In Florida, foreclosures are judicial, meaning they go through the court system. Private mortgage foreclosures, initiated by individual lenders rather than banks or entities like Fannie Mae, follow the same legal process but often face fewer hurdles in proving the right to foreclose. Here’s a quick overview:

- Timeline: Typically takes 180 days but can extend to years if contested.

- Key Deadlines: Borrowers have 20 days to respond to a foreclosure lawsuit.

- Right of Recourse: Lenders can pursue a deficiency judgment if the sale doesn’t cover the debt.

- Steps: Missed payments → Demand/Breach Letters → Filing of Complaint → Court Judgment → Auction → Post-Sale Proceedings.

Florida homeowners should respond promptly to foreclosure notices, as ignoring them can lead to losing their homes without a chance to contest. Legal representation can help delay proceedings, challenge claims, or explore alternatives like loan modifications.

Florida Foreclosure Process Timeline: From Missed Payment to Sale

The Florida Foreclosure Process Explained

What Starts a Foreclosure?

Foreclosure begins when a homeowner falls behind on mortgage payments. After missing a payment, lenders typically allow a 10–15-day grace period before late fees start adding up. By around 30 days past due, lenders often send demand letters as a formal warning.

Federal law generally prevents loan servicers from starting foreclosure proceedings until a borrower is more than 120 days behind on payments. This window gives homeowners an opportunity to look into alternatives, like loan modifications or forbearance, by submitting a loss mitigation application. However, private lenders might have different rules based on the terms of your mortgage agreement.

In Florida, most mortgages require lenders to send a breach letter (also called an acceleration notice) before filing a foreclosure lawsuit. This letter informs the borrower of the default and provides a final chance to pay the overdue amount. If the lender skips this step, it could be a valid defense in court. Once the breach letter is sent and the default continues, the lender moves forward with legal action.

Filing the Foreclosure Complaint

If missed payments and default notices remain unresolved, foreclosure moves into the legal stage. The lender files a Complaint and a Lis Pendens in the court of the county where the property is located. The Lis Pendens serves as a public notice, alerting anyone checking the property records that the home is tied up in a lawsuit. This notice can complicate efforts to sell or refinance the property until the case is resolved. After filing, the court issues a Summons, which, along with the Complaint, must be served to the homeowner – usually through personal or substitute service.

To proceed, the lender must prove they have the legal right to foreclose. Under Fla. Stat. § 702.015, the lender needs to present the original mortgage note or, if it’s unavailable, provide a lost note affidavit along with documentation showing a clear chain of ownership. Only the rightful holder of the note can initiate foreclosure proceedings.

How Homeowners Can Respond and Defend

Homeowners have 20 days to respond to a foreclosure lawsuit. Ignoring this deadline can result in a default judgment, which allows the lender to move forward with selling the property without giving you a chance to contest the case.

Filing an Answer is essential. This formal response challenges the lender’s claims, addresses each allegation, and raises potential defenses. For example, you could question whether the lender has the legal standing to foreclose, argue that required notices weren’t properly delivered, or point out mistakes in the legal filings or the service of the lawsuit.

"A foreclosure plaintiff must show: an agreement; a default; an acceleration of debt to maturity; and the amount due." – Bank of Am., N.A. v. Delgado, 166 So. 3d 857, 859 (Fla. 3d DCA 2015)

The lender must prove all four elements listed above. If they can’t produce the original note, prove you defaulted, or show the debt was properly accelerated, you may have grounds to fight the foreclosure. Filing a written response not only delays a default judgment but also keeps your defenses intact while you explore other options like mediation or loss mitigation.

sbb-itb-d613a70

Court Procedures and Foreclosure Judgment

Summary Judgment and Trial Process

In Florida, most foreclosure cases are resolved through summary judgment. This process allows the lender to request a court ruling in their favor without the need for a full trial. The lender argues that there are no "genuine issues of material fact" requiring further debate in court.

To secure summary judgment, the lender must demonstrate – by a preponderance of the evidence – that four key elements are satisfied: the mortgage is valid, the borrower has defaulted, the loan has been accelerated, and the amount owed is accurate. If you’ve raised affirmative defenses in your Answer, the lender must also address and either factually disprove those defenses or show they lack legal merit.

"When a party raises affirmative defenses, a summary judgment should not be granted where there are issues of fact raised by affirmative defenses which have not been effectively challenged and refuted factually." – Alejandre v. Deutsche Bank Trust Co., 44 So. 3d 1288, 1289 (Fla. 4th DCA 2010)

To challenge summary judgment, you must file a counter-affidavit outlining disputed facts at least two business days before the hearing. If the judge determines that even a minor issue of material fact is in question, the request for summary judgment will be denied. In such cases, the matter moves forward to a full foreclosure trial, where evidence is formally presented, witnesses testify, and the lender must prove every aspect of their case. Before this trial, most judges require both parties to attempt mediation.

