When your mortgage servicer mishandles your escrow account, it can lead to serious financial problems like unexpected payment increases, credit damage, or even foreclosure risks. Escrow accounts are designed to simplify property tax and insurance payments, but mistakes – such as overpayments, missed payments, or inaccurate calculations – can disrupt your budget and cause unnecessary stress.

Key takeaways:

- Escrow accounts divide annual property tax and insurance costs into monthly payments.

- Common errors include overcharging, undercharging, or failing to pay taxes or insurance on time.

- Federal law protects you, requiring servicers to investigate and fix errors within 30 business days.

- You can dispute errors by sending a written notice to your servicer and escalate unresolved issues to the CFPB or seek legal help.

Stay proactive by reviewing your escrow statements, verifying payments, and addressing discrepancies immediately. If issues persist, legal assistance may be necessary to protect your home and finances.

🏚Escrow Account Errors 🤑

sbb-itb-d613a70

Understanding Escrow Accounts in Mortgage Payments

An escrow account, also known as an impound or trust account, is a type of deposit account managed by your mortgage servicer. Its purpose? To handle property-related expenses like taxes and insurance on your behalf. Essentially, when you make your monthly mortgage payment, part of it goes toward your loan and part goes into this account.

Your monthly payment is structured using the PITI model: Principal, Interest, Taxes, and Insurance. The tax and insurance portions are set aside in the escrow account. For example, if your annual property taxes are $2,400 and your homeowner’s insurance is $1,200, your monthly contribution to escrow would be $300 ($3,600 divided by 12 months).

This system benefits both you and your lender. It ensures you’re not hit with large, unexpected bills, while also protecting the lender’s interest by avoiding issues like unpaid taxes, which could lead to tax liens on the property. Knowing how this works is key to spotting potential errors down the line.

How Escrow Accounts Handle Taxes and Insurance

Your mortgage servicer collects funds from your monthly payments and holds them in the escrow account. When your tax or insurance bills come due, the servicer uses the funds to pay those bills. To account for any unexpected increases, federal law allows lenders to include a "cushion" in the account. This cushion is limited to one-sixth of the annual escrow disbursements. For instance, if your yearly taxes and insurance total $3,600, the cushion can’t exceed $600. While this does raise your monthly payment slightly, it ensures there’s always enough money available.

Required Annual Escrow Analysis Under RESPA

The Real Estate Settlement Procedures Act (RESPA) mandates that mortgage servicers perform an escrow analysis at the end of each "computational year." This analysis reviews how much you’ve paid into escrow against the actual amounts disbursed. Servicers are required to provide this review within 30 days of the computation year’s end.

The analysis results in one of three outcomes:

- A shortage, meaning you’ve underpaid.

- A surplus, meaning you’ve overpaid.

- A balanced account, indicating everything is on track.

If there’s a surplus of $50 or more, the servicer must refund you the excess. For shortages, you typically have two options: pay the amount in full or spread it out over the next 12 months. The New York State Department of Financial Services explains the limits clearly:

"The lender may require that you pay into the escrow account each month no more than 1/12 of the total of all payments needed during the year, plus an amount necessary to pay for any shortage in the account. In addition, the lender may require a cushion, not to exceed an amount equal to 1/6 of the total amount needed for the year".

This yearly review ensures your payments stay accurate and prevents overcharges. However, errors in this process can lead to financial headaches for homeowners, as we’ll explore further.

Types of Loan Servicer Errors in Escrow Accounts

Loan servicers, even under federal oversight, can make mistakes that disrupt your finances. Being aware of common errors can help you catch issues early and avoid unnecessary stress.

Collecting Too Little in Escrow Funds

If your servicer underestimates property taxes or insurance premiums, it can lead to an escrow shortage. This means your account balance falls below the required target, including the cushion. You’re then left with two choices: pay the shortage in a lump sum within 30 days or spread it out over 12 months. Either way, your monthly mortgage payment increases, making it harder to stick to a budget or plan for the future.

Collecting Too Much in Escrow Funds

On the flip side, an escrow surplus happens when servicers overestimate costs or fail to adjust for reductions in taxes or insurance. While surpluses over $50 are refunded, it’s still inconvenient. Essentially, you’ve lent your servicer money without earning interest – money that could’ve been used to pay down debt or grow in a savings account. Worse, servicer mistakes can sometimes lead to missed payments, increasing financial risks.

Missing Tax or Insurance Payments

Sometimes, servicers fail to make timely tax or insurance payments, even though federal law requires it. A former Bank of America mortgage servicing specialist revealed:

"The system flags anomalies, but the queue to review them was always months behind. By the time someone catches a duplicate payment, the customer has already been paying an inflated amount for six months or more".

