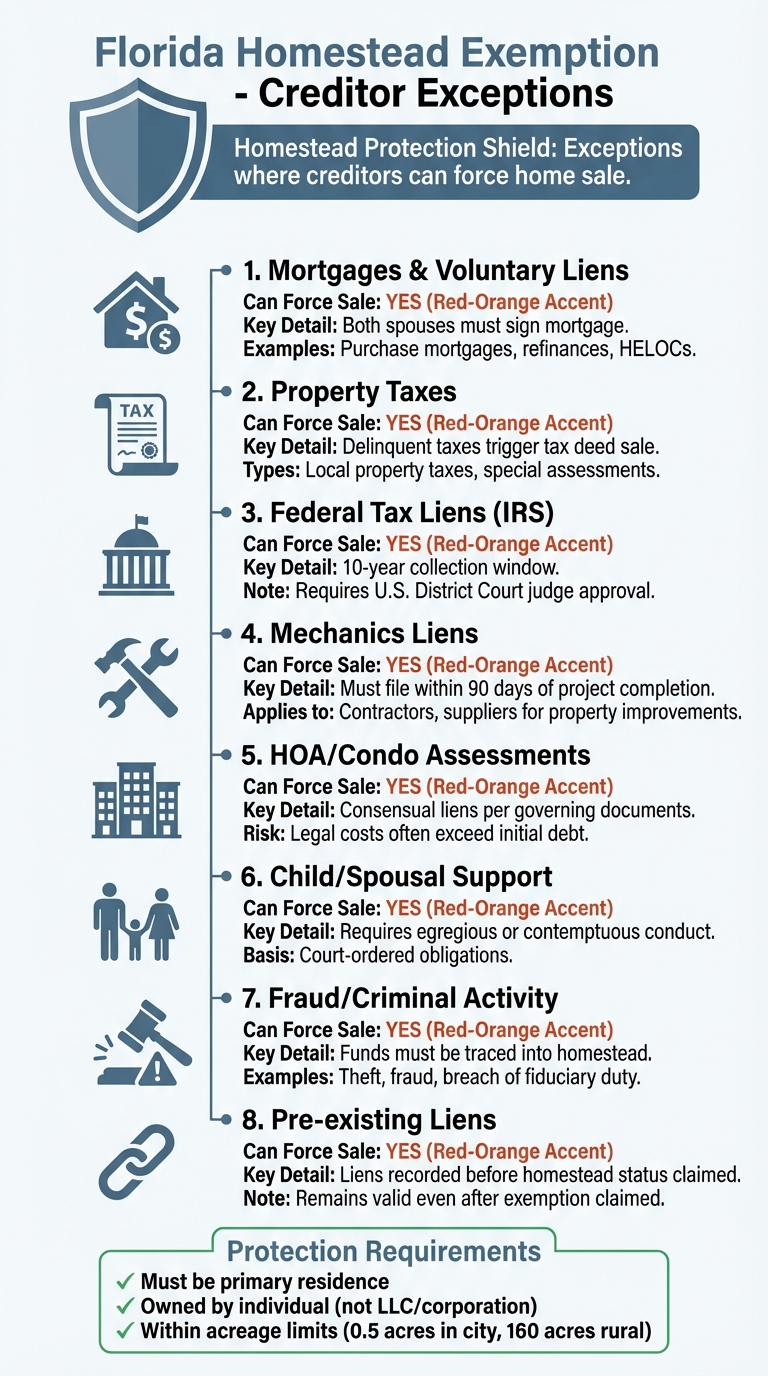

Florida’s homestead exemption protects your primary residence from most creditors, regardless of its value. However, there are key exceptions where creditors can force the sale of your home. These include:

- Mortgages & Voluntary Liens: Defaulting on loans secured by your home.

- Property Taxes: Unpaid local or federal taxes.

- Mechanics Liens: Debts to contractors or suppliers for property improvements.

- HOA/Condo Assessments: Unpaid dues tied to association agreements.

