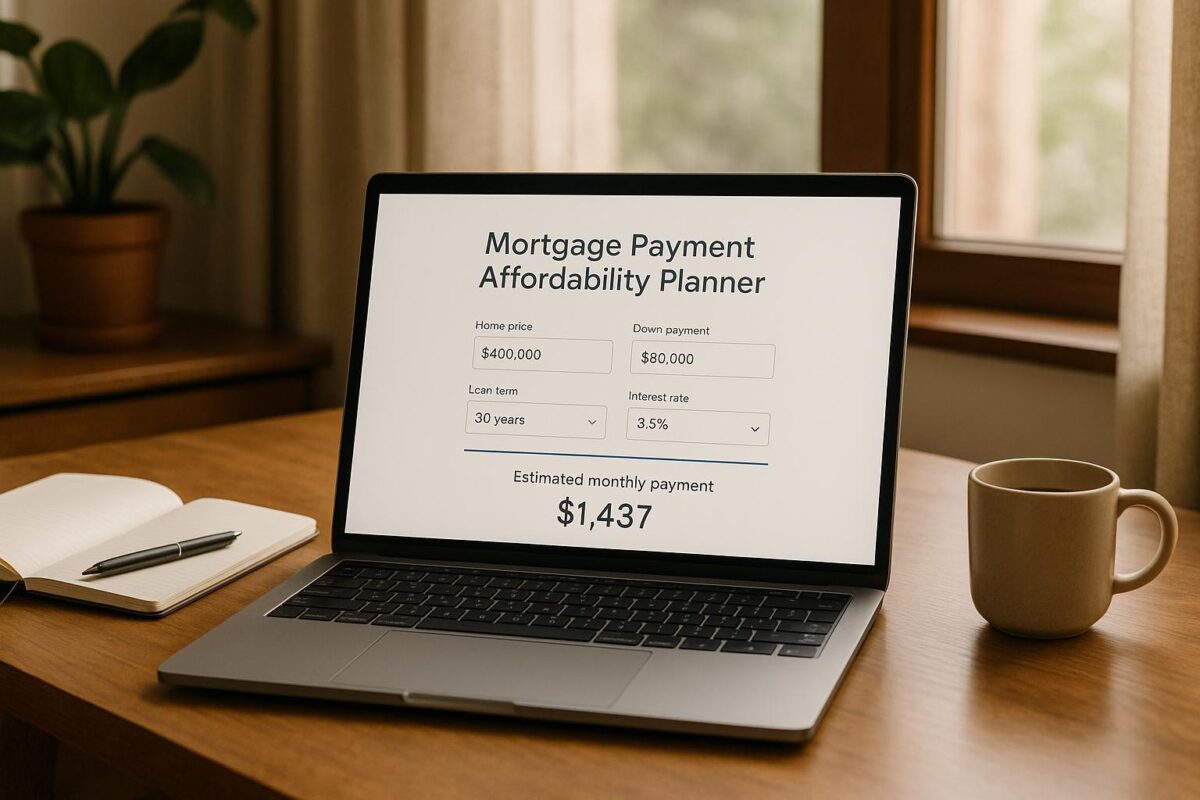

Plan Your Home Purchase with a Mortgage Affordability Tool

Buying a home is one of life’s biggest financial decisions, and understanding your budget is the foundation of a smart purchase. A mortgage payment affordability planner can be a game-changer, helping you figure out a realistic price range before you start house hunting. By entering details like your income, debts, and preferred loan terms, you get a clear snapshot of what’s within reach without stretching your finances too thin.

Why Knowing Your Limit Matters

It’s easy to fall in love with a dream home, only to realize the monthly payments are out of reach. Using a tool to estimate your housing budget keeps expectations grounded and prevents financial stress down the road. These calculators often follow trusted guidelines, ensuring the suggested payment aligns with what most lenders consider manageable. Plus, they account for variables like interest rates and down payments, tailoring the results to your unique situation.

Take the First Step

Whether you’re a first-time buyer or upgrading to a new place, starting with a home loan affordability tool empowers you to shop confidently. It’s a small step that can save time, narrow your search, and set you up for a smoother journey to homeownership.

FAQs

What is the 28% rule for mortgage affordability?

The 28% rule is a common guideline used by lenders and financial advisors. It suggests that your monthly mortgage payment shouldn’t be more than 28% of your gross monthly income after accounting for other debts. For example, if you earn $5,000 a month and have $500 in debt payments, the remaining income is considered, and your mortgage payment should ideally stay under $1,400. This helps ensure you’re not overextending yourself financially and can still cover other living expenses.

How accurate is this mortgage affordability planner?

Our tool provides a solid estimate based on standard guidelines like the 28% rule, using the financial details you provide. However, it’s not a substitute for professional financial advice or a loan approval from a lender. Things like credit scores, local housing markets, and specific lender requirements can affect what you’re ultimately approved for. Think of this as a starting point to get a sense of your budget before diving deeper with a mortgage expert.

Why does down payment percentage matter in the calculation?

The down payment percentage directly impacts the loan amount you’ll need to borrow, which in turn affects your monthly payments. A higher down payment means a smaller loan, leading to lower monthly costs and often better interest rates. For instance, putting 20% down versus 5% can save you thousands over the life of the loan. Our tool factors this in to give you a realistic picture of what you can afford based on how much you’re able to pay upfront.