When property taxes go unpaid, your local government can place a lien on your property. If insurance coverage lapses, you’re left vulnerable to disasters like fires or storms. Federal law (12 C.F.R. § 1024.17) does require servicers to advance funds for these payments, even if your escrow account is short – but only if your mortgage payment is less than 30 days overdue.

Wrongly Imposed Force-Placed Insurance

If a servicer mistakenly believes your homeowner’s insurance has lapsed, they might purchase force-placed insurance on your behalf. These policies are much more expensive and offer less coverage. This mistake can cause an immediate escrow shortage, leading to payment shock – a sudden and steep rise in your monthly payment. Resolving such errors often involves a lengthy process, adding to the financial and emotional toll.

Failed Escrow Adjustments After Loan Changes

Servicers sometimes fail to update escrow accounts when property taxes, insurance premiums, or loan terms change. This can result in "sticker shock" when the annual escrow analysis reveals a significant shortage. Under RESPA, servicers are required to conduct this analysis annually, but delays or calculation errors can leave you dealing with unexpected payment increases. Regularly reviewing your escrow account is key to avoiding these surprises and maintaining financial stability.

Consequences of Escrow Errors for Homeowners

Escrow errors can lead to major financial and legal challenges, putting both your home and credit at risk.

Credit Score Damage and Late Payment Risks

When payments are misapplied, you could be mistakenly marked as delinquent. This can harm your credit score, lead to automatic late fees, and complicate refinancing or other financial plans. If your servicer neglects to pay your property taxes, your local government might place a tax lien on your home. In some cases, unresolved issues could even result in foreclosure actions.

Federal law does provide some protection, but you may still feel the financial strain initially. For example, if a servicer forgets to pay your insurance or tax bill, they are required to fix the mistake within 30 business days and cover any penalties caused by the delay:

"If it turns out that the servicer did forget to pay the insurance or tax bill, it must correct the error within 30 business days… and cover the cost of any penalties imposed due to the late disbursement".

However, you might have to pay these charges upfront while waiting for the servicer to resolve the issue.

Your Rights Under RESPA Regulations

Federal protections, particularly under the Real Estate Settlement Procedures Act (RESPA), are in place to safeguard your rights when escrow errors occur. Acting quickly is key. You can send a written notice of error to your servicer’s designated address, as outlined in RESPA § 1024.35.

Once your notice is received, the servicer must:

- Acknowledge it within 5 business days.

- Investigate and resolve the issue within 30 business days.

During this time, they cannot report any negative information about the disputed payment to credit bureaus for 60 days. Additionally, they are not allowed to charge any fees or demand payment related to their investigation. If the servicer fails to respond or resolve the issue properly, you may have the right to take legal action to recover actual damages, statutory damages, and attorney’s fees.

These protections ensure you have a way to hold servicers accountable while safeguarding your financial stability.