- Child/Spousal Support: Court-ordered obligations in cases of egregious behavior.

- Fraud/Criminal Activity: Funds obtained illegally and tied to the property.

- Pre-existing Liens: Liens recorded before claiming homestead status.

To qualify for this protection, your home must be your primary residence, meet acreage limits, and be owned by an individual (not an LLC or corporation). Planning strategies, such as proper titling and prioritizing specific debts, can help safeguard your property from these exceptions.

Florida Homestead Exemption: 8 Creditor Exceptions That Can Force Home Sale

Are You Falling For These Florida Homestead Myths?

sbb-itb-d613a70

How Florida Homestead Protection Works

Florida’s homestead protection, outlined in the state constitution (Article X, Section 4), offers a powerful safeguard for homeowners. It ensures that the full equity of your primary residence is protected from most creditors, regardless of the property’s value.

This protection kicks in automatically when you establish your residence. Unlike the homestead tax exemption – which requires an annual filing with your county property appraiser by March 1 – creditor protection does not involve any paperwork. However, it only applies if you meet certain residency and ownership requirements.

Who Qualifies for Homestead Protection

To qualify, the property must be owned by an individual (not a corporation or trust) and serve as their primary, permanent residence. Florida courts rely on evidence like your driver’s license, voter registration, or vehicle registration to confirm your permanent residence status.

There are also limits based on the property’s location. If the home is within city limits, protection covers up to half an acre of contiguous land. Outside city boundaries, this extends to 160 acres. Interestingly, if a rural property is annexed into a city, existing owners can retain ("grandfather in") the full 160-acre protection. However, future buyers of the same property would be restricted to the city’s half-acre rule.

Once you meet these qualifications, your home is protected from most general claims by creditors.

What Debts Are Normally Protected

The homestead exemption shields your home from most unsecured debts and general civil judgments. This includes debts from credit cards, medical bills, and personal injury claims. Creditors in these cases cannot force the sale of your home to settle such debts.

A notable example is the 2001 case Havoco of America, Ltd. v. Hill. In this case, the Florida Supreme Court ruled that a debtor who purchased a $650,000 home shortly after being hit with a $15 million judgment still retained full homestead protection. This decision highlights the strength of Florida’s homestead laws in protecting homeowners from unsecured creditors.

That said, some debts – like those tied to statutory obligations or liens – are exceptions to this rule. These exceptions will be discussed in the next section.

Debts That Can Override Homestead Protection

While Florida’s homestead exemption offers strong protection against creditors, there are specific situations where this protection doesn’t apply. These exceptions allow creditors to force the sale of a homestead property, even if substantial equity has been built.

Here’s a closer look at the types of debts that can bypass homestead protection.

Mortgages and Voluntary Liens

When you take out a mortgage or refinance, you voluntarily waive homestead protection by using your property as collateral. This includes purchase-money mortgages, refinances, and home equity lines of credit. Florida law requires that both spouses sign the mortgage, even if the property is titled in only one name. This ensures that one spouse cannot jeopardize the family’s home without the other’s consent. If you default on these obligations, the lender can foreclose, leading to a forced sale.

Property Taxes and Government Liens

Unpaid property taxes are another exception. Local governments can initiate a tax deed sale to recover delinquent property taxes or special assessments. Additionally, under the Supremacy Clause of the U.S. Constitution, federal tax liens from the IRS can attach to a homestead if taxes remain unpaid after a demand for payment.

As asset protection attorney Jon Alper points out:

"The IRS is the most significant exception to Florida’s homestead protection."

Although the IRS rarely forces the sale of a primary residence (requiring approval from a U.S. District Court judge), the lien remains attached until resolved, often through a sale or refinance. The IRS has a 10-year window to collect after the tax is assessed.

Construction and Mechanics Liens

If you hire contractors or suppliers to improve your property and fail to pay them, they can file a mechanics lien. Florida law allows such liens for property improvements. To enforce these liens, contractors must send a "Notice to Owner" within 45 days of starting work and record the lien within 90 days of completing the project. Legal action to foreclose on the lien must generally occur within one year of recording, or within 60 days if you file a "Notice of Contest."