Final Judgment and Sale Date

If the lender prevails – either through summary judgment or a trial verdict – the judge will issue a Final Judgment of Foreclosure. This document specifies the total debt owed, including the loan principal, accrued interest, escrow advances (for taxes and insurance), legal fees, and attorney’s fees. It also sets a date for the public auction of the property.

Under Florida law, the foreclosure sale must be scheduled between 20 and 35 days after the Final Judgment is entered, though courts have the discretion to extend this timeline. The lender’s attorney must prepare and submit a foreclosure judgment packet – including the proposed Final Judgment, original note or lost note affidavit, Notice of Sale, and Certification of Compliance – at least five business days before the hearing.

Once the Final Judgment is signed, your right of redemption – the ability to reclaim your home by paying the total debt – ends when the Clerk of Court files the Certificate of Sale following the auction.

Foreclosure Sale and What Happens After

Public Auction and Sale Confirmation

In Florida, foreclosure sales are held through public auctions, which are often conducted online in counties like Miami-Dade, Broward, and Palm Beach. Lenders are required to publish sale notices weekly for two consecutive weeks, with a final notice appearing at least five days before the auction .

During the auction, the lender typically places a credit bid equal to the total debt owed. Third-party bidders, however, must submit a 5% deposit electronically before participating in the sale and pay the remaining balance by noon the next day. Once the auction concludes, the court clerk files a certificate of sale within one business day. If there are no objections filed within 10 days, the clerk will issue a certificate of title, officially transferring ownership to the winning bidder . These steps form the foundation for understanding what happens after the sale.

Post-Sale Rights and Deficiency Judgments

After the auction, both homeowners and buyers must adhere to Florida’s post-sale procedures. Unlike some states, Florida does not allow a post-sale redemption period. However, if the property sells for more than the total debt, the former homeowner can claim the surplus proceeds by contacting the court clerk within 10 days .

If the property sells for less than the debt owed, the lender has the option to seek a deficiency judgment. This judgment is limited to the difference between the outstanding debt and the property’s fair market value. The lender must file for this judgment within one year of the certificate of title being issued. Once the new owner takes possession of the property, they can request a writ of possession, which gives former occupants 24 hours to vacate if they haven’t already done so voluntarily .

If you’re dealing with uncertainties or difficulties during the foreclosure process, consulting with a legal professional can make a big difference. Foreclosure Defense Group provides experienced legal assistance to help homeowners navigate these intricate proceedings.

How Foreclosure Works in Florida (Step-by-Step Guide for 2026)

Foreclosure Timelines and Deadlines in Florida

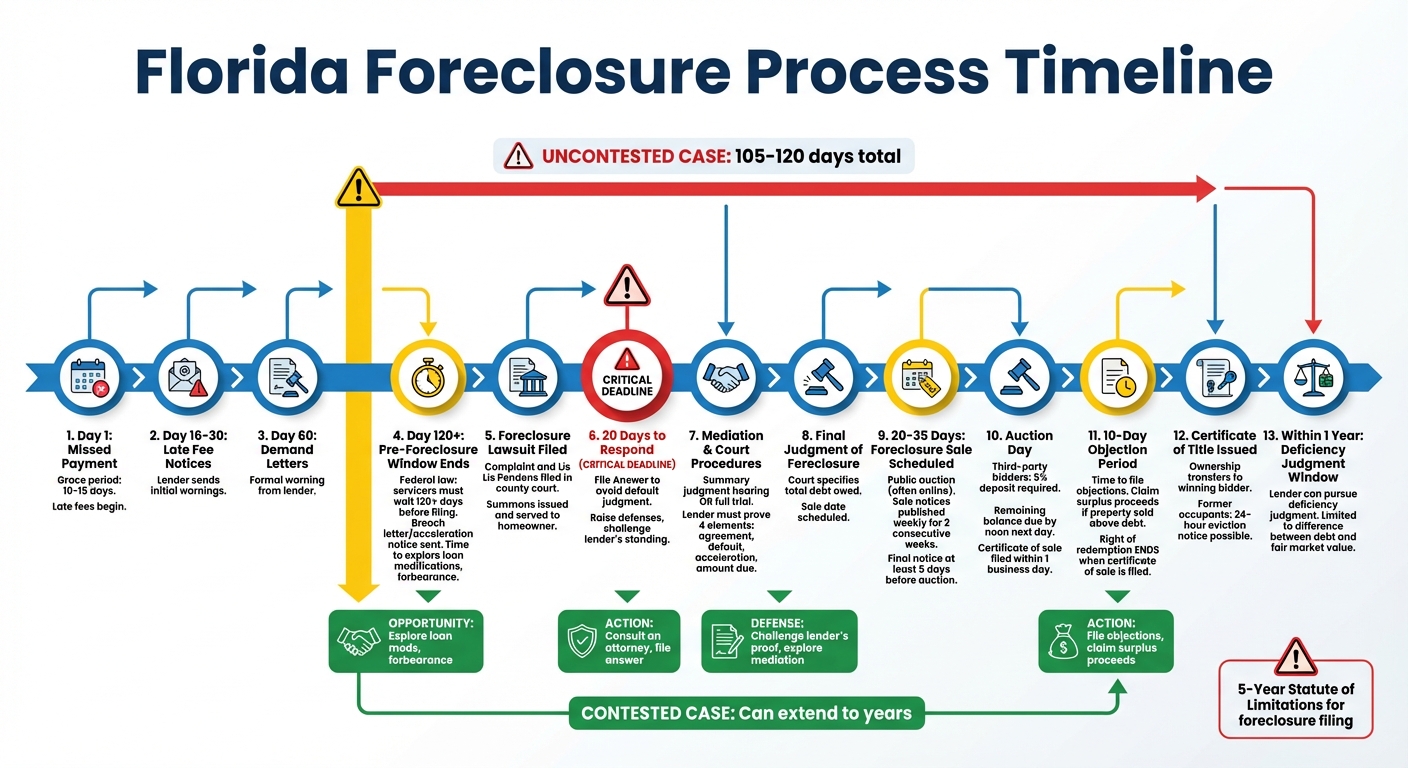

Grasping the foreclosure timeline is essential for homeowners to take action when it matters most. In Florida, the process can move quickly – an uncontested foreclosure (where no response is filed) might wrap up in as little as 105 days. On the other hand, cases with defenses can stretch on for years. This wide range underscores the importance of acting promptly at every stage.

The timeline kicks off when you miss a payment. Under federal law, servicers must wait until you’re over 120 days behind on payments before filing a foreclosure lawsuit. During this pre-foreclosure window, you might get late fee notices around day 16 and demand letters by day 60. These notices can be a chance to explore options like loan modifications or short sales.

Once the lawsuit is filed and served, you have 20 days to respond. Ignoring this can lead to a default judgment, with a foreclosure sale potentially happening 45–60 days after the initial filing. If a final judgment is entered, the property sale is typically scheduled 20–35 days later.

Your right to redeem the property – by paying off the entire loan balance – ends when the clerk files the certificate of sale. After that, there’s a 10-day window to file objections before the title is transferred. If you’re still living in the property after the title transfer, you could face a 24-hour eviction notice.

For lenders pursuing a deficiency judgment on residential properties with four or fewer units, they have one year from the day after the certificate of title is issued to file. Additionally, the statute of limitations for starting a foreclosure is five years.

Knowing these deadlines can make all the difference when navigating foreclosure defense.

Conclusion

Navigating Florida’s foreclosure process step by step can give you the tools to safeguard your home and finances. Since Florida follows a judicial foreclosure system, lenders must present their case in court. This provides you with a chance to address any procedural mistakes, confirm the lender’s legal standing, and consider options like loan modifications or short sales. Acting promptly is essential.

Here are some key points to remember: Uncontested foreclosures might wrap up in as little as 120 days, while contested cases can take significantly longer. The decisions you make within 20 days of receiving court documents could shape the entire outcome of your case.

Having an experienced attorney on your side can make a big difference. They can help delay proceedings, dispute deficiency judgments, or negotiate more favorable terms. As attorney Amy Loftsgordon explains: "Once you understand the Florida foreclosure process and your rights, you can make the most of your situation and, hopefully, work out a way to save your home or at least get through the process with as little anxiety as possible".

Don’t wait. Whether you’re at the beginning stages of missing payments or already facing a foreclosure complaint, reaching out to foreclosure defense attorneys or HUD-approved housing counselors can help you discover solutions you may not have considered. For tailored legal support that prioritizes your rights, contact Foreclosure Defense Group for a free consultation. Your home and financial security are worth the effort.

FAQs

Can I stop a Florida foreclosure after the lawsuit is filed?

Yes, stopping a foreclosure in Florida after a lawsuit has been filed is possible, but it requires taking specific legal steps. Some options include filing for bankruptcy, seeking a loan modification, or contesting the foreclosure in court. Florida law offers certain protections that could delay or even stop the process entirely. Speaking with a skilled foreclosure attorney can help you understand your options and decide on the best course of action for your circumstances.

What defenses work best against a private lender in Florida?

Effective ways to challenge a private lender in Florida include arguing lack of standing, pointing out the failure to deliver the required notice of default, invoking the statute of limitations, or asserting unclean hands. These strategies can question the lender’s claims and help safeguard your rights during foreclosure proceedings.

Will I still owe money after the foreclosure sale in Florida?

Yes, in Florida, you could still owe money after a foreclosure sale if the proceeds from the sale don’t fully cover your remaining mortgage balance. This leftover amount is known as a deficiency balance, and lenders can sometimes take legal steps to collect this amount from you.

Related Blog Posts

- 7 Legal Rights Every Florida Homeowner Should Know

- 3 Ways to Stop Foreclosure in Florida

- Florida Tenant Rights in Foreclosure Cases

- Deficiency Judgments in Florida: Key Facts