How to Find and Fix Escrow Account Errors

How to Identify and Dispute Escrow Account Errors: A Step-by-Step Guide

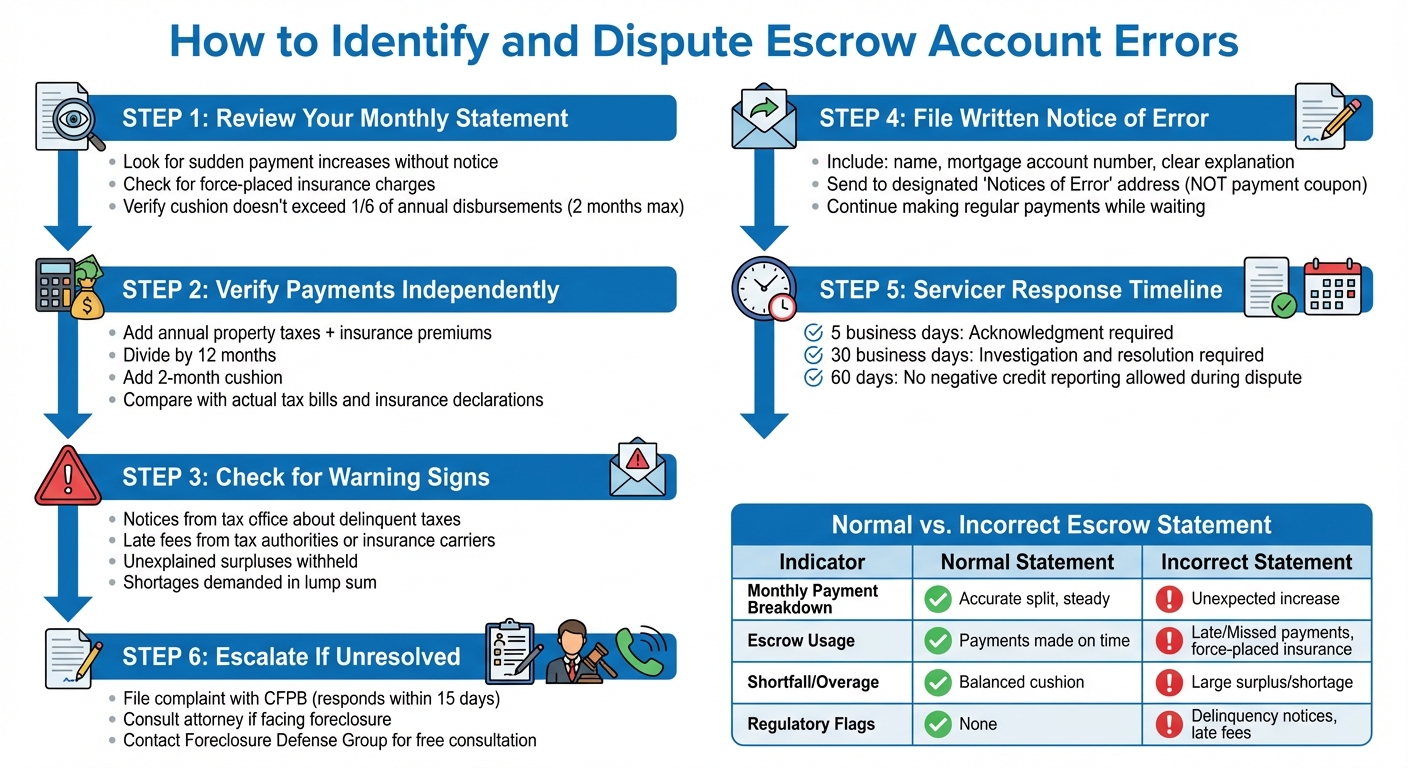

Catching escrow account errors early can save you from unnecessary headaches like credit issues or tax liens. The secret lies in knowing how to spot these errors and acting quickly to address them.

Reading Your Escrow Statements for Errors

Your monthly mortgage statement can reveal potential escrow problems if you know what to look for. For instance, if your total monthly payment suddenly jumps without any prior notice about increased property taxes or insurance premiums, it’s a red flag.

Another warning sign: notices from your local tax office about delinquent property taxes. This likely means your mortgage servicer didn’t make the required payments from your escrow account on time. Similarly, charges labeled as "force-placed" or "lender-placed" insurance could appear even if you already have active coverage. Keep in mind that federal law limits the escrow account cushion to no more than one-sixth (or two months) of your total annual disbursements. Anything beyond this is not allowed.

To verify your escrow payments, add your annual property taxes and insurance premiums, divide by 12, and include the two-month cushion. Cross-check these numbers with your actual tax bills and insurance declarations. If something doesn’t add up, investigate and dispute the errors immediately.

Filing a Notice of Error with Your Servicer

If you find an error, sending a written notice is the first step to activating federal protections under RESPA (Real Estate Settlement Procedures Act). Your letter should include your name, mortgage account number, and a clear explanation of the issue. Importantly, don’t write this notice on a payment coupon, as servicers are not required to treat it as a formal dispute. The Consumer Financial Protection Bureau explains:

"A notice on a payment coupon or other payment form supplied by the servicer need not be treated by the servicer as a notice of error".

Send your letter to the address specifically designated for "Notices of Error" or "Qualified Written Requests." This address is often different from where you send payments, so check your monthly statement or the servicer’s website. Once the notice is received, strict timelines kick in for acknowledgment and resolution. During this period, servicers cannot report negative information about the disputed payment to credit bureaus for 60 days. However, continue making your regular payments while waiting for their response.

Table: Normal vs. Incorrect Escrow Statements

Here’s a quick comparison to help you identify normal versus problematic escrow statements:

| Indicator | Normal Escrow Statement | Incorrect Escrow Statement |

|---|---|---|

| Monthly Payment Breakdown | Changes only after annual analysis or specific tax/insurance rate change notice | Sudden, unexplained increases without corresponding tax or insurance hikes |

| Escrow Usage | Taxes and insurance paid on or before deadlines to avoid penalties | Late fees from tax authorities or insurance carriers; notices of unpaid bills or tax liens |

| Shortfall/Overage | Surpluses of $50+ refunded within 30 days; shortages spread over at least 12 months | Surpluses withheld without explanation; shortages demanded in a single lump sum |

| Regulatory Flags | Cushion no more than 1/6 of annual disbursements; annual statement provided within 30 days | Cushion exceeds legal limit; force-placed insurance despite proof of coverage |