Homeowners’ association (HOA) and condominium association liens are treated similarly. By purchasing the property, you agree to abide by the association’s governing documents, which makes these liens consensual.

Child Support and Spousal Support

Family support obligations, like child support and alimony, can override homestead protection due to public policy considerations. Courts may impose an equitable lien on a homestead if the debtor’s behavior is deemed egregious or contemptuous – such as using the homestead exemption to avoid support payments.

For example, in the 2005 case Partridge v. Partridge, the Florida Fourth District Court of Appeal allowed foreclosure to satisfy a support obligation, stating:

"Contemptuous conduct may certainly be the functional equivalent of fraud, and it represents the kind of reprehensible conduct justifying foreclosure."

Similarly, in the 2007 case Sell v. Sell, the court permitted attorneys’ fees to be paid from homestead proceeds due to the husband’s "fraudulent, egregious, and consistently contemptuous" behavior.

Fraud and Criminal Activity

Homestead protection does not cover property purchased or improved using funds obtained through fraud, theft, or breach of fiduciary duty. Courts can impose an equitable lien if stolen or defrauded funds are directly traced into the homestead. As Jon Alper explains:

"Money obtained through fraud, theft, or breach of fiduciary duty cannot be converted into homestead protection."

However, using legally owned funds to purchase or improve a homestead is protected, even if done to shield assets from creditors. The Florida Supreme Court has clarified:

"Converting cash into a home to shelter it from a pending judgment is not, by itself, fraudulent."

It’s also important to note that if a judgment lien is recorded before a property gains homestead status (e.g., when it was a secondary home), that lien remains valid even after the homestead exemption is claimed.

| Exception Type | Can Force Sale? | Key Requirement |

|---|---|---|

| Purchase Money Mortgage | Yes | Both spouses must sign |

| Property Taxes | Yes | Delinquent taxes |

| Construction Liens | Yes | Perfected within deadlines |

| HOA/Condo Liens | Yes | Consensual per governing documents |

| Federal Tax Liens | Yes | Cleared upon sale/refinance |

| Support Obligations | Yes | Egregious conduct required |

| Fraud/Criminal Activity | Yes | Funds traced into homestead |

| Pre-existing Liens | Yes | Attached before homestead status |

How These Exceptions Affect Homeowners

Common Scenarios and Risks

Certain exceptions can leave your property vulnerable in ways you might not expect. One of the most frequent issues is property tax delinquency. Falling behind on property taxes can lead to a tax deed sale, putting your home at risk.

Another common pitfall involves HOA and condominium assessments. Unpaid dues can quickly snowball with late fees and penalties. Because these assessments are considered consensual liens, homeowners associations can foreclose on your property, much like a mortgage lender. The legal costs involved can often exceed the initial debt.

Mechanics liens are another potential hazard, especially during renovation projects. Even if you’ve paid your general contractor in full, unpaid subcontractors or suppliers can file mechanics liens against your home. If these liens are properly filed and perfected, they could lead to a forced sale of your property.

Abandonment of your home also creates risks. Moving out, renting the property, or transferring the title to an LLC removes its constitutional protection, making it vulnerable to judgment liens. This protection also disappears if you buy a second home and designate it as your primary residence.

Understanding these risks is the first step toward protecting your property.

Planning to Protect Your Homestead

To safeguard your home against these exceptions, consider implementing these strategies. For married couples, holding the title as "tenants by the entirety" rather than as tenants in common or in one spouse’s name can offer extra protection. This structure shields the property from creditors pursuing one spouse. Following the Florida Supreme Court’s December 2025 decision in Loumpos v. Dove Investment Corp., couples can also more easily convert individual bank accounts into protected tenancy by the entirety accounts by signing a new signature card.

If you’re using a revocable living trust for estate planning, make sure the trust explicitly designates the property as a Florida homestead and grants the beneficiary occupancy rights. Without this specific language, constitutional protections may not apply.

When selling your homestead, it’s crucial to keep the sale proceeds separate and reinvest them into a new Florida homestead promptly. Mixing these funds with other money or delaying the purchase of a new home could jeopardize their protection from creditors.

For those dealing with financial struggles, prioritize payments for property taxes and HOA dues over unsecured debts. While credit card companies can’t force the sale of your home, tax authorities and HOAs can. If bankruptcy is on the table, remember that the homestead exemption is capped at $189,050 if you purchased the property within 1,215 days (about 40 months) before filing.

Lastly, avoid transferring your primary residence into an LLC. While it might seem like a smart asset protection move, doing so removes the constitutional homestead protection, which is reserved for properties owned by natural persons.

If you’re facing foreclosure or creditor challenges, seek advice from a qualified attorney. The Foreclosure Defense Group offers free consultations to help homeowners navigate these complex issues and protect their homestead rights.

Conclusion

Florida’s homestead exemption offers strong protection for your primary residence, but it’s not absolute. Certain exceptions – like mortgages, property taxes, HOA assessments, mechanics liens, and support obligations – can still put your home at risk.

"The homestead exemption is the strongest creditor protection in Florida. The Florida Constitution protects a person’s primary residence from forced sale by judgment creditors. The protection has no dollar cap." – Jon Alper, Asset Protection Attorney

While state laws provide robust protection, they come with conditions. Proper titling, proof of residency, and adherence to acreage limits are critical. Additionally, federal bankruptcy law caps protection at $189,050 if the property was purchased within 1,215 days before filing.

Taking proactive steps can make a big difference. Ensure your property is titled correctly, maintain clear residency records, and prioritize payments on debts like property taxes and HOA assessments that can override homestead protection. If you sell your home, keep the sale proceeds separate and avoid transferring ownership to a business entity. These steps align with earlier advice on securing your homestead. For lingering questions or specific concerns, consulting a legal expert is always a wise move.

Getting Legal Help

Given the complexities of Florida’s homestead laws, professional legal guidance is often essential. If you’re dealing with foreclosure, creditor issues, or need help understanding your rights, having an experienced attorney can make all the difference. From using the Notice of Homestead process under Florida Statute § 222.01 to navigating the 45-day window for creditor contests, the expertise of a legal professional is invaluable.

Foreclosure Defense Group offers free consultations to help homeowners protect their property. Whether you’re facing foreclosure, bankruptcy, or creditor claims, their team is ready to provide the assistance you need. Visit https://foreclosuredefensegroup.com to schedule your consultation and take the first step toward safeguarding your home.

FAQs

Can a credit card judgment ever force the sale of my Florida homestead?

No, a credit card judgment generally cannot force the sale of your Florida homestead. Under the Florida Constitution, your primary residence is protected from forced sales or liens by most creditors, including those tied to credit card debt. This protection applies as long as your property meets the criteria for a homestead, ensuring your home remains shielded from such claims.

Does putting my home in a trust or LLC affect homestead creditor protection?

When you place your home in a well-structured revocable trust, Florida’s homestead creditor protections usually remain intact. This is because the trust allows you to maintain control and reside in the property during your lifetime. On the other hand, transferring your home to an LLC often eliminates these protections since an LLC is treated as a separate legal entity.

Are my homestead sale proceeds protected, and for how long?

Under Florida law, the proceeds from the sale of a homestead are typically safeguarded as long as they are kept separate and used to purchase a new homestead within a reasonable period. Alternatively, these funds may stay protected if they are deposited into a financial asset that qualifies for exemption. Proper handling of these funds is crucial to ensure these protections remain intact.

Related Blog Posts

- 7 Legal Rights Every Florida Homeowner Should Know

- 3 Ways to Stop Foreclosure in Florida

- Deficiency Judgments in Florida: Key Facts

- Florida Homestead Exemption: Step-by-Step Guide