction, to ensure the refinance is worthwhile.

With the average refinance rejection rate hitting 25.6% in 2024, shopping around is crucial. Even for "no credit check" streamline loans, lenders may apply their own credit overlays, so comparing multiple offers can make a big difference .

For homeowners facing financial challenges or uncertainty about their refinancing eligibility, consulting a service like Foreclosure Defense Group can provide valuable insights and support throughout the process.

Conclusion

Even with poor credit, there are refinancing options available to help you manage your mortgage more effectively. Programs like FHA Streamline, VA IRRRL, and USDA Streamline Assist offer simplified processes with minimal paperwork. For those looking to tap into their home equity, the FHA Cash-Out option is available for credit scores as low as 500. If you’ve experienced bankruptcy or foreclosure, Non-QM loans could offer a path forward, though they often come with higher interest rates.

Steps to Strengthen Your Financial Profile

Before applying for refinancing, take steps to improve your financial standing. Start by reviewing your credit reports at AnnualCreditReport.com. Errors on credit reports are more common than you might think – about 20% of consumers have inaccuracies that can hurt their scores. Addressing these errors can make a big difference. Additionally, aim to keep your credit utilization below 30%, as this factor accounts for nearly 30% of your FICO score. Positive changes in utilization can reflect in your score within 30 to 60 days. Avoid opening new lines of credit during the refinancing process, as even one hard inquiry can temporarily drop your score.

Your payment history is even more important, making up 35% of your FICO score. If you’ve consistently made on-time payments for 6–12 months on your FHA, VA, or USDA loan, streamlined programs are more likely to overlook other credit issues. Another strategy is to add a co-signer with a strong credit score (above 760). This can improve your chances of qualifying for better rates, though the co-signer will share legal responsibility for the loan.

Consider the Costs and Timing

Before refinancing, calculate your break-even point. Closing costs usually range from 2% to 5% of the loan amount. By dividing these costs by your estimated monthly savings, you can determine how long you’ll need to stay in your home to recover your expenses. If your application is denied by automated underwriting, don’t give up – request a manual review. A human underwriter may consider factors like cash reserves or stable employment that automated systems might overlook.

If you’re dealing with foreclosure or unsure of your refinancing plan, reach out to Foreclosure Defense Group. They can provide expert legal advice on alternatives such as loan modifications or forbearance alongside refinancing options.

FAQs

Which refinance option is best for my situation?

When it comes to refinancing, the right option largely depends on your credit profile and what you aim to achieve financially. If you have poor credit, FHA loans might be your best bet. These loans typically have lower credit score requirements and more flexible guidelines, making them easier to qualify for. Plus, FHA streamline refinancing can make the process even smoother if you already have an FHA loan.

Another route to explore is lender-specific programs, which may offer options tailored to borrowers with less-than-perfect credit. You could also consider applying with a co-signer, as their stronger credit profile might help you secure better terms. And don’t overlook the long-term benefits of working on your credit score – improving it could open the door to more favorable refinancing options.

Will refinancing hurt my credit even more?

Refinancing with poor credit doesn’t have to damage your credit further – if you approach it strategically. While it’s true that poor credit can result in higher interest rates and fees, taking steps like improving your credit score beforehand and shopping around for the best lender can help soften the impact. Careful planning and proactive measures can make refinancing work in your favor.

How do I know if refinancing is worth the closing costs?

To figure out if refinancing makes sense financially, start by comparing the potential savings on your monthly payments or overall interest to the upfront closing costs. A key step is calculating the break-even point – the moment when your savings surpass the costs of refinancing. If you plan to stay in your home beyond that point, refinancing could be a smart move. Be sure to factor in your long-term plans, the terms of your current loan, and whether recent interest rate reductions could result in noticeably lower payments.

Related Blog Posts

- Refinancing vs. Loan Modification: Key Differences

- How to Refinance from ARM to Fixed-Rate Mortgage

- How Appraisals Affect Refinancing Costs

- How Private Lender Refinancing Stops Foreclosure