Getting Help to Resolve Escrow Problems

Fixing Errors and Getting Refunds

When you send a Notice of Error to your mortgage servicer, they are required to acknowledge it within five business days. From there, they have 30 business days to either resolve the issue or provide an explanation. If they confirm an error, they must take steps to fix it. This includes adjusting your account balance, removing incorrect late fees (like charges for force-placed insurance), and refunding any overpayments. If they determine no error occurred, they must send you a written explanation detailing their reasoning. Attorney Amy Loftsgordon explains:

"After receiving a notice of error, the servicer must fix the mistake by the deadline, let you know about the correction, and give you contact information so you can get further help if needed."

If you disagree with their findings or if they fail to meet the required deadlines, you can escalate the matter to the Consumer Financial Protection Bureau (CFPB), which typically responds within 15 days.

For disputes that go beyond simple corrections, legal assistance may become necessary.

Legal Help from Foreclosure Defense Group

Sometimes escrow issues can spiral into more serious problems, such as foreclosure proceedings. For example, servicers might misapply escrow funds or engage in "dual-tracking" – pursuing foreclosure while a loan modification is still under review. In such cases, acting quickly is crucial. The Consumer Financial Protection Bureau advises:

"If you have an escrow account and your mortgage servicer fails to pay your property taxes, or if you are facing imminent foreclosure or have been served with legal papers, you may need to consult an attorney."

Foreclosure Defense Group specializes in helping homeowners navigate these complex issues. Their attorneys are experienced in enforcing federal laws like RESPA to hold servicers accountable. They provide services such as foreclosure defense, loan modification assistance, and bankruptcy guidance. If you’re dealing with a servicer who refuses to acknowledge clear mistakes or if you’ve received foreclosure notices while disputing an escrow error, legal intervention can help protect your home. They offer free consultations to review your case and explore options to prevent wrongful foreclosure.

Conclusion

Mistakes in escrow accounts can lead to unexpected payment increases, harm your credit, or even put your home at risk of foreclosure. While your loan servicer manages the account, you are still responsible for ensuring that property taxes and insurance premiums are paid on time. Stay vigilant by keeping a close eye on your bills.

Fortunately, federal regulations provide important protections. Compare your annual escrow analysis with your actual tax and insurance bills, and double-check disbursements with local government records to catch errors early. If you spot an issue, report it immediately in writing.

If routine corrections don’t resolve the problem or a dispute escalates to the point where foreclosure becomes a concern, it’s time to seek legal advice. Foreclosure Defense Group is experienced in holding loan servicers accountable, stopping improper practices, and defending homeowners’ rights. They offer free consultations to help you understand your options and protect your home from wrongful foreclosure.

The key is to act quickly. Keep detailed records of any discrepancies, verify payments independently, and escalate unresolved issues to the CFPB or legal professionals if necessary. Taking prompt action can make all the difference in protecting your finances and your home.

FAQs

How do I know if my escrow payment is wrong?

To determine if your escrow payment is off, start by carefully reviewing your mortgage statements and bills. You can also request a detailed escrow analysis from your loan servicer. This analysis will help you compare actual costs with your escrow account balance. Be especially alert if you receive notices about unpaid taxes or insurance – these could signal a problem with your escrow account.

What should I include in a Notice of Error letter?

When writing a Notice of Error letter, make sure to include the following:

- Your full name, address, and mortgage account number: This information helps the servicer identify your loan.

- A detailed explanation of the error: Be specific – include dates, amounts, or payment details to clarify the issue.

- Relevant supporting documents: Attach items like notices from taxing authorities or insurance companies if the error involves escrow.

- Send it to the correct address: Use the servicer’s designated error correction address, not the payment address. Always keep a copy of the letter for your records.

By following these steps, you can ensure your letter is clear and reaches the right department.

When should I contact a foreclosure attorney about escrow issues?

If escrow mistakes threaten your property or put you at risk of foreclosure, reach out to a foreclosure attorney right away. This could involve cases where the loan servicer doesn’t pay escrowed taxes or insurance, or if you believe escrow issues have led to a wrongful foreclosure. Taking swift action can safeguard your rights and help resolve the issue before it worsens.

Related Blog Posts

- How Attorneys Help Resolve Mortgage Disputes

- Escrow Errors vs. Lender Mismanagement

- Top Refinancing Mistakes with Escrow Fees

- Common Lender Errors in Foreclosure